Go Back

Lin

Weekly Market Update: Happy Easter

Happy Easter everyone.

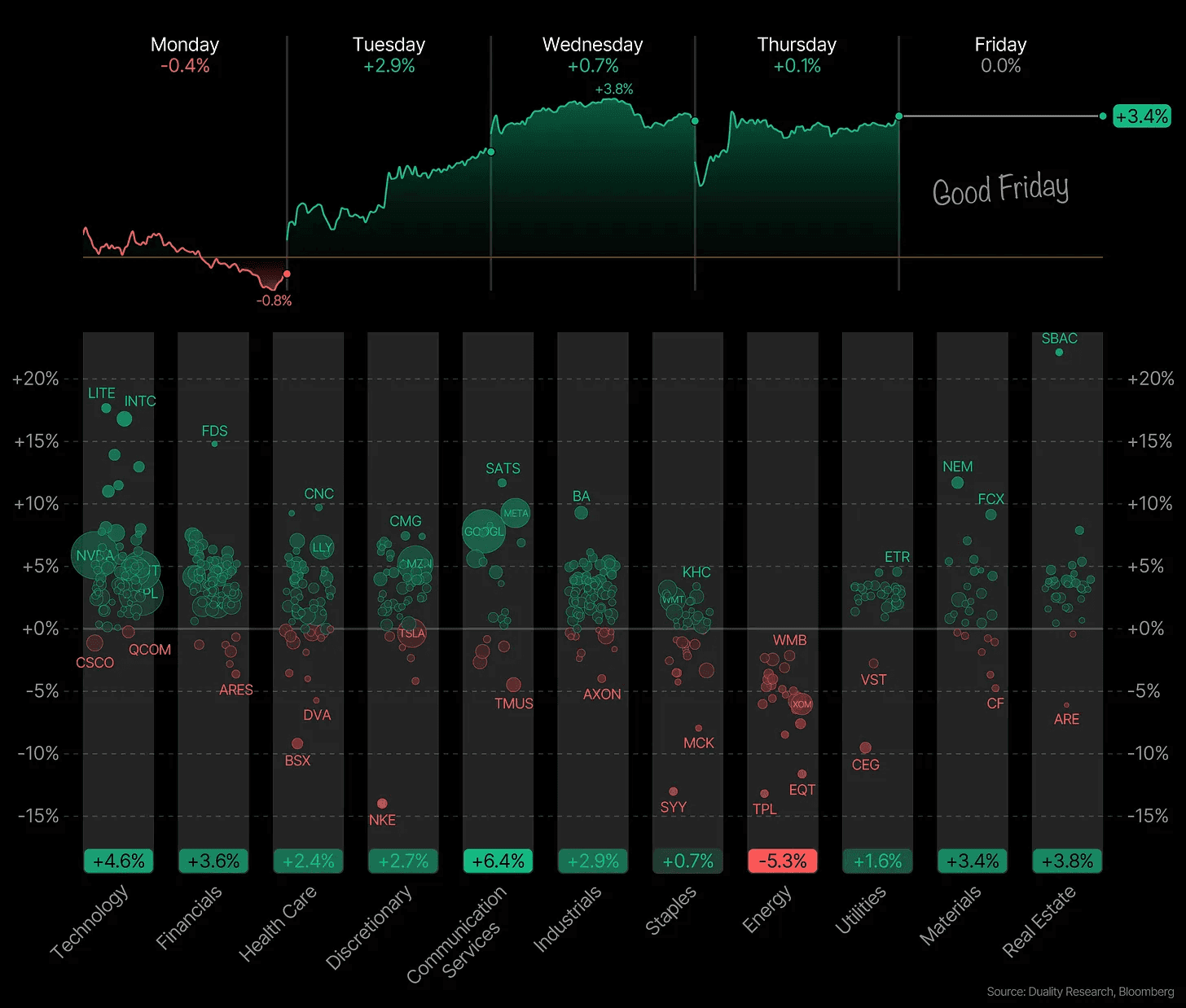

Last week finally gave investors something they hadn’t felt in a while. A bit of hope. Headlines about Iran working with Oman to keep the Strait of Hormuz open were enough to lift stocks off the lows. The S&P 500 even ended the week up after five straight down weeks.

But the news is all over the place.

48 hours. That’s the deadline Trump gave Iran on Saturday morning before a potential escalation in the Middle East. He didn’t say exactly what would happen, but the message was clear. If no deal is made, things could get very ugly.

Just days ago, the Iranian president sounded open to a deal and even talked about ending the war. That optimism helped drive the market higher. Then you get a post like this from Trump, saying time is running out and repeating that “hell will rain down” if nothing happens.

Meanwhile, the U.S. appears to be preparing for something bigger. Large waves of military aircraft are moving toward the Middle East. Transport planes, refueling aircraft, troops, heavy equipment. It is being described as the largest airlift since the conflict started.

On Friday, things escalated further. Iran shot down a U.S. F-15E fighter jet over southern Iran. That is the first manned American aircraft lost in this conflict. At the same time, oil traffic through the Strait of Hormuz is at its highest level since the operation began. Another signal that activity is increasing, not slowing down.

So you end up with two very different pictures. On one side, signals that both sides might want a deal. On the other, clear preparation for escalation. We’ll have to find out which way it goes.

But one thing is certain. Market cycles these days move much faster. The main reason is that information spreads faster than ever. X and Reddit push ideas instantly. Narratives spread like wildfire. A story can go from nothing to everywhere in hours. That, in turn, means more volatility.

But one good week doesn’t fix the bigger picture yet.

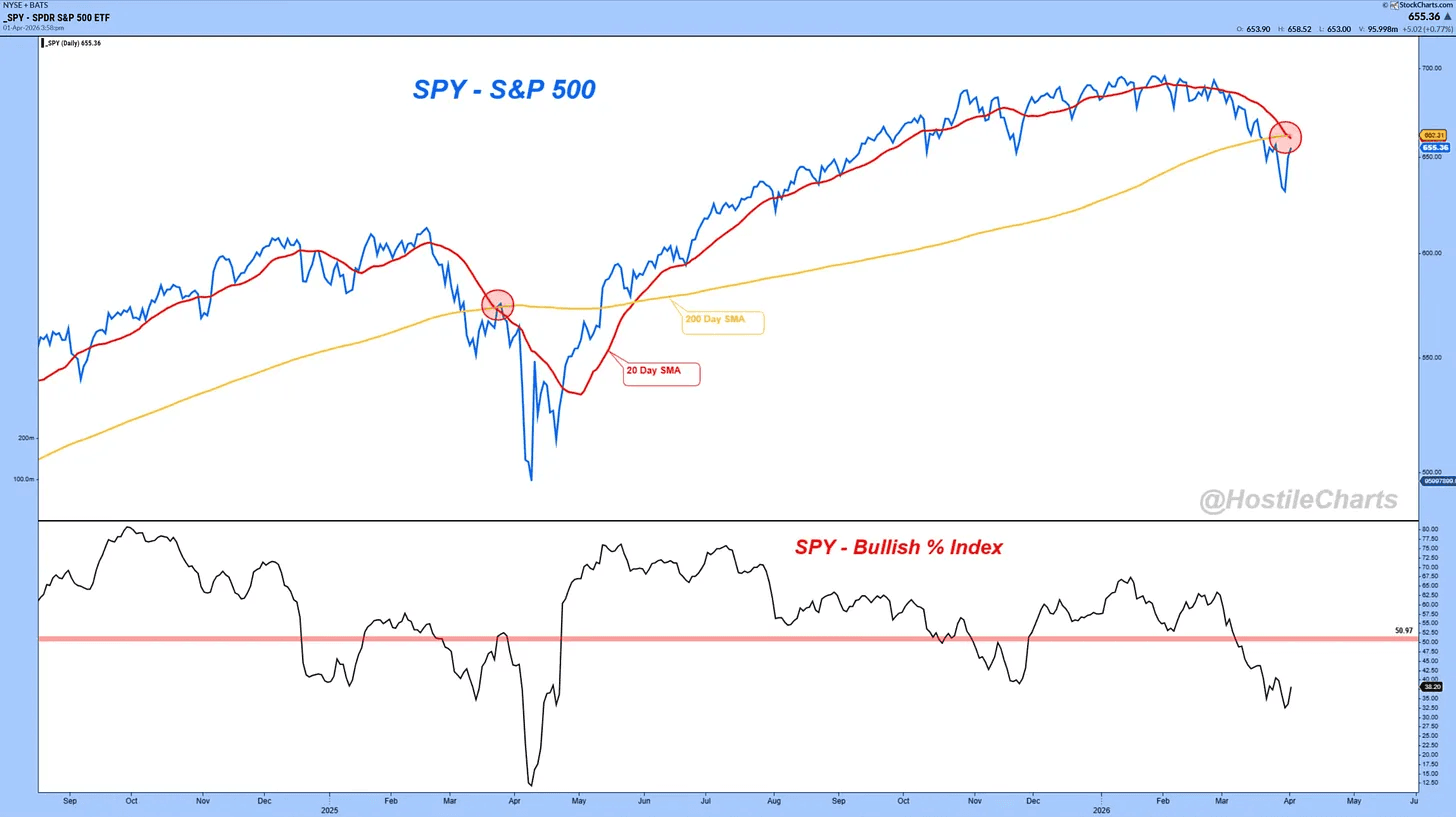

The S&P 500 has now spent 11 straight days below its 200-day moving average going into this week. That’s the longest stretch in about a year. As long as it stays below, the default stance should be caution.

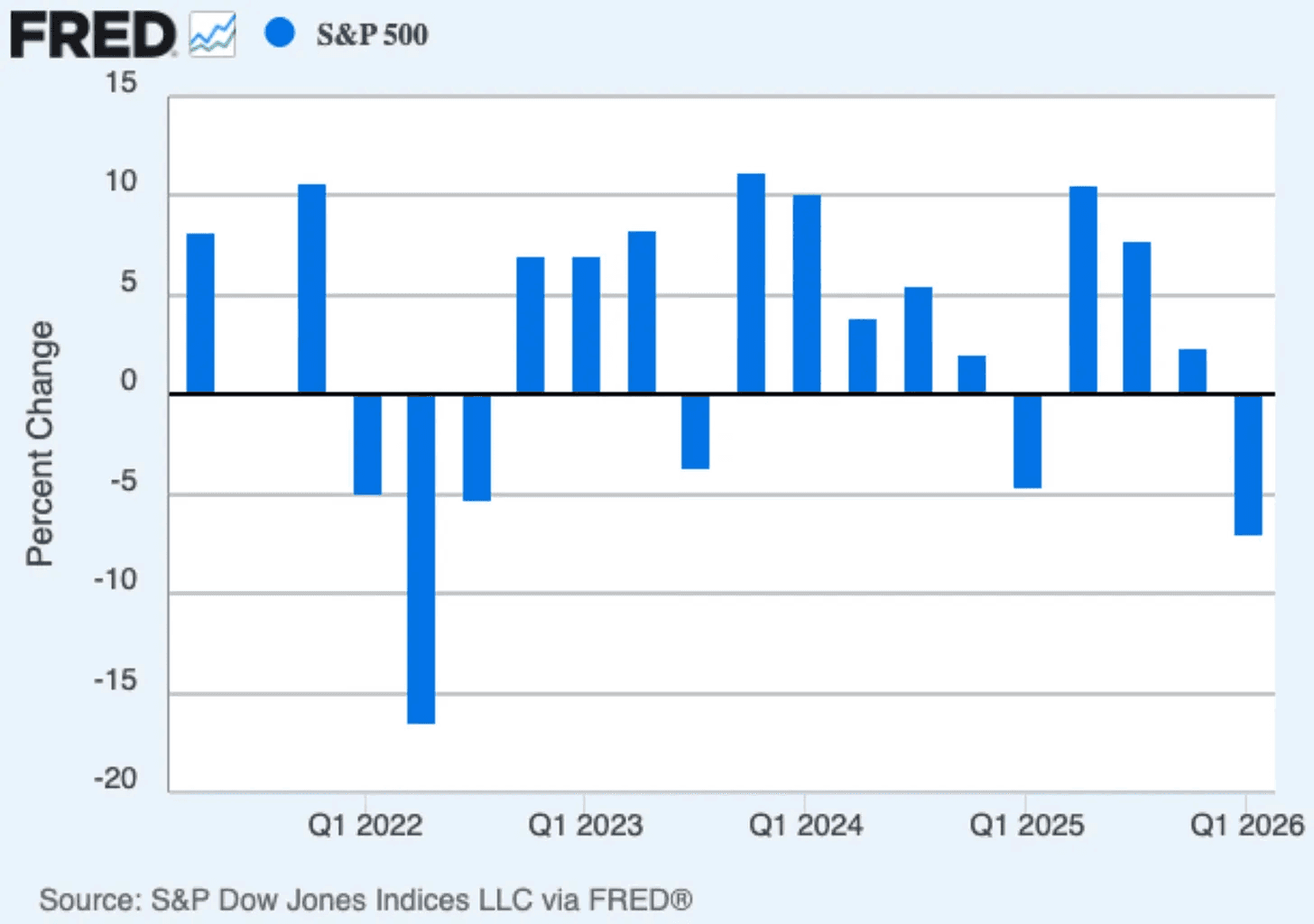

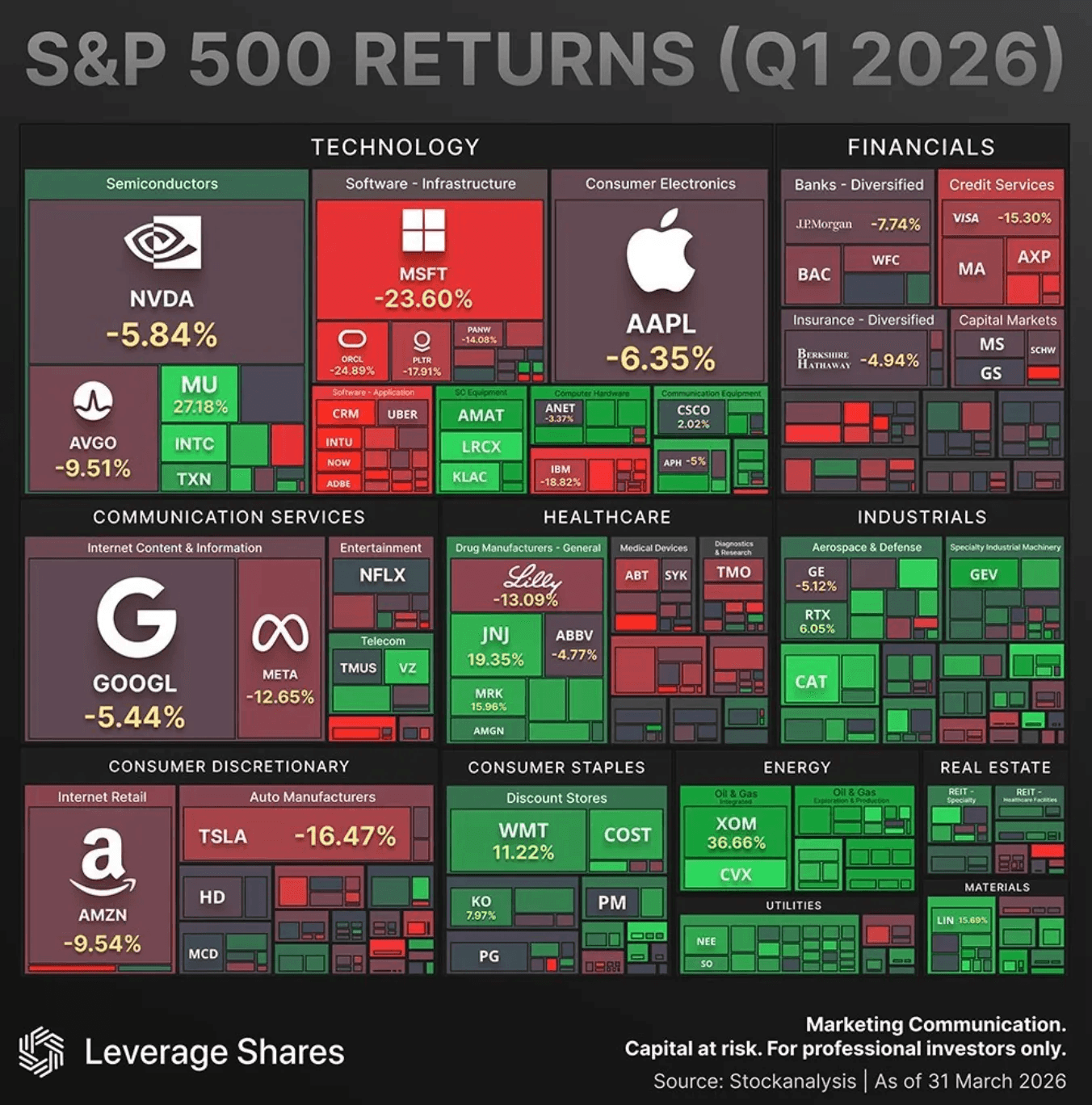

The first quarter is now officially in the books. The S&P 500 ended Q1 down 5.9%, its worst quarter since Q3 2022, when Russia’s invasion of Ukraine shook global markets. After three strong years, the market gave back a sizable chunk of gains in just 90 days.

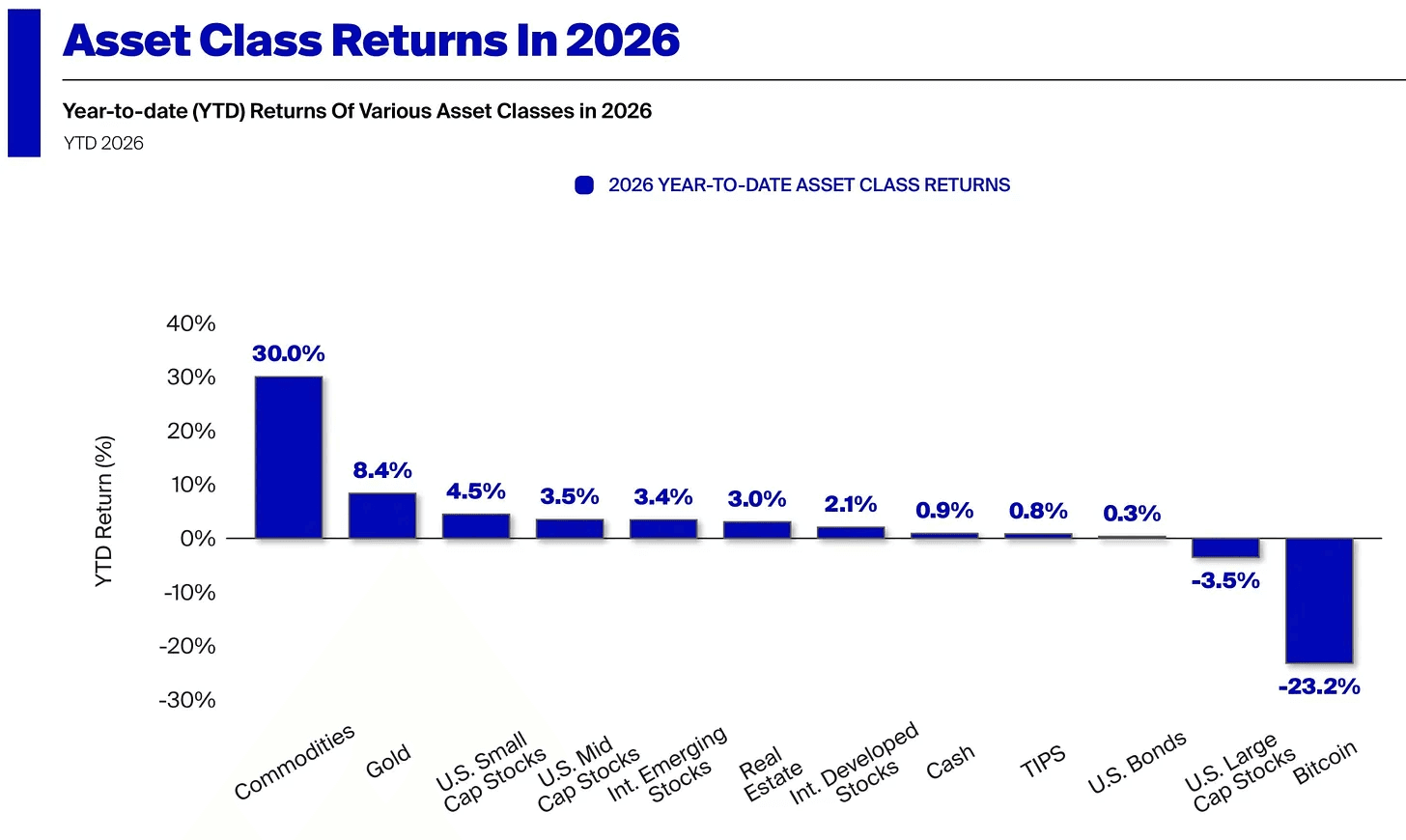

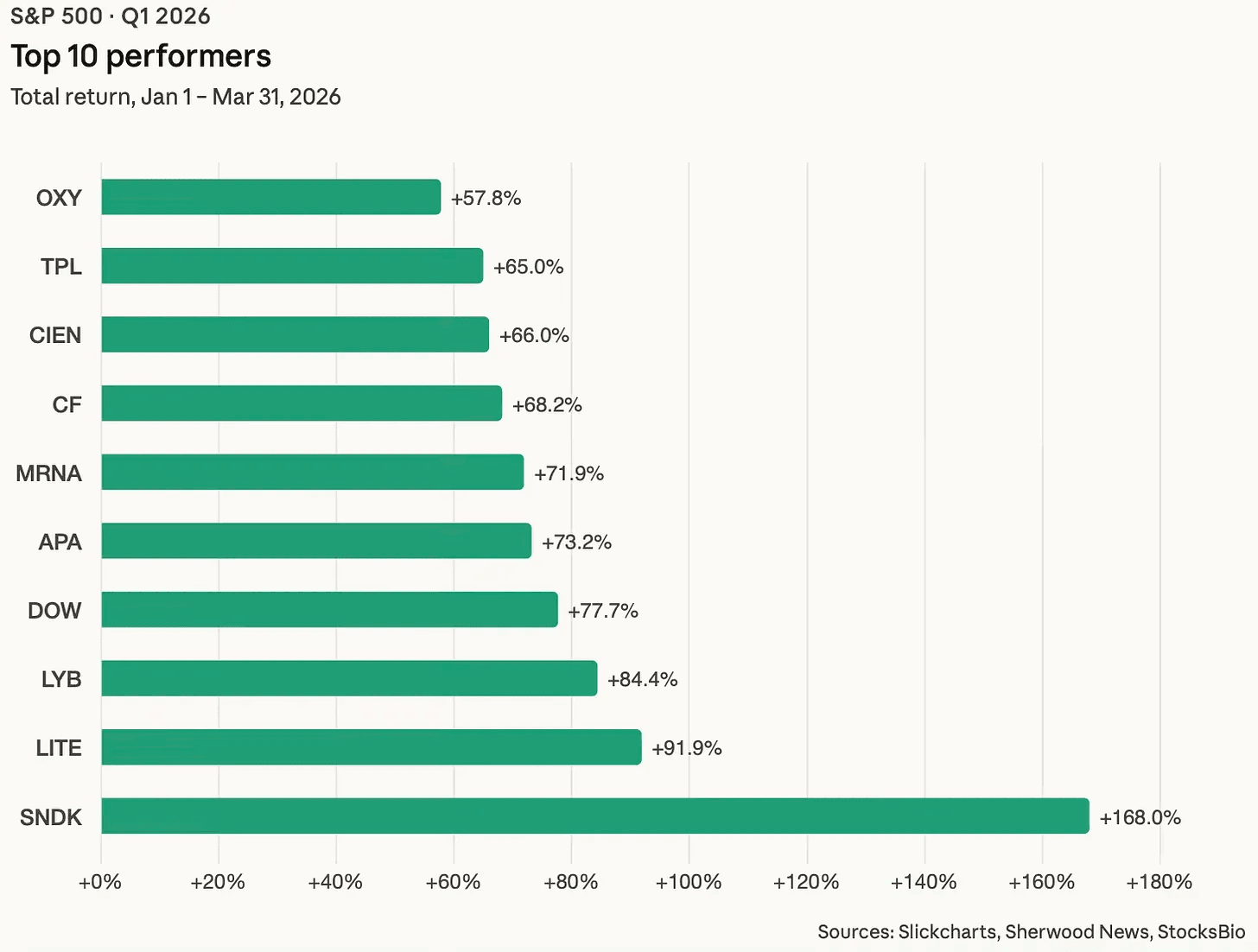

Very few investors would have guessed that Bitcoin would be the worst-performing asset and commodities the best to start 2026. It’s another prime example that the market rarely does what everyone expects.

What really stands out is how different this feels from the last few years. The usual leaders, like big tech and financials, didn’t lead. In fact, they were among the worst performers. At the same time, the areas people had ignored for a long time, like energy and staples, are now standing out.

Megacaps didn’t just underperform. They pulled the whole market down with them.

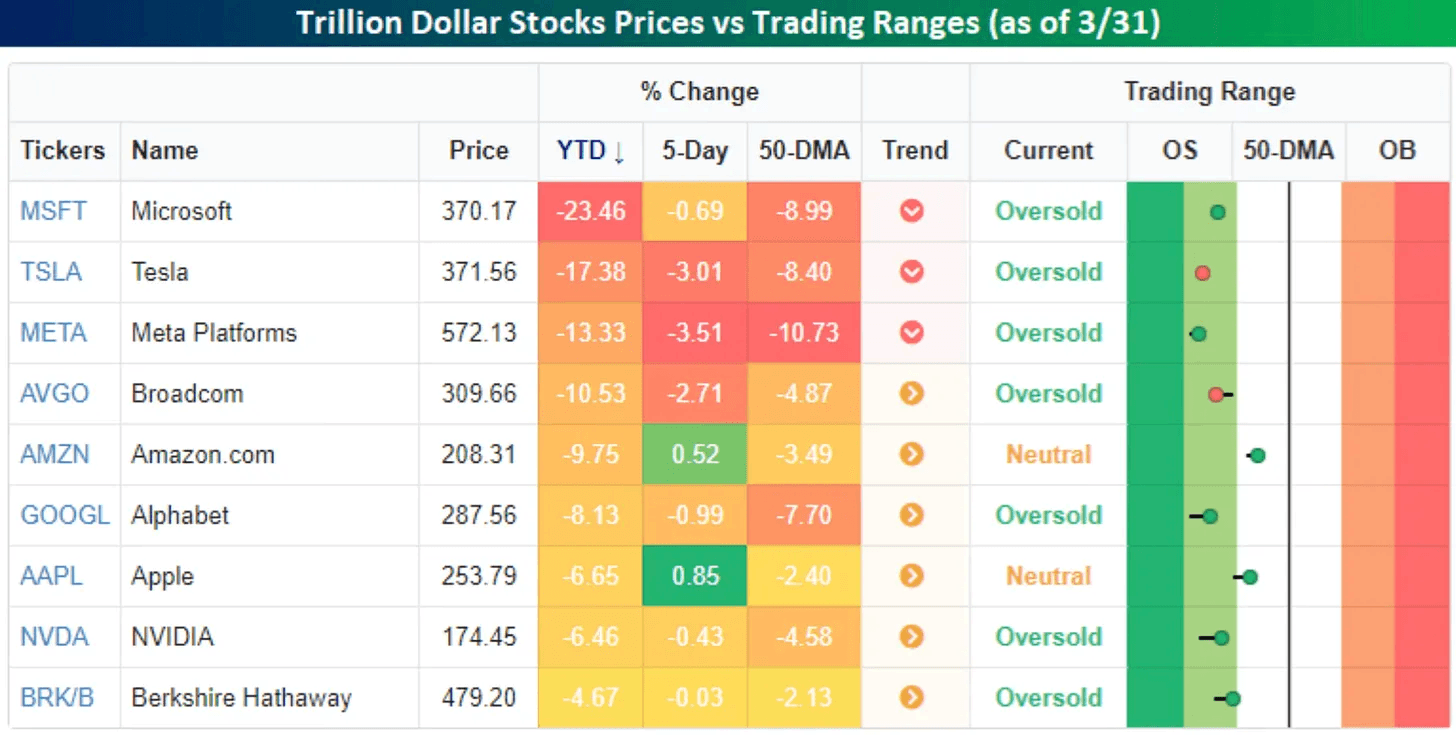

Microsoft is down more than 23% year to date. Tesla is off nearly 17%. Every name in that group is in the red. Most of them are already in oversold territory, which shows how fast this cycle has played out.

But that’s also where things start to get interesting.

If you’re a long-term investor, it could make sense to start paying attention. Microsoft is back to where it traded in 2021. The same goes for Tesla. Nvidia is now trading at one of its lowest forward multiples in years.

Not much has changed except for positioning and sentiment. These are still great businesses.

There’s an interesting split under the surface.

Small and mid-cap stocks are still up this year. The weakness is really coming from the top. A handful of mega-cap names are pulling the whole index down, and it’s been a tough year for growth stocks.

Since those names are heavily owned and sit in a lot of portfolios, it makes the drawdown feel worse than it actually is.

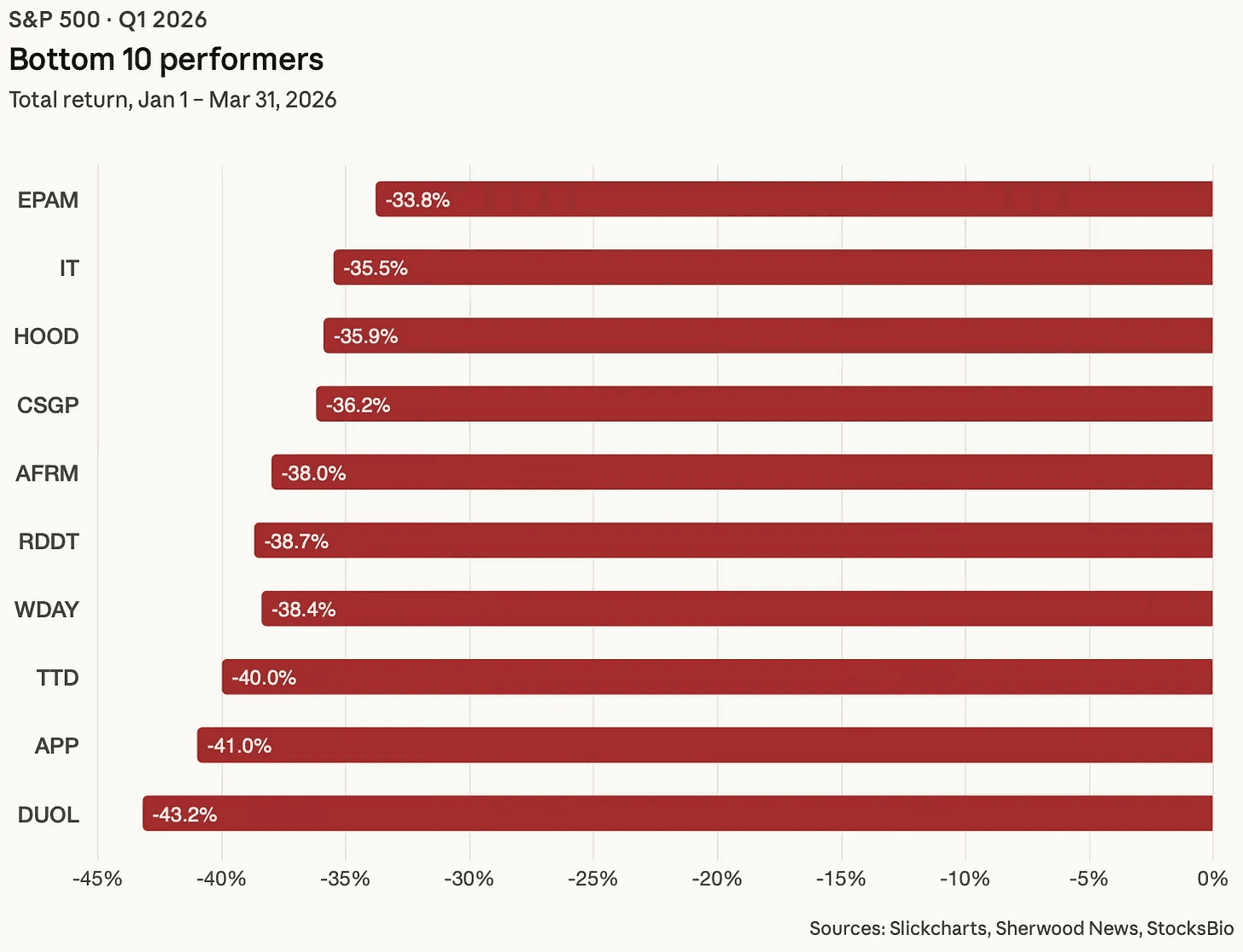

Some of the biggest winners from 2025 got hit the hardest. Software names made up more than half of the 20 worst performers in Q1.

Trade Desk fell 40%. Workday dropped 38%. Adobe declined 31%. Salesforce lost 30%. And AppLovin, which had surged 108% last year, flipped to the worst performer in the index this quarter, down 41%.

This is a perfect example of how powerful narratives are in the market.

Nothing fundamentally broke overnight. These are still the same companies, with the same products, serving the same customers. But the story around them changed. And when the story changes, price follows.

Last year, the narrative was simple. Software is unstoppable. High margins, recurring revenue, huge demand. Investors were willing to pay almost any price for that story. AI enters the picture, and suddenly the question is not “how big can these companies get,” but “how much of what they do can be replaced?” Same businesses. Totally different framing. And that shift in perception is enough to take a stock down 30 to 40% in a few months.

Markets don’t just price fundamentals. They price expectations about the future. And expectations are driven by stories people believe.

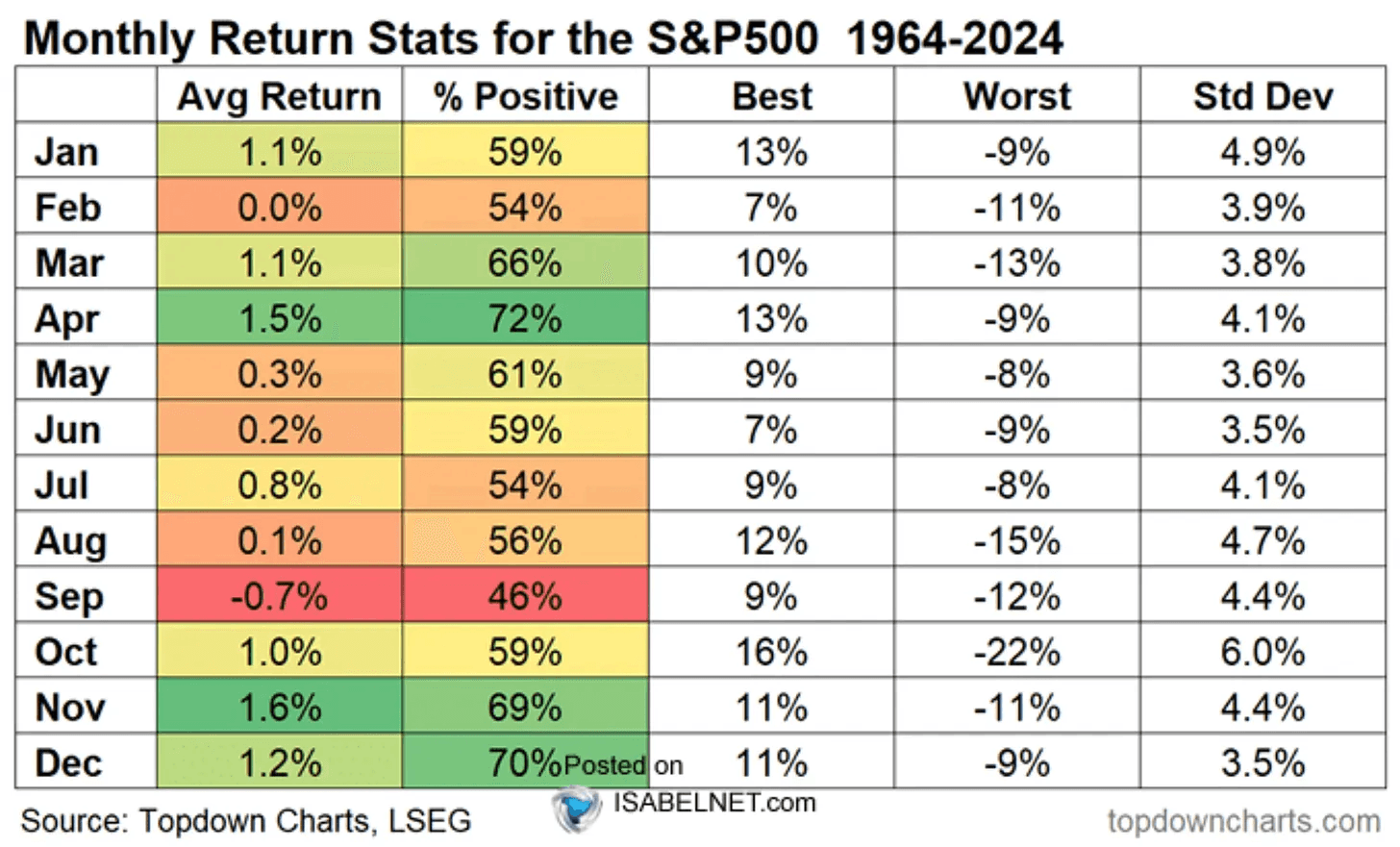

The good news is, if you just look at history, April tends to be a pretty good month.

Since 1964, the S&P 500 has averaged about +1.5% in April and finished higher 72% of the time. That’s the best win rate of any month. April has been one of the most consistently positive months for stocks.

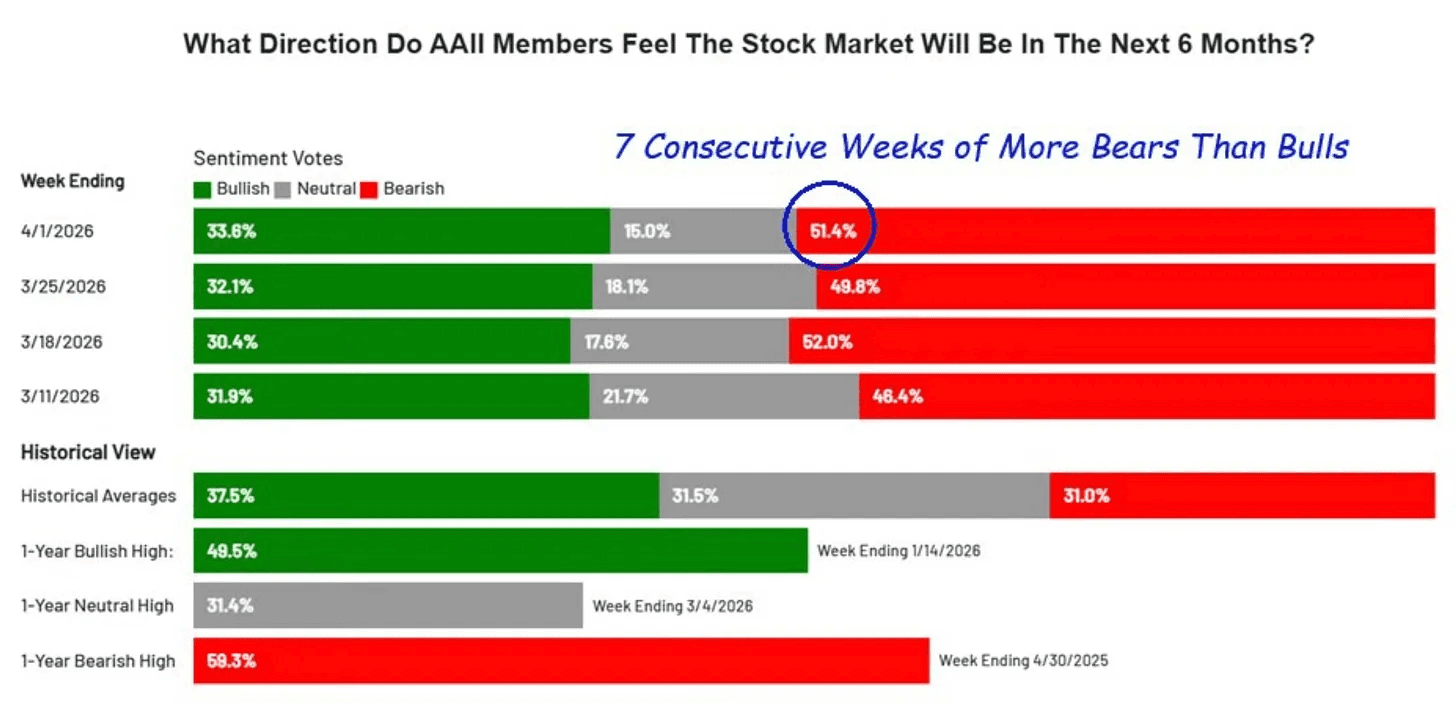

Sentiment is already deep in the basement. There have been seven straight weeks with more bears than bulls among individual investors. The last time bearishness was this persistent was during the Liberation Day tariff fallout in 2025, which turned out to be a buying opportunity.

Given everything that’s happened, the actual damage to stocks has been surprisingly contained.

A war in the Middle East. Oil above $100. An AI disruption narrative rattling every software company. Rising rates. Big tech rolling over. And the S&P 500 is down about 4% for the year.

For the first time in weeks, there’s a real reason to be a bit more optimistic. The market is starting to show early signs of stabilizing.

That said, this is not the moment to go all in. Some of the strongest rallies happen during corrections. Until we reclaim key levels like the 200-day moving average and start a new uptrend, it still pays to stay cautiously optimistic. You’re still in a market where the odds are not in your favor, especially with the current geopolitical backdrop.

Because this environment is not normal.

In a typical market, prices move based on earnings, growth, and valuations. There can still be volatility, but there is usually some logic behind the moves. Right now, the main driver is uncertainty. Headlines about Iran, oil, and escalation can move the market instantly. One tweet can change everything within minutes.

That makes the market less reliable. You can get strong green days or even a few good weeks, and it can feel like you’re missing the bottom. But a lot of that is just short covering or temporary relief. In this kind of environment, those moves can reverse very quickly.

The positive side is that this kind of environment also creates opportunity.

When investors get scared, they don’t sell carefully. They sell everything. Good companies or bad companies, it doesn’t matter. They just want out. That’s where the opportunity comes from.

There are a few sectors and companies that could start to look interesting going into Q2. More on those soon. Earnings season is kicking off again, and we’re finally getting real fundamental data that reflects what’s actually happening inside businesses.

Previous Updates

View All

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap