Go Back

Lin

Weekly Market Update: The Grand Finale

It was a short trading week, but it certainly wasn’t a boring one. The S&P 500 was up 1.1%, and the Nasdaq gained 1.5%. That made it the best week for both since January 9. The Nasdaq also finally snapped a 5 week losing streak.

The big moment came on Friday. The Supreme Court struck down one of President Trump’s tariff plans, and that was enough to get buyers back into the market. Trump later announced a new 10% global tariff, which the markets largely ignored.

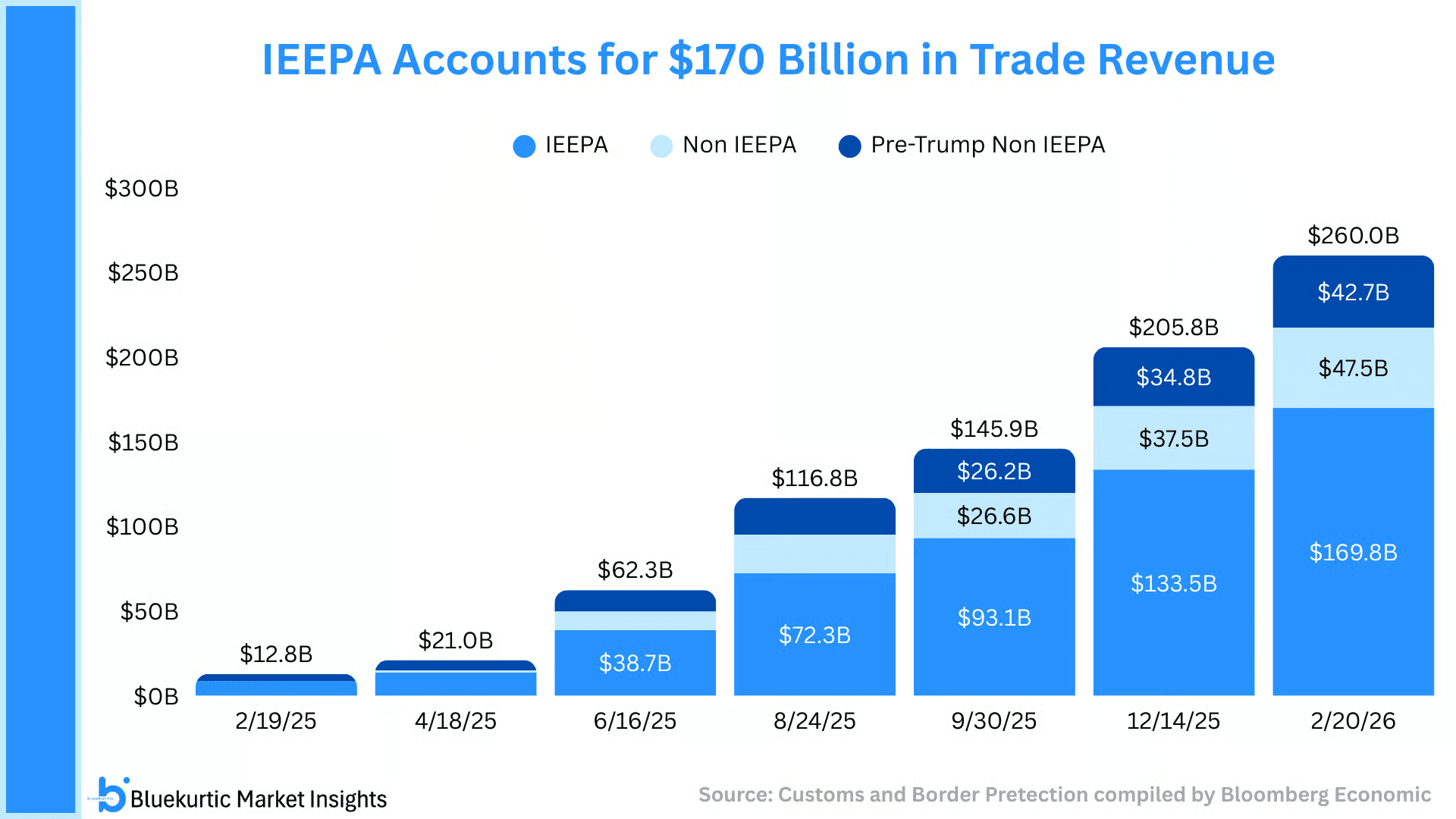

With the Supreme Court ruling the IEEPA tariffs imposed by President Trump illegal, the administration now faces up to $170B in potential tariff refunds. Over 1,500 companies have already filed trade court claims to secure their place in line.

On the upside, there is an immediate reprieve from current tariffs, which could act like a temporary tax cut for businesses. On the downside, any tariffs imposed under these other statutes are more likely to stick. But the administration has several other tools it can use to re-impose similar tariffs, but those will take time.

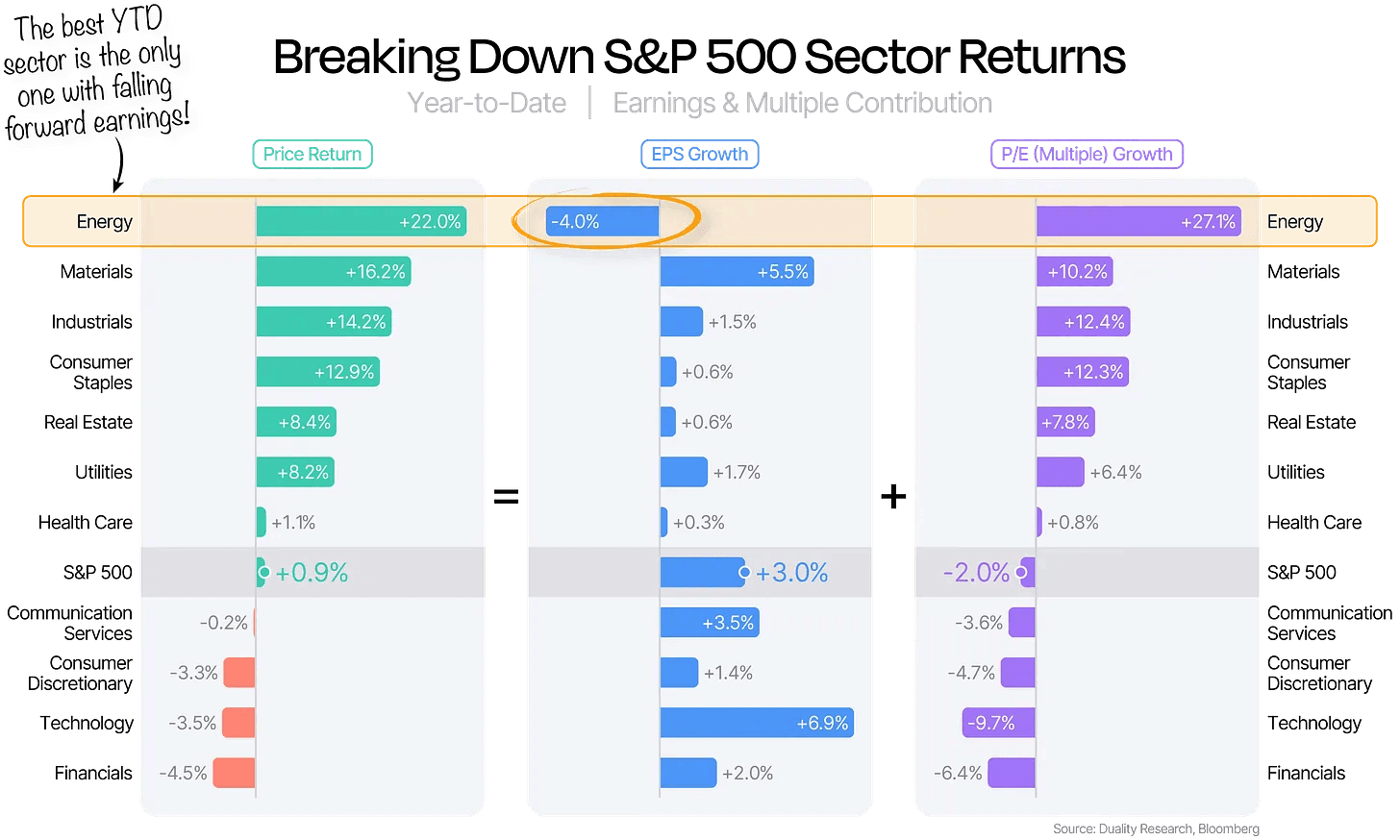

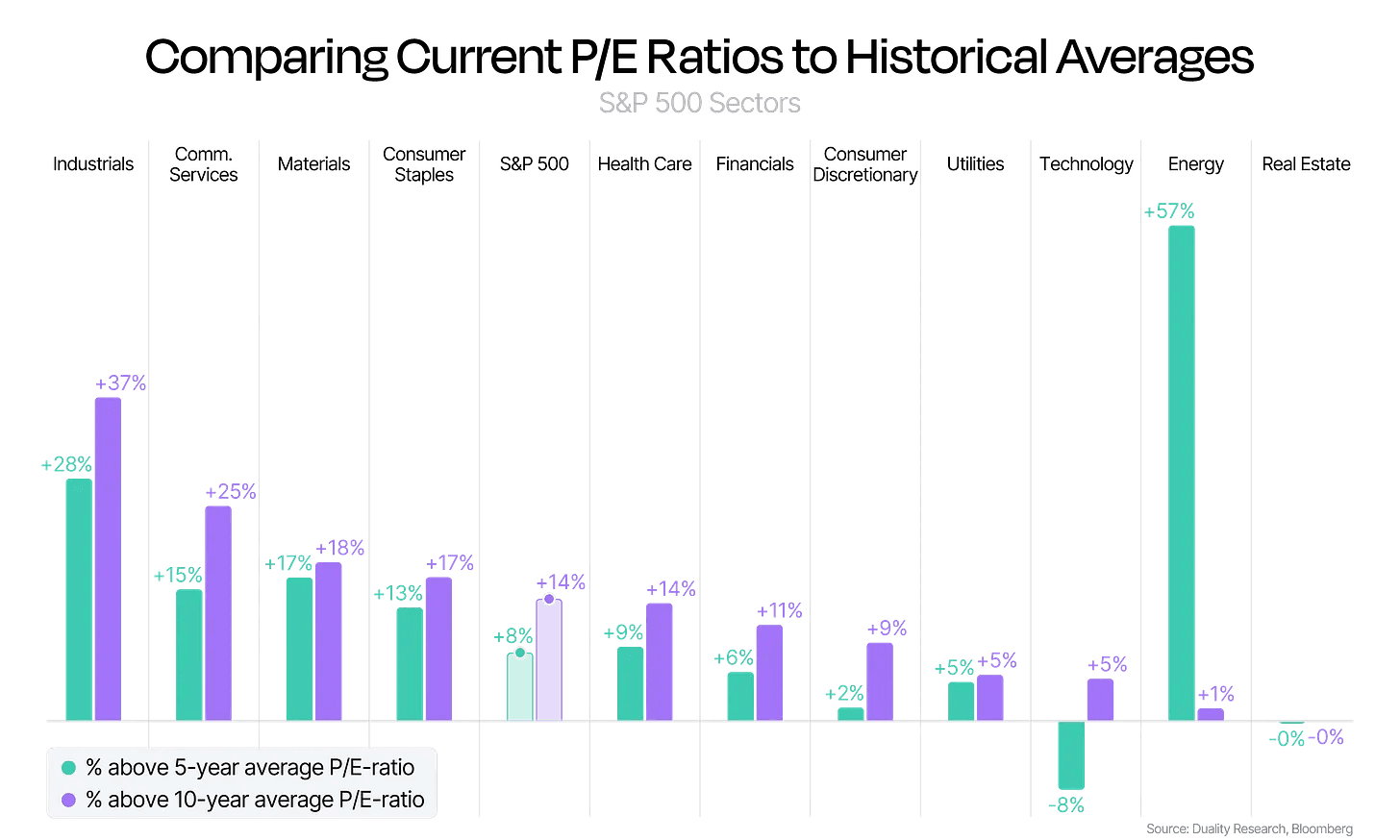

Energy is the best performing sector this year.

This the best start to a year over the past 25 years for the energy sector. However, the irony is that it’s the only sector with negative earnings growth.

Meanwhile, The worst performing sector are financials.

I don’t like to see energy leading bull markets. Financials lead new bull markets. They don’t lag. The financial sector is traditionally the first sector to lead a new market move. Energy is traditionally the last.

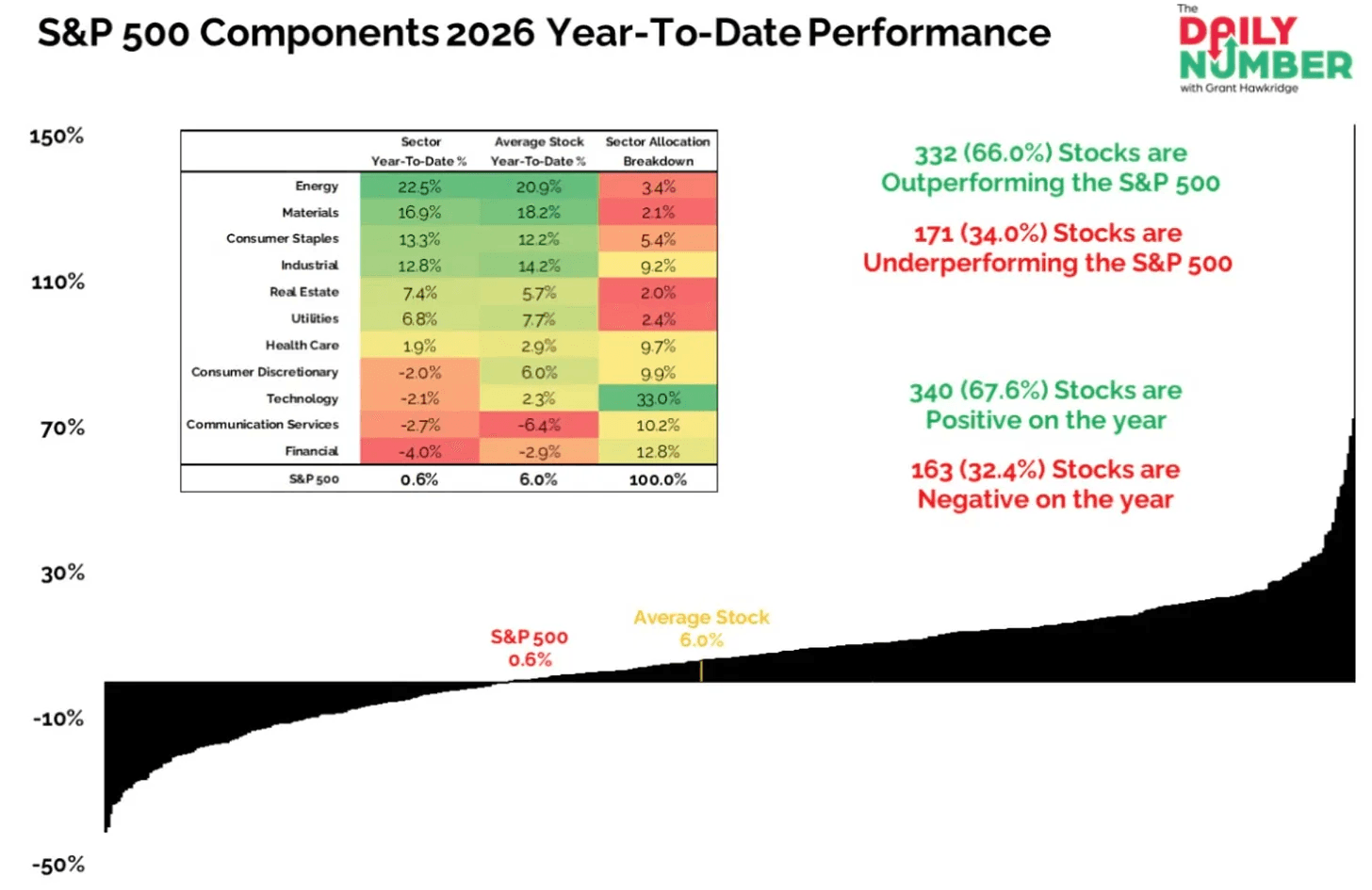

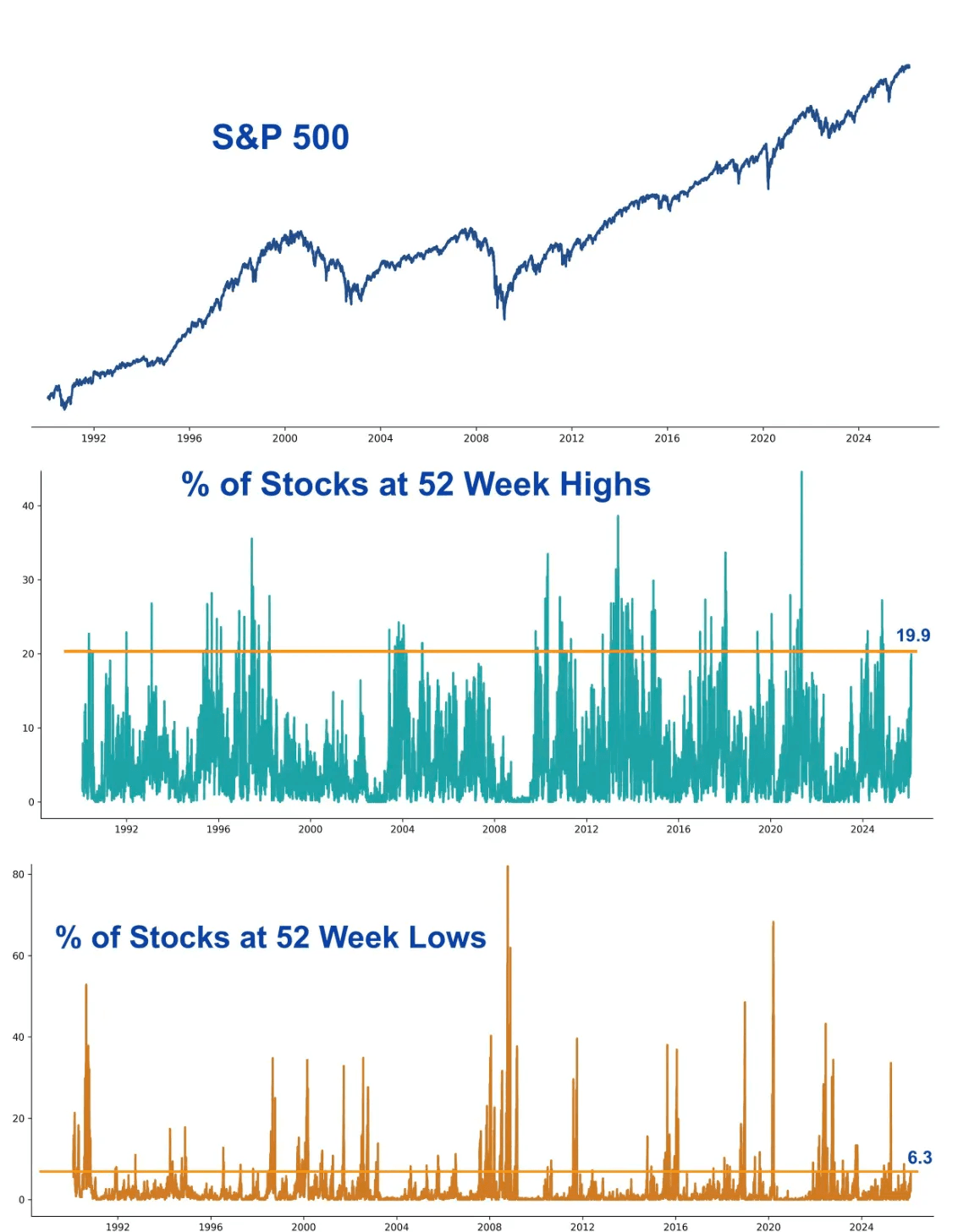

The S&P 500 is basically flat on the year.

But if you are only watching the index, you are missing most of the action.

In fact, The average stock in the index is up 6.0% in 2026. About two-thirds of S&P 500 stocks are positive on the year, and two-thirds are actually outperforming the index itself.

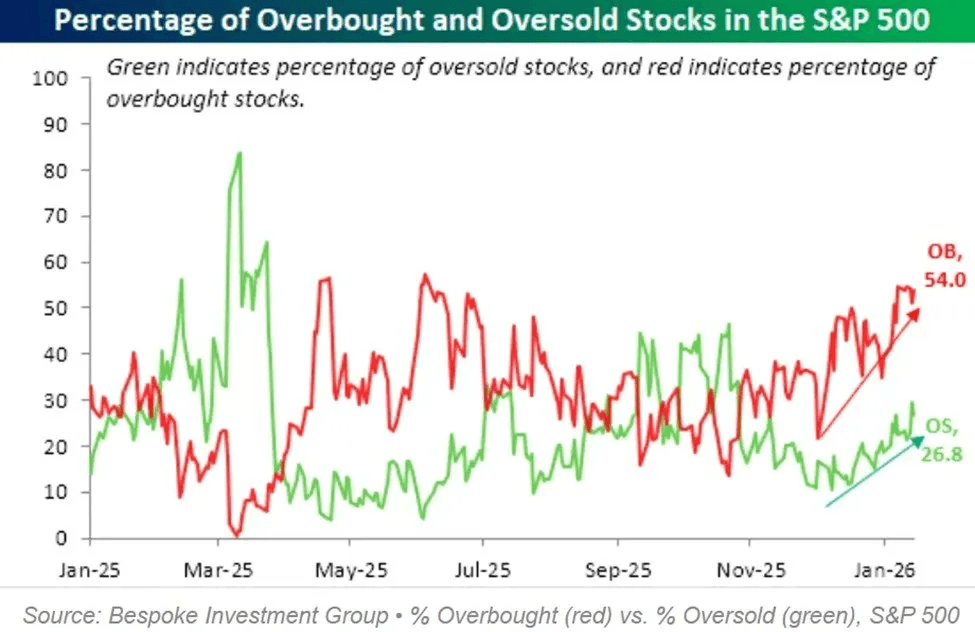

54% of S&P 500 stocks are currently overbought, which is the highest percentage since June 2025. At the same time, 27% of names are oversold, the highest level since October.

Normally, when a lot of stocks are overbought, very few are oversold. And when many are oversold, very few are overbought. They usually move in opposite directions. Right now, both are high at the same time. That means many stocks are being aggressively bought while many others are being aggressively sold.

It shows the market is very bifurcated, emotional, and volatile.

Perhaps the most unusual data point is this. Nearly 20% of S&P 500 stocks are at 52-week highs, while 6.3% are at 52-week lows at the same time. It’s incredibly rare to see such an extreme divide.

The big question is how long this can last. Broad participation is a good thing, but the index still depends on its biggest names. Right now, the megacaps are mostly on the sidelines. But tech stocks make up more than 40% of the S&P 500, and most of them down on the year. That is a lot of weight for the rest of the market to carry.

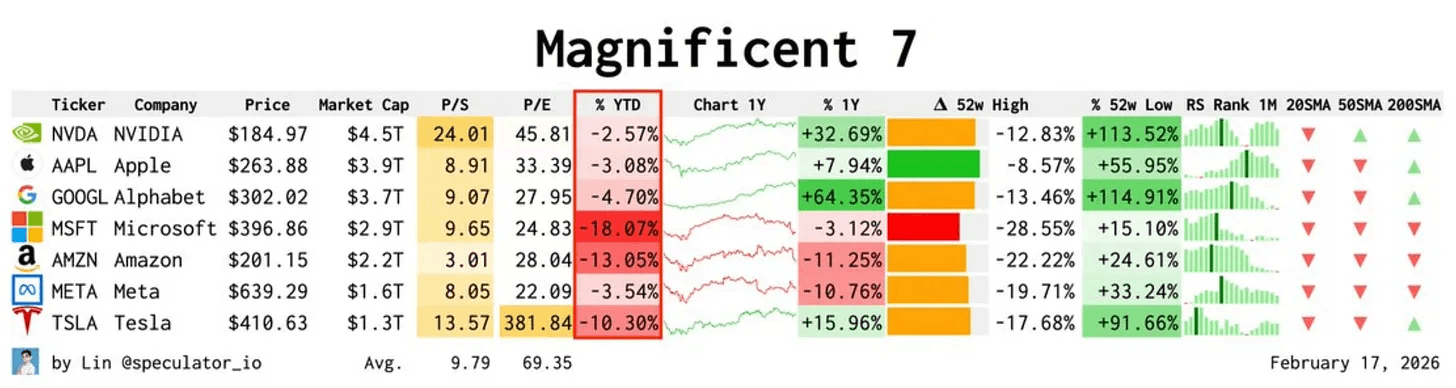

Here’s a number that really puts things in perspective. All 7 members of the Magnificent 7 are negative on the year right now. That does not happen often.

The last time this happened was March 2025, after the tariff announcement. Before that, you have to go back to 2022, when the group sold off hard during the Fed’s aggressive rate hikes.

The S&P 500 will continue to struggle, if the Mag 7 don’t start to turn around.

The $MAGS ETF holds only the Mag 7 stocks and T-Bills. Because of that, it is a clean way to see how the Mag 7 are doing compared to the rest of the market. Right now, it is sitting at a key inflection point right at the 200-day moving average. This is the make or break moment.

Valuations have also come down a lot. The Mag 7’s forward P/E has dropped from nearly 32 a year ago to 25.8 today. Still not cheap, but a much more reasonable entry point than where this group was trading at its peak.

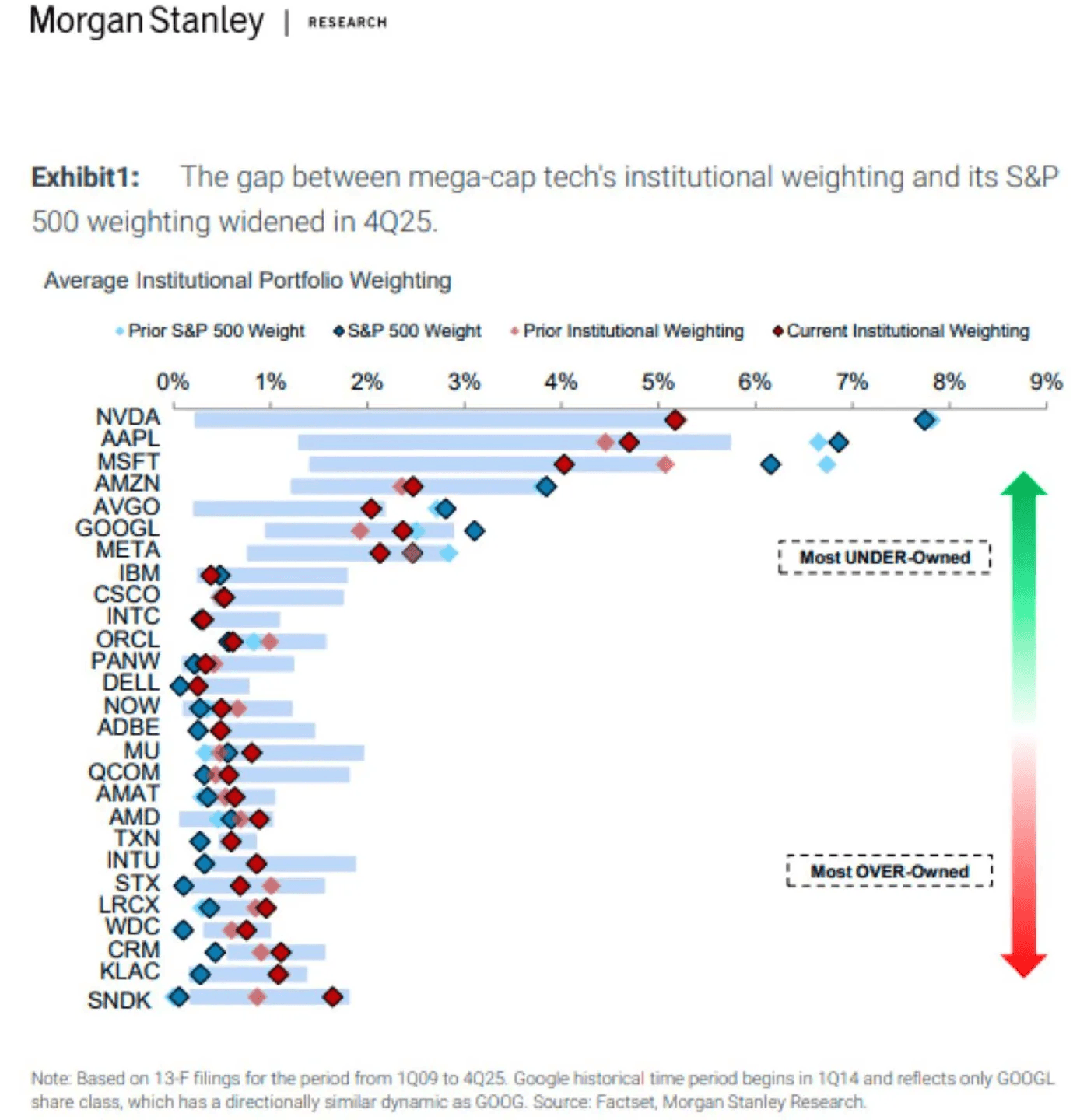

And perhaps most telling. According to Morgan Stanley, mega-cap tech is now the most underowned it has been in 17 years. At the top of the list is Nvidia. This will be very interesting going into next week.

This is the grand finale of earnings.

To start, we have Nvidia, the most important stock in the market. I expect a strong beat and raise quarter with very bullish commentary. The capex numbers we have heard from almost every company have blown away expectations, and most of that money is flowing straight to Nvidia.

The reaction will be critical. If a big beat and raise is bought, that could be a major signal that there is still strong appetite for AI names. If not, it would be a major red flag in my view.

Nvidia’s earnings could very well be the next big catalyst for the market. For months, we have not made much progress. Since November, we have only seen a volatile, directionless market. This is not a supportive environment for most growth and momentum names. And there is really not much to do unless we get a clear direction, either way.

But whichever way it goes, it will continue to be critical to avoid sectors that are likely to be disrupted by AI and focus on the ones that will benefit. That divide is only getting wider. AI is not lifting the whole market. It is rewarding a small group of companies and pressuring others at the same time.

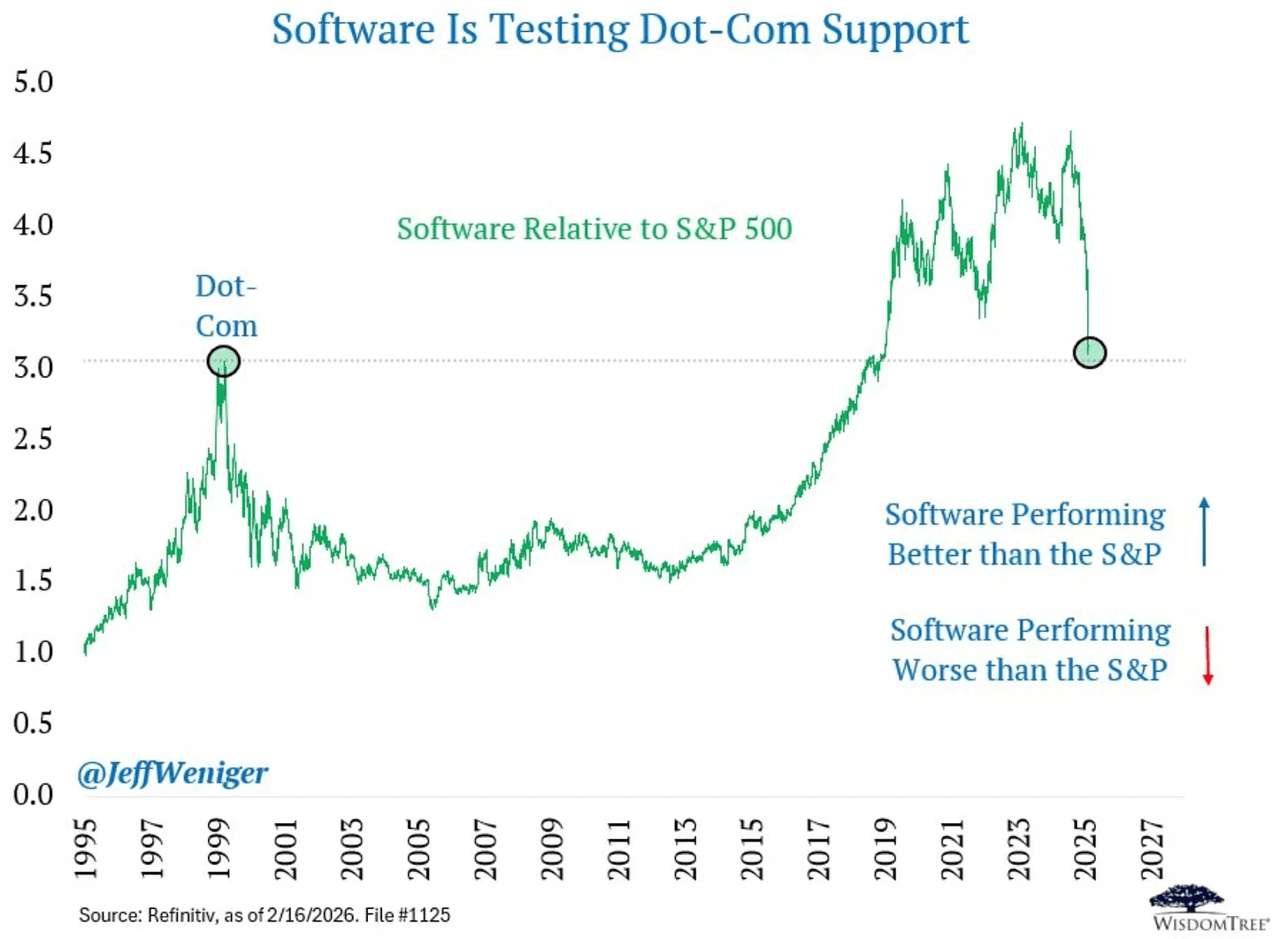

The software selloff has now reached a new low. Relative to the S&P 500, software stocks have been crushed all the way back to where they were trading at the peak of the dot-com bubble. That is not a typo.

The selling in software is relentless, and it’s starting to spread.

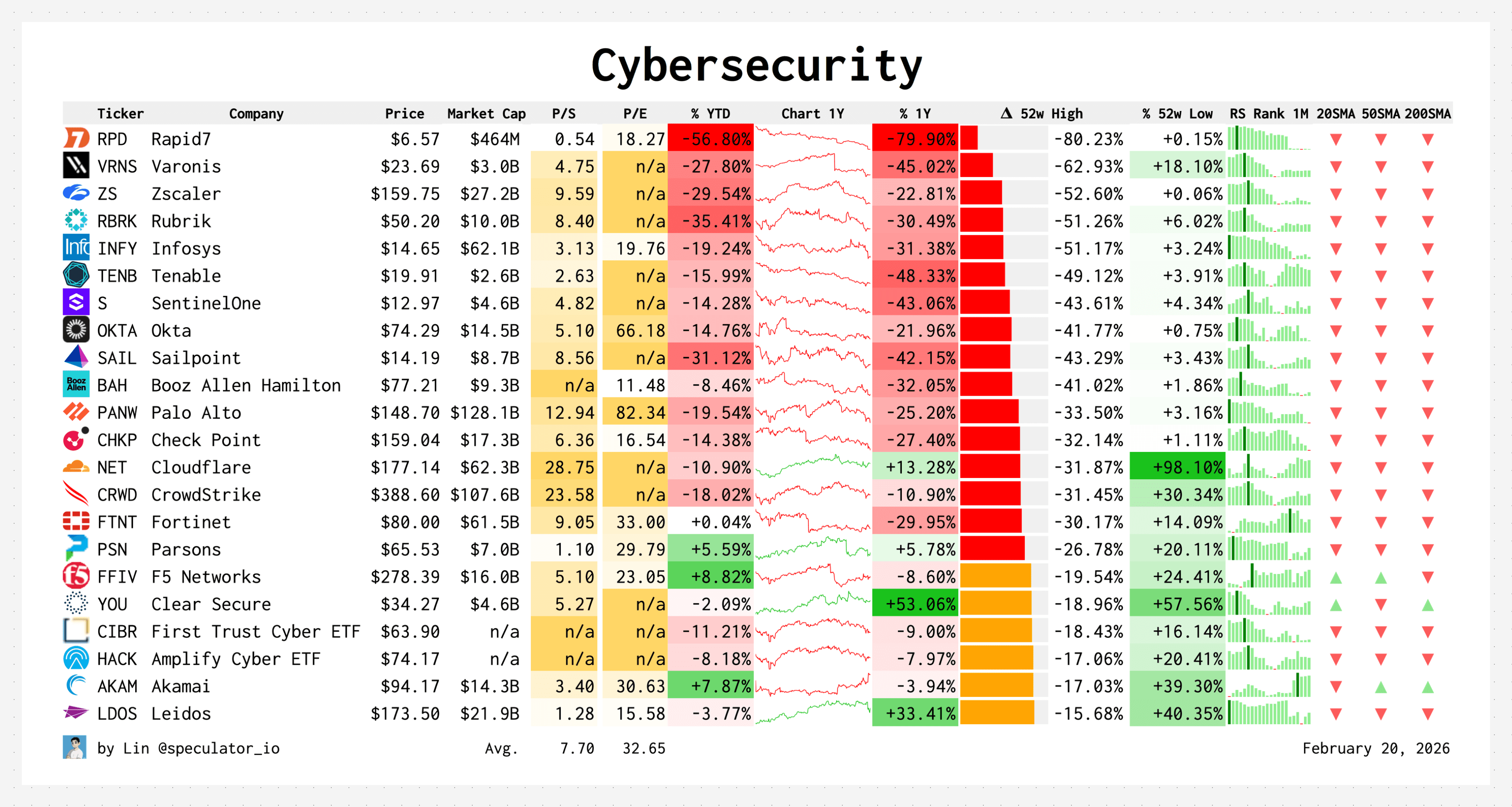

This past week, Anthropic announced their newest offering called Claude Code Security.

This led to a major selloff across cybersecurity names, whether that’s Cloudflare, Crowdstrike, or Zscaler. All of them got hit. At this point, owning software or anything even remotely close to software is taking on major risk because we’re just a headline or breakthrough away from a group wide selloff.

In my view the sell-off is mostly overblown and unjustified. The mass adoption of AI will actually increase the demand for security tools. Scams, ransomware, etc. will only get more sophisticated with AI, not less.

But this is the kind of market where anything with a non-zero chance of being disrupted will be punished. It is best to stay clear of those areas for the time being. Markets can be irrational in both directions for a long time.

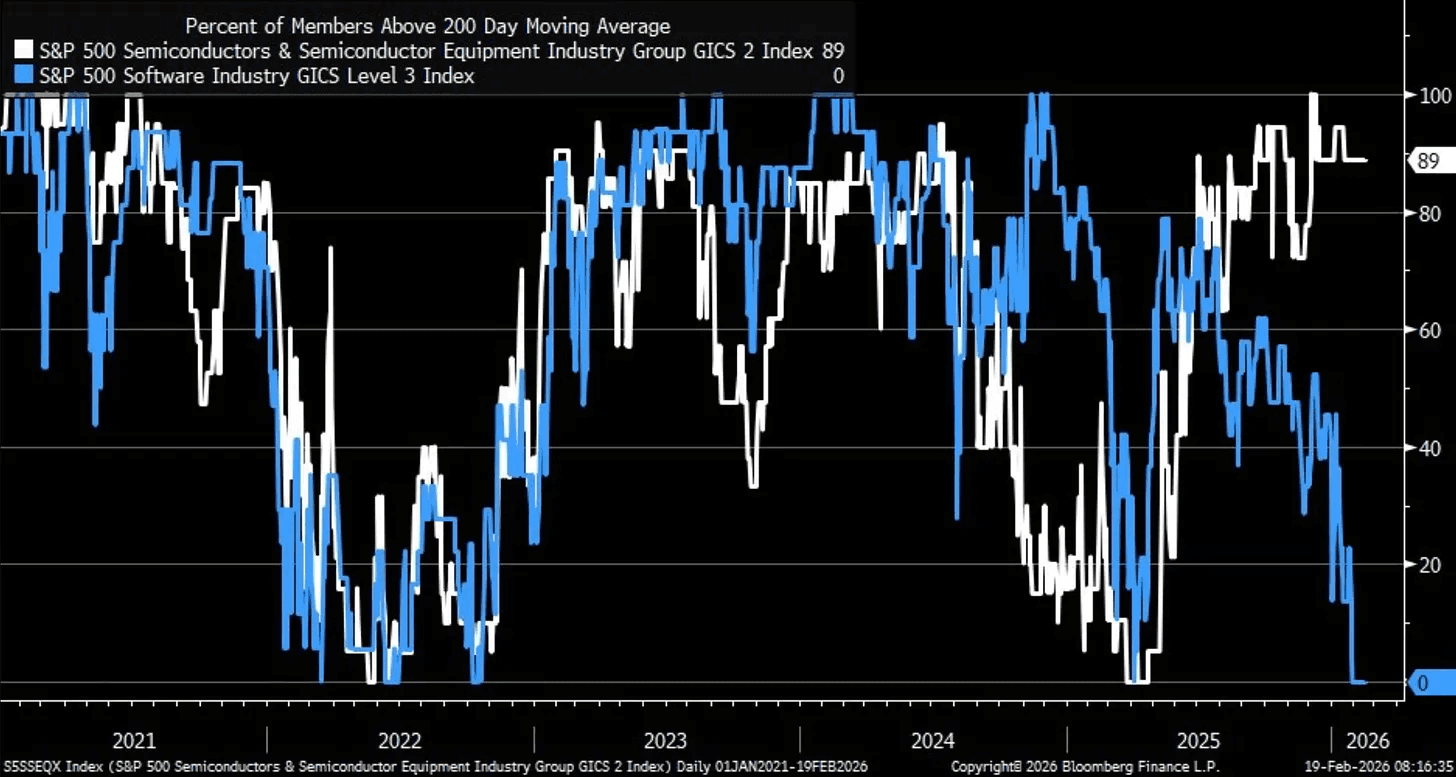

Perhaps the starkest data point of all. 89% of semiconductor stocks are trading above their 200-day moving average right now. For software, that number is exactly 0%. Not a single name. Two sectors, both in tech, living in completely different worlds.

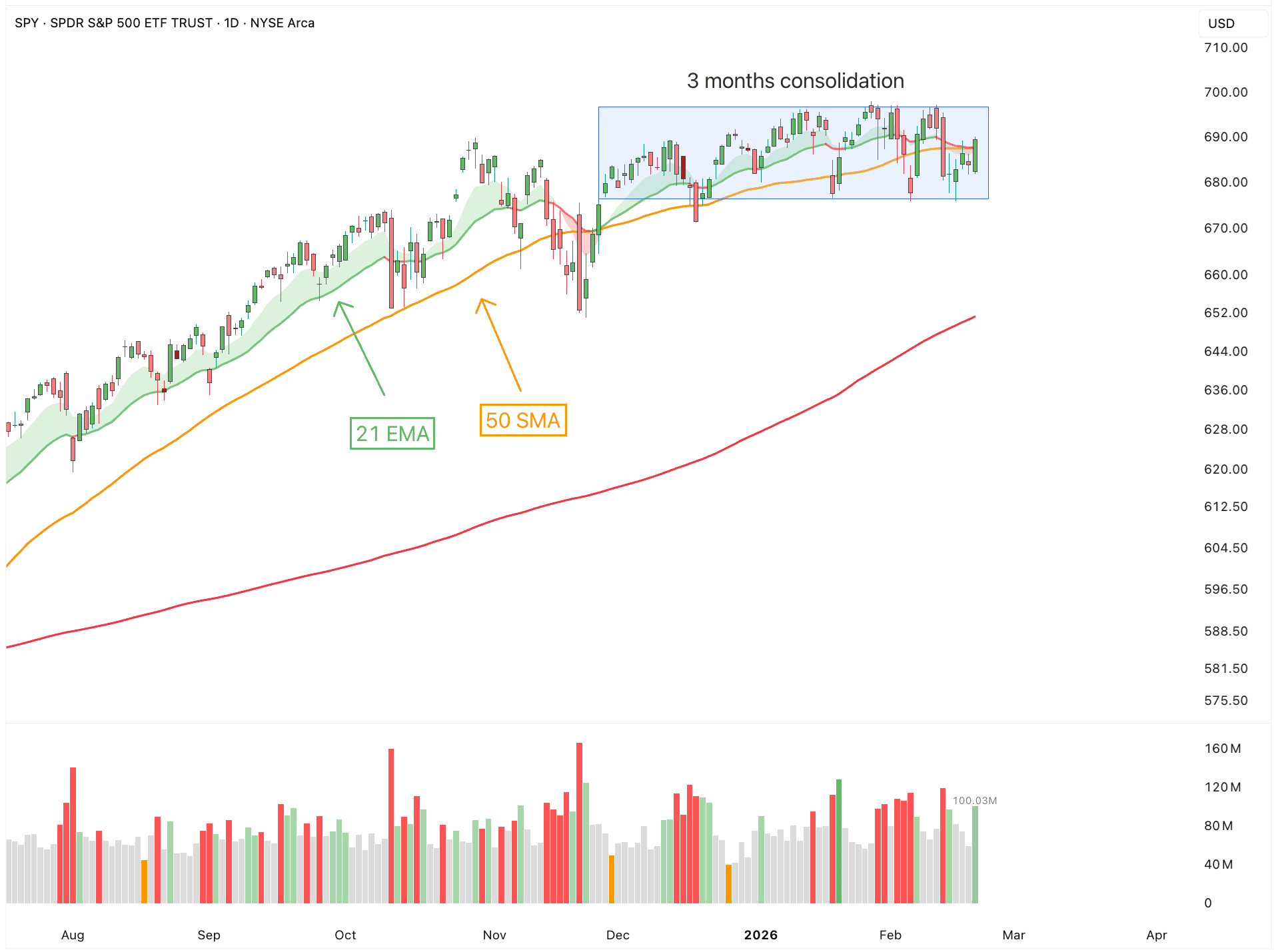

The markets seems to be inching closer to a decision point. Nvidia could act as the catalyst that pushes the Nasdaq in either direction out of this drawn-out, multi-month consolidation.

And there are a few interesting sectors and stocks that I will be highlighting soon. These are areas I want to focus on going forward, especially if the market decides to resume its uptrend after Nvidia’s earnings.

For now I want I want to reiterate exactly what I said last week. In the big picture, I am still bullish. But short-term I remain cautious. I have long exposure, but I am not trying to be aggressive. That kind of action is best saved for clear uptrends and easy markets. You want to be aggressive when the market feels easy, when everything starts to work. Not when there is a volatile chaos.

Previous Updates

View All

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap