Go Back

Lin

Weekly Market Update: Patience

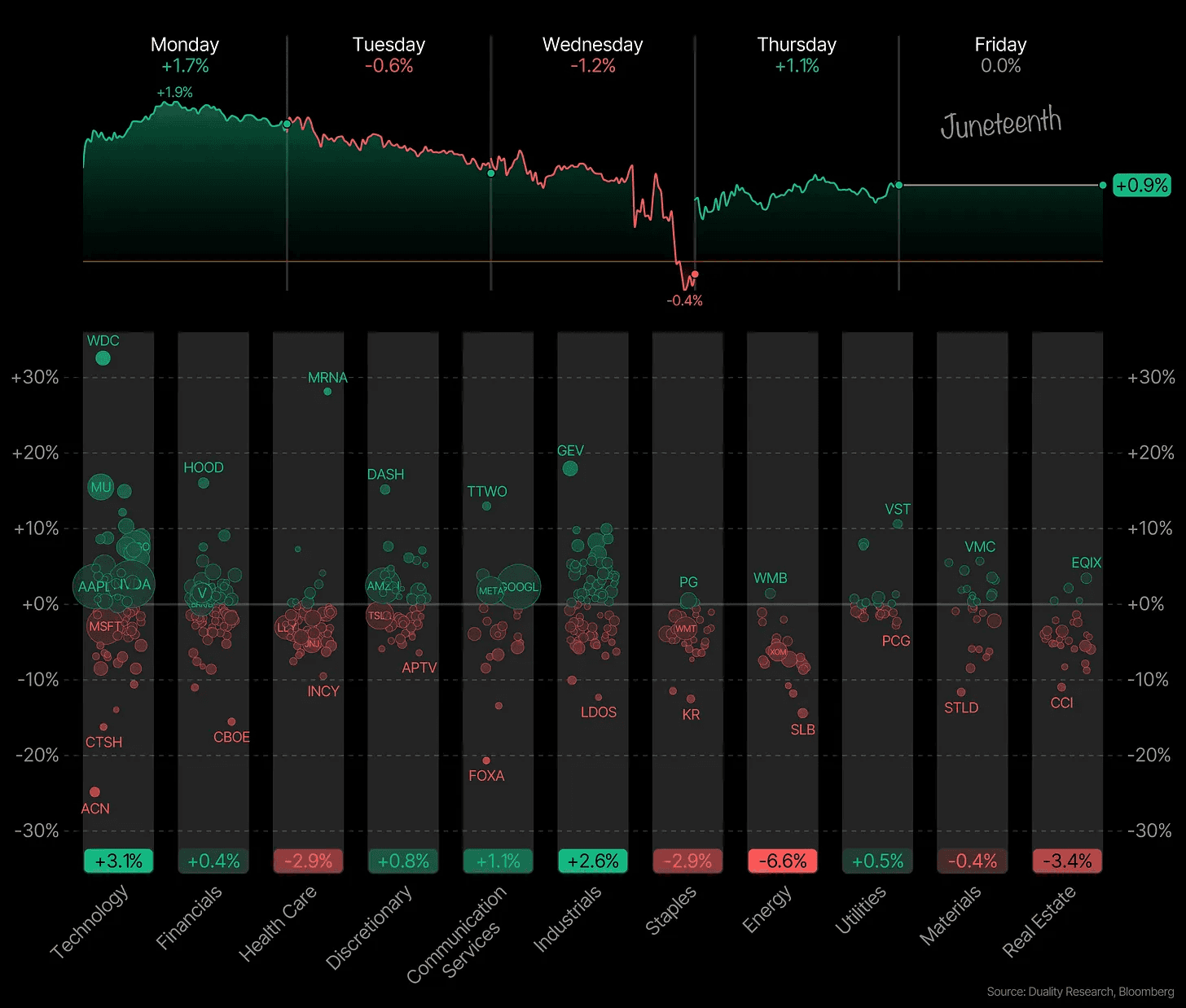

This past week, we made it through pretty much every major catalyst the market had been worried about.

Whether it was high inflation data, the liquidity drain from the SpaceX IPO, the Iran deal, or Kevin Warsh’s debut as the new Fed Chair, everything the market was worried about now appears to be in the rearview, at least for now.

That’s what you call a resilient market.

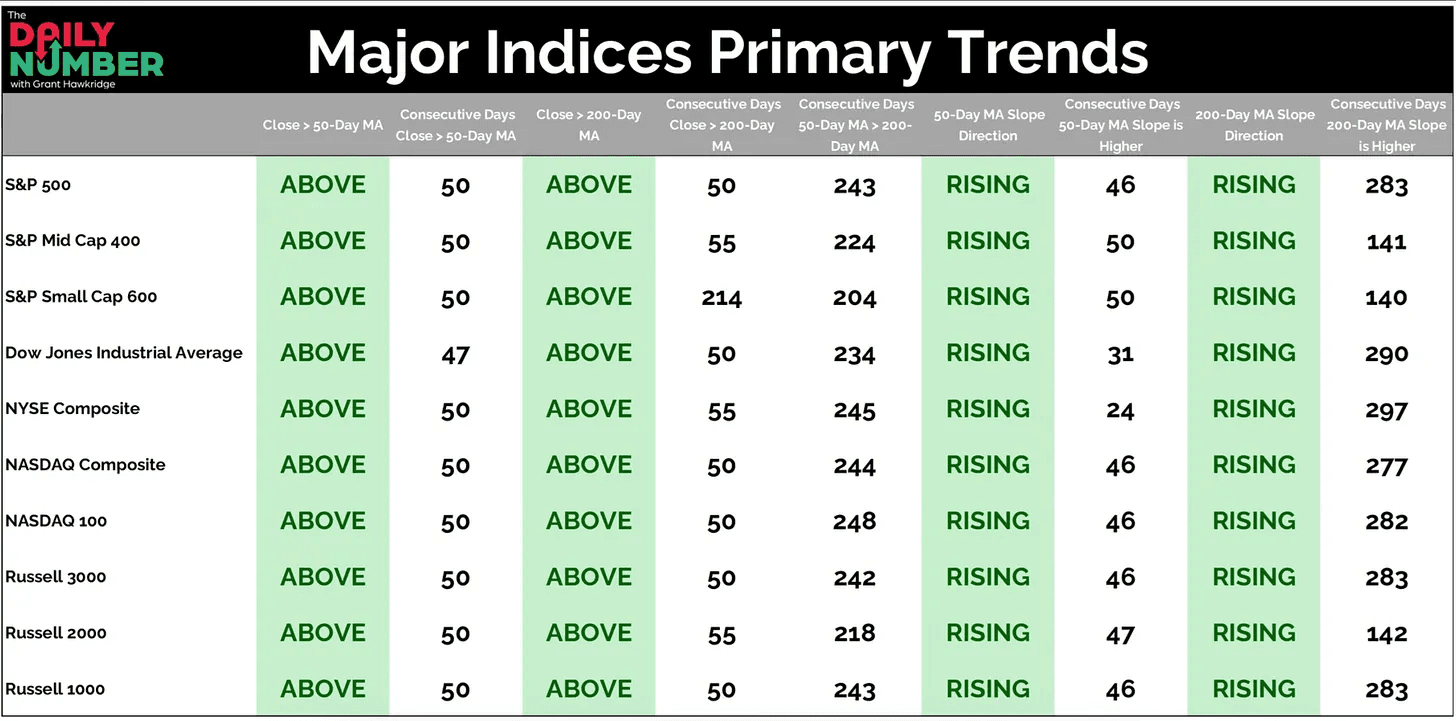

Every major index, the S&P 500, the Dow, the Nasdaq, the Russell 2000, all of them, sits above both its 50 day and 200 day moving average right now. Every one of those moving averages is also rising. That’s about as textbook a definition of an uptrend as you’ll find.

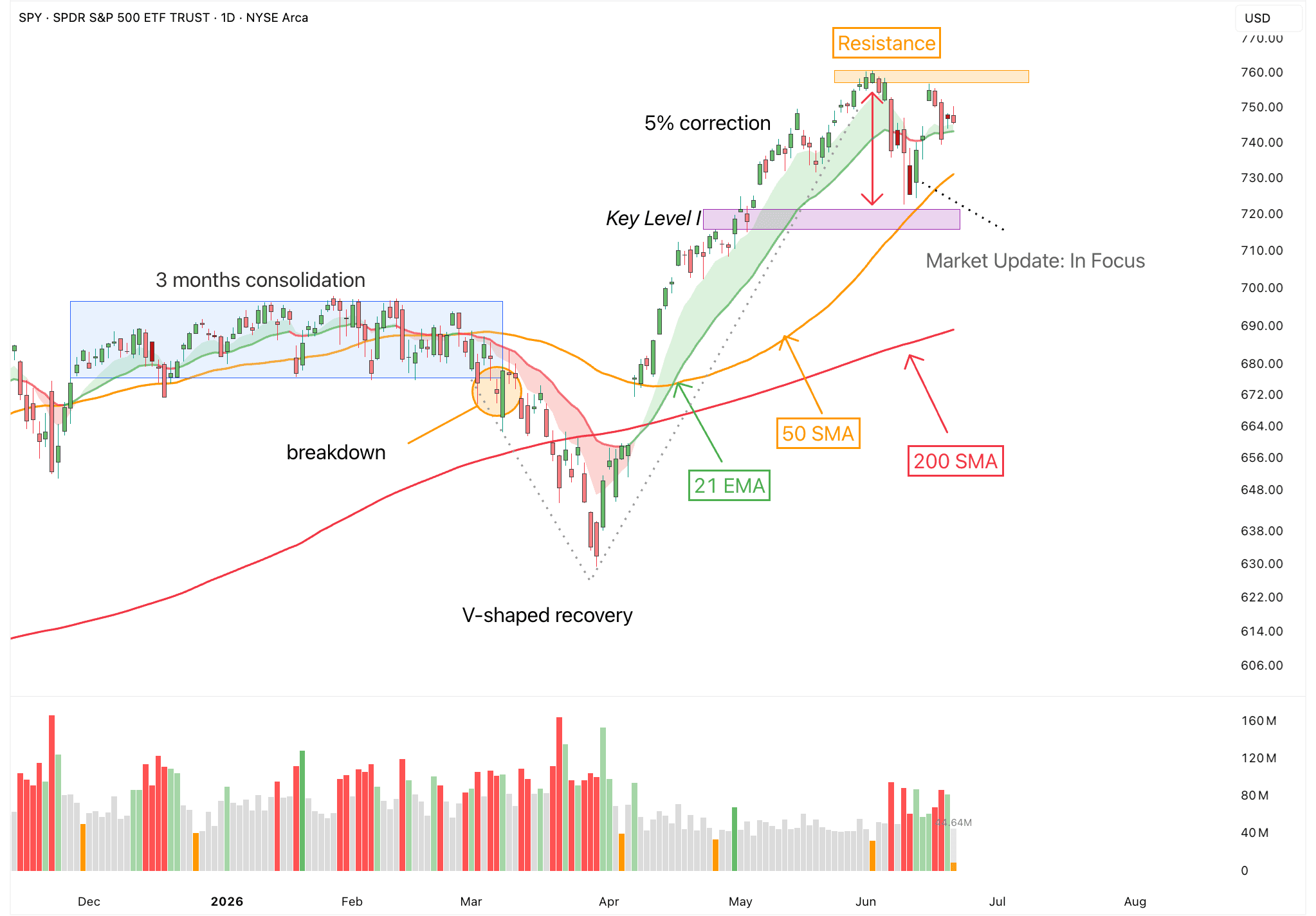

So, the recent pullback played out pretty much as expected. This Marked Update calling for a market bottom was pretty spot on. Now, though, we’re in a consolidation phase. The market is basically in limbo, with no clear direction outside of sideways action. Hence, it’s important to be selective right now.

Unless we break out to new all-time highs, I’d stay a bit more cautious here. The key is for the market to hold and break out of this level. If it starts to roll over, this pullback could still turn into a larger correction. Even so, we’re still in a bull market. And bull markets usually do not die that easily. One correction does not end the whole trend. But they can still hurt, especially if you are too aggressive at the wrong time.

It’s impossible to know exactly what will happen in advance that’s why it is critical to have a scenario plan already prepared. If the market breaks out to new highs, it’s time to get more aggressive again. If it keeps moving sideways, stay patient and selective. If it starts to break down, protect capital. For now, there is absolutely no reason to be euphoric. The goal is not to predict the market perfectly. The goal is to already know what you will do in each scenario.

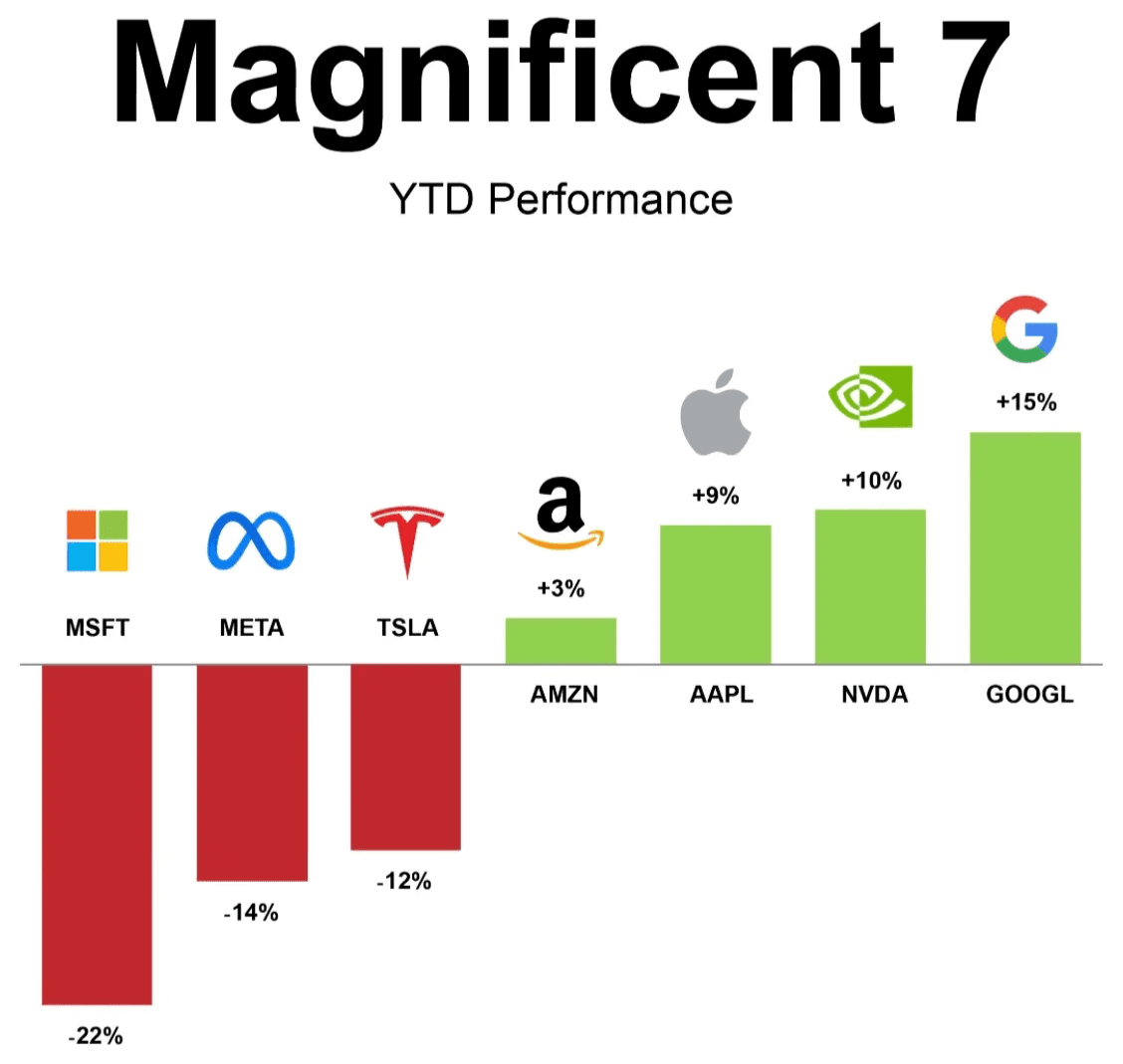

It’s been a pretty mixed year for the Mag 7. They are no longer moving together as one trade. They’ve split into two very different camps. Nvidia, Google, Apple, and Amazon are still pulling their weight, with Google leading the pack at plus 15%. Microsoft, Meta, and Tesla are doing the opposite, with Microsoft down a brutal 22% year to date.

For most of this bull market, the leadership has been extremely narrow. The Mag 7 carried the index, pulled the market higher, and became the main reason the S&P 500 outperformed.

That has changed.

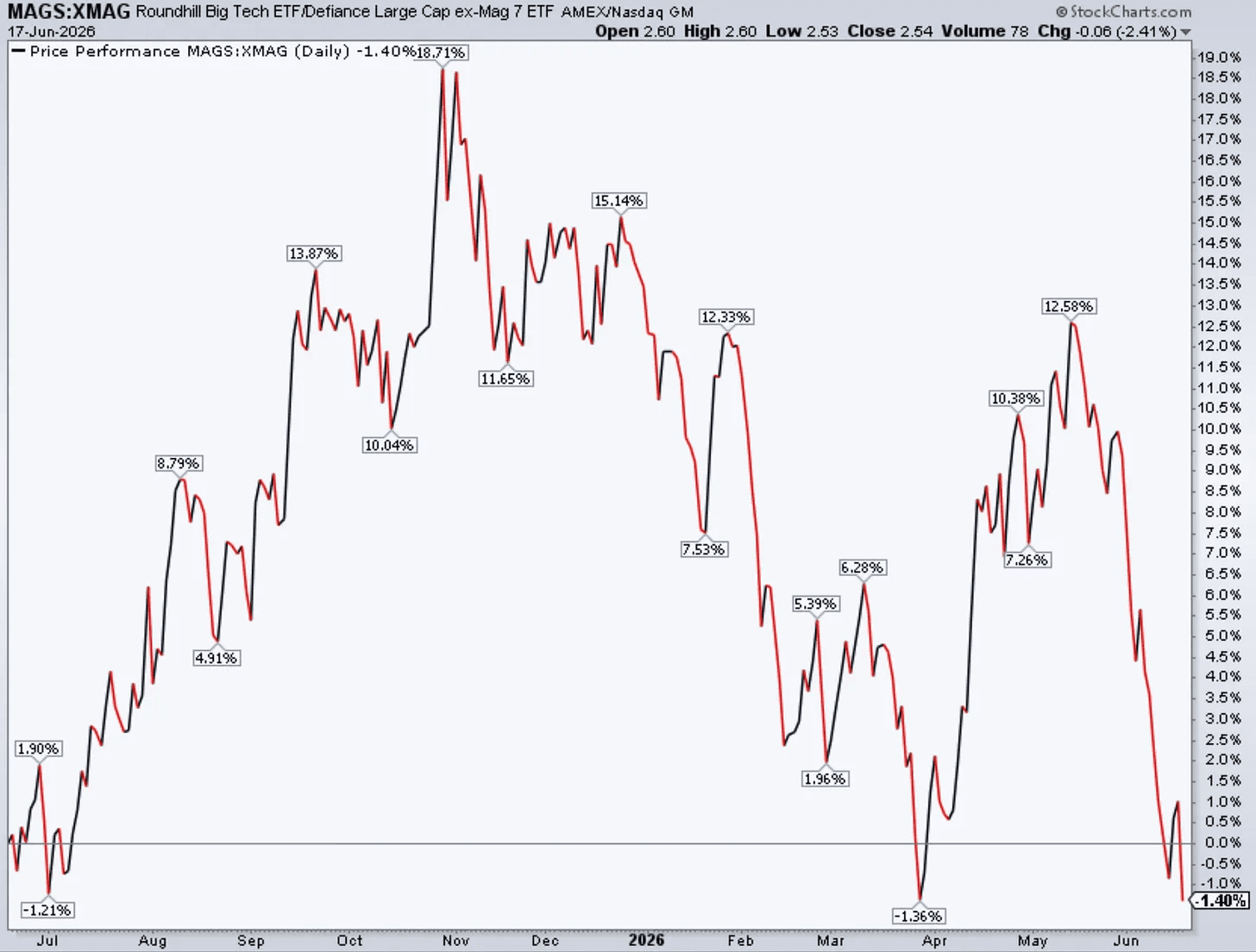

The Mag 7 ETF versus the rest of the S&P 500, the S&P 493, just hit a 52-week low. In simple terms, the average non-Mag 7 stock is starting to outperform the mega-cap names that have driven this entire bull market since 2023.

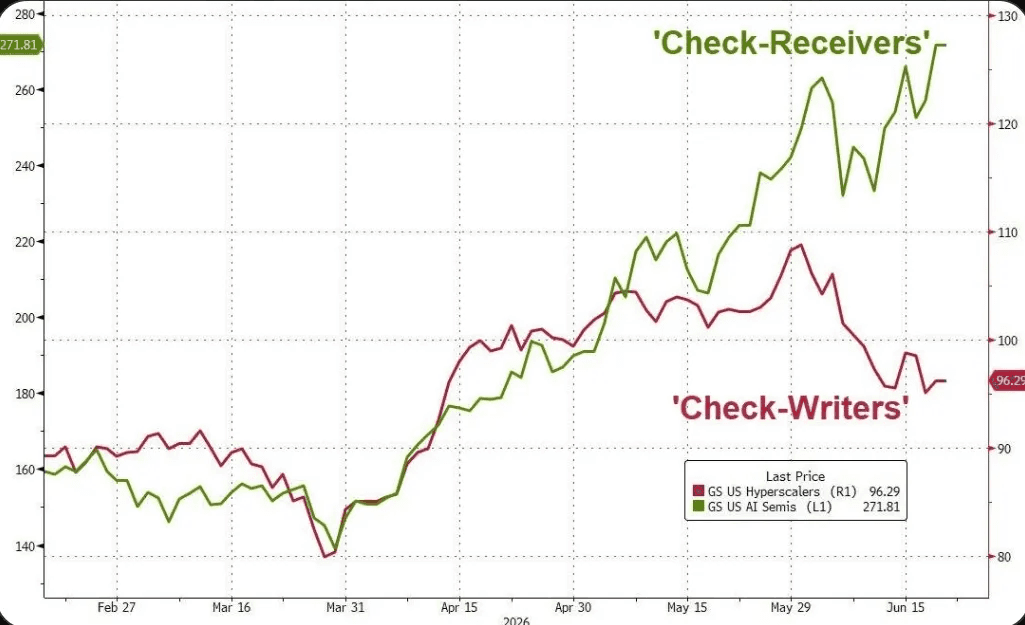

When Meta, Microsoft, Google, Amazon, and other hyperscalers increase capex, that money becomes revenue for the companies selling GPUs, CPUs, memory, servers, networking gear, power systems, cooling, and other AI infrastructure. Investors are rewarding the companies that directly benefit from the spending cycle because their near-term earnings can rise as orders grow. That is why names like ARM, Dell, AMD, Nvidia, Vertiv, Broadcom, Arista, and other AI infrastructure players have been much stronger and why it’s so important to focus on the leading themes.

On the other hand, the companies spending the money and having high capex have become out of favor. They are investing huge amounts upfront funding the AI buildout, but the payoff takes longer to prove.

There is one thing the market hates more than high rates: uncertainty around rates.

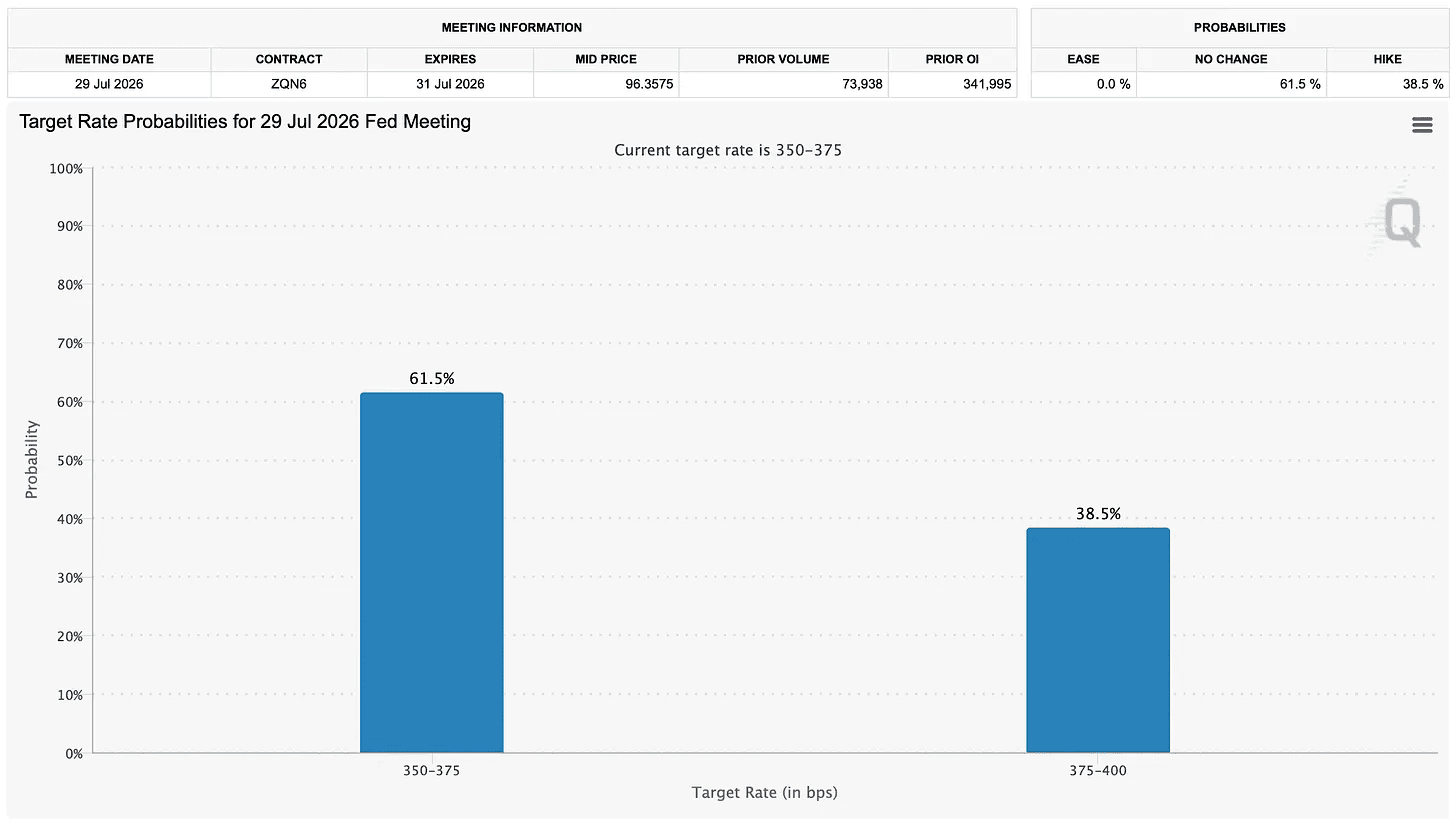

A few weeks ago, investors were still debating when the Fed would start cutting. Now the market is pricing in a real chance that the Fed may have to hike again. A rate cut is now completely off the table for July, while the probability of a hike has jumped to 38.5%. In simple terms, the market is saying inflation may still be too sticky, and the Fed may not be done tightening yet.

This is not a sell signal, but it is something to keep in mind.

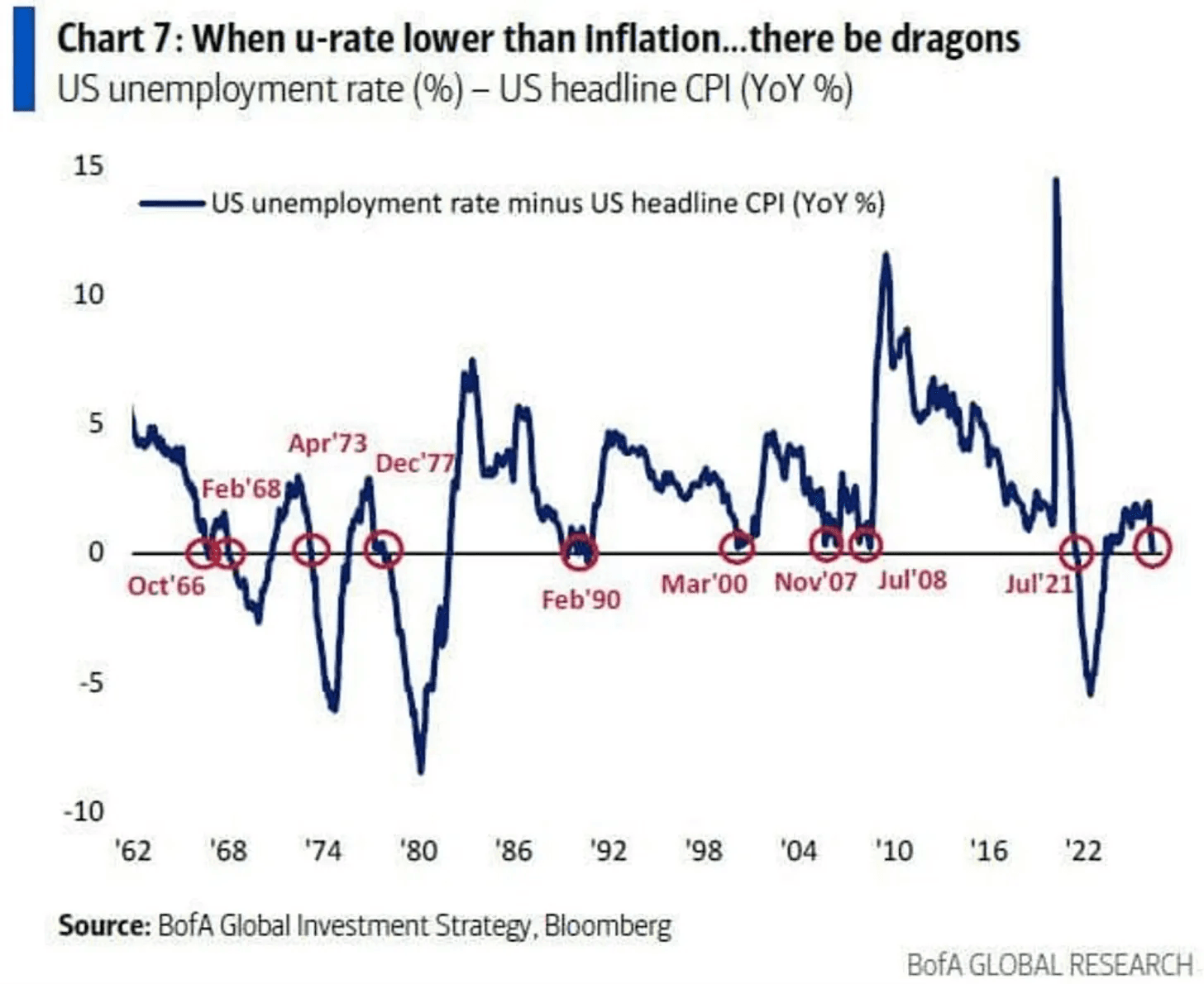

The Fed wants inflation to come down, but inflation is starting to move higher again while unemployment remains low. Low unemployment means people still have jobs, wages can stay firm, and spending can hold up. If prices are also rising at the same time, the Fed may think the economy is still too hot. That makes rate cuts much harder to justify.

The last time this gap collapsed was from 2021 to 2022, when inflation ran hotter than unemployment for 22 consecutive months. The Fed’s answer was 5.25 percentage points of hikes between March 2022 and July 2023, taking rates to 5.5%, the highest level since 2001 which was a pretty tough period for the markets..

We are not there yet. Inflation hit 4.2% in May, the highest reading since April 2023, while unemployment has held steady at 4.3% for 3 straight months. But it’s worth tracking closely.

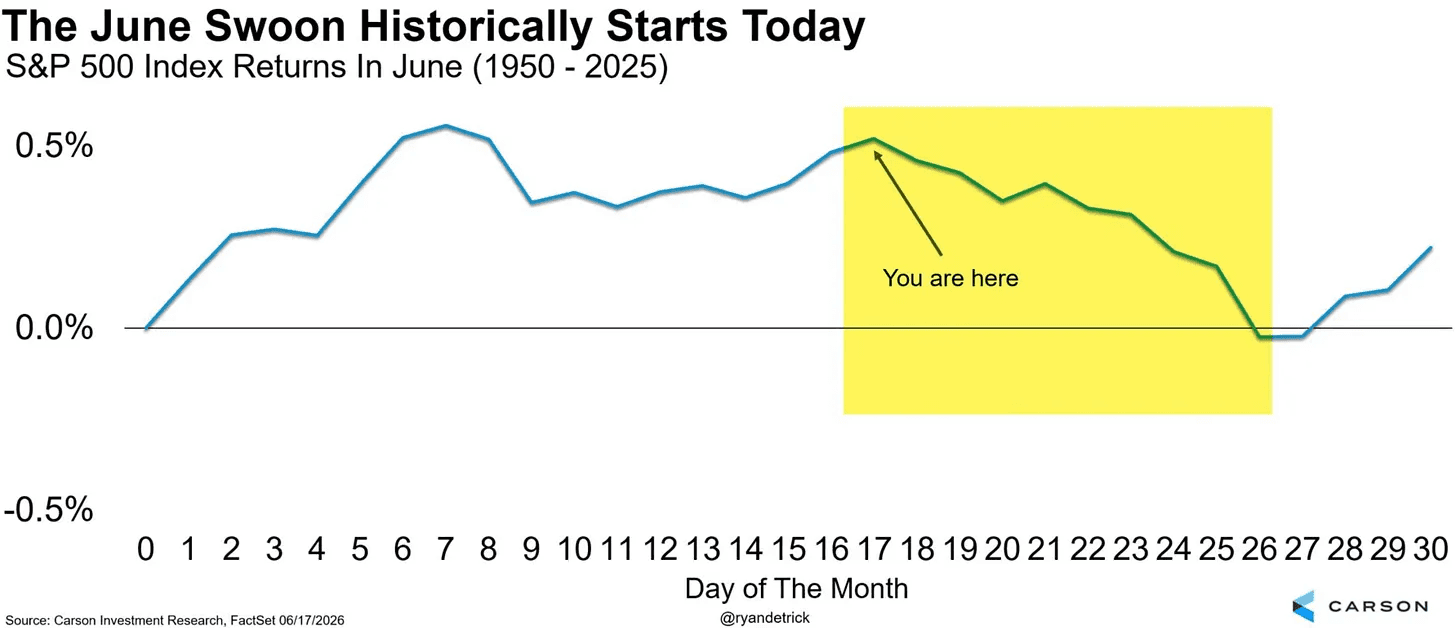

Seasonality is also not on our side for the time being. Since 1950, June 17th has historically marked the start of one of the worst 10 day stretches of the entire year for the S&P 500. Of course, seasonality should never be treated as a standalone signal. Seasonality is most useful when it lines up with what we are already seeing in the market.

Semiconductors are seeing an extreme amount of investor demand right now. Last week alone, US semiconductor ETFs like SSMH and SOXX attracted $4.7 billion in inflows, the largest combined weekly inflow ever recorded. That means investors are not just buying a few individual chip stocks. They are aggressively buying the entire semiconductor theme through ETFs.

On top of that, half of the most traded ETFs in early June were tied to semiconductor stocks, which shows how much attention this part of the market is getting. Money is flooding into the sector at record speed, and that creates strong buying pressure across the whole group. There is a lot crowding built up in the semiconductor trade right now and that eventually needs to cool off a bit.

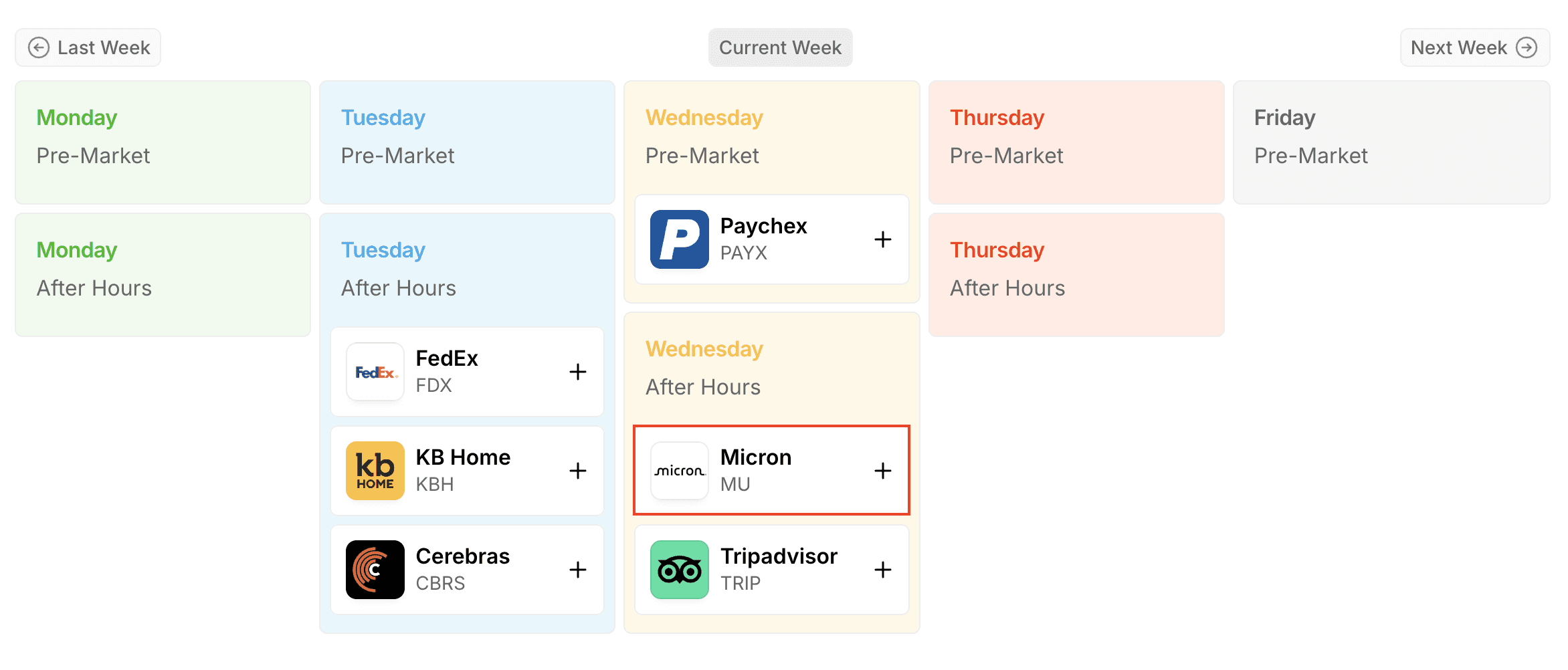

Earnings season is almost over.

But we have more important company to report earnings: That’s Micron.

The commentary and guidance will surely be important to the market here as market participants continue to evaluate how impactful the memory shortage is going to be on the market. Remember, Micron and memory names are major reasons why we’re seeing massive earnings revisions. The earnings estimates from these companies are absurd.

We had SpaceX IPO fears, Iran headlines, FOMC, inflation concerns, a short trading week, a major Monday gap, and plenty of volatility.

Despite all of that, leadership remains intact and the overall market structure still looks healthy. That said, there are a few yellow flags investors should not ignore. For now, those yellow flags are not enough for me to abandon my bullish bias. As long as earnings are holding up, and the AI theme continues to drive the market. But it’s enough to keep your guards. They are a reminder that this is not the time to get careless. That’s when discipline and preparation are absolutely critical.

For now the main job is to stay patient with the names that continue to act well, add supplemental positions where the setup makes sense, and stay ruthless when cutting losers. There are too many strong themes and emerging opportunities right now to keep capital tied up in stocks that are not working.

Previous Updates

View All

- Weekly Market Update: LTCM 2.0

- Market Update: The Trajectory of AI Compute

- Weekly Market Update: Peak Earnings Season

- Market Update: Q2 Earnings Recap #1

- Market Update: DeepSeek 2.0

- Weekly Market Update: All Eyes On the Mag 7

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience