Go Back

Lin

Weekly Market Update: A Bifurcated Market

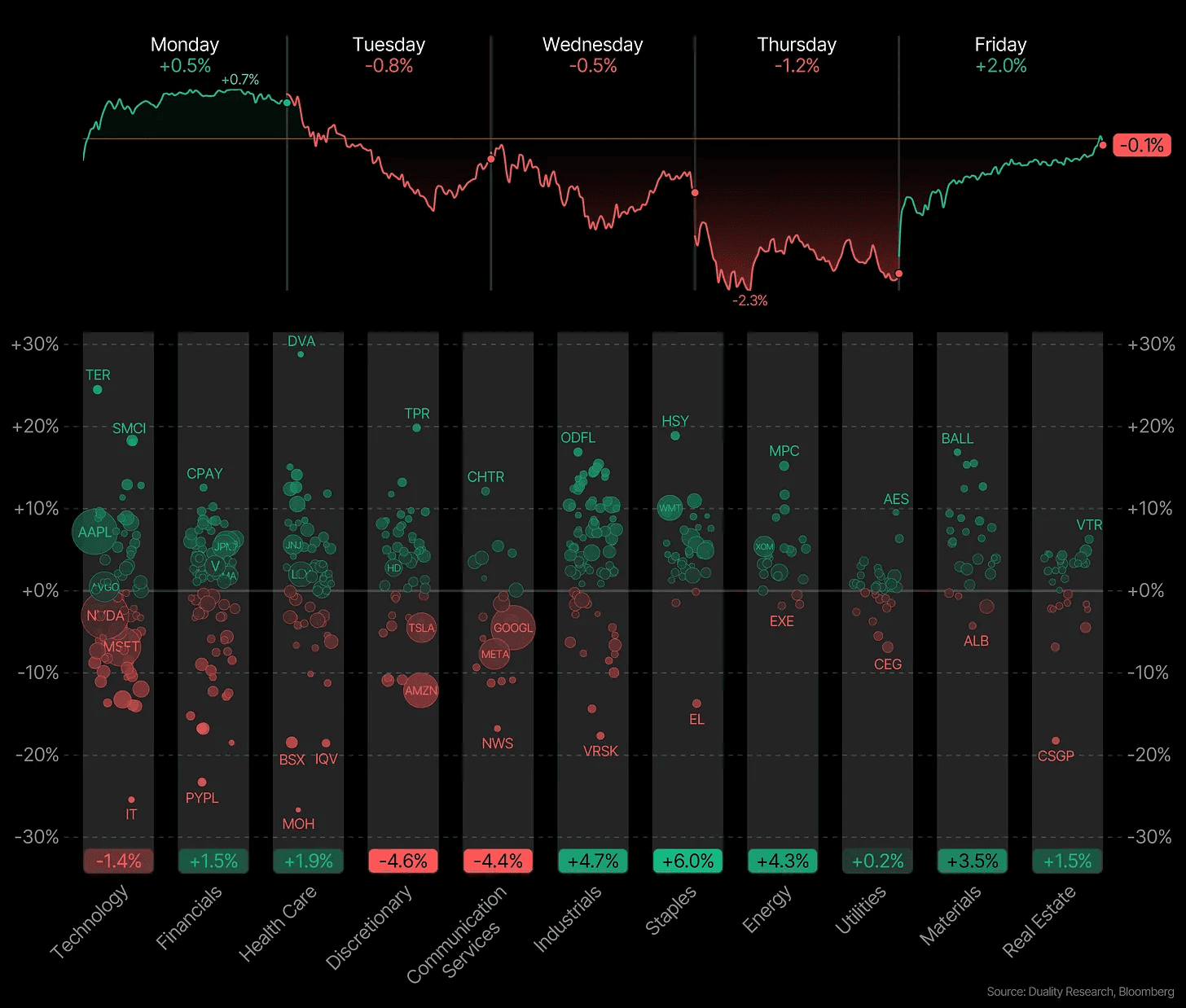

The last week was one of the most bifurcated weeks of 2026.

The Dow Jones crossed 50,000 for the first time ever. But beneath this good headline the market underwent a violent rotation. The Nasdaq had its worst 3 day decline since April before Friday’s reversal. Software stocks posted their worst week since the 2008 financial crisis. Bitcoin and the entire crypto complex melted down, while the S&P 500 was essentially flat.

It’s remarkable how well the S&P 500 held up with everything going on. But let’s explore.

A clear rotation is happening under the hood.

Market participants are moving into more stable blue chips and defensive. Energy, materials, and industrials all hit record highs this week.

The divergence is striking. Value and cyclicals are gaining strength while growth and tech face an existential reckoning tied to AI disruption.

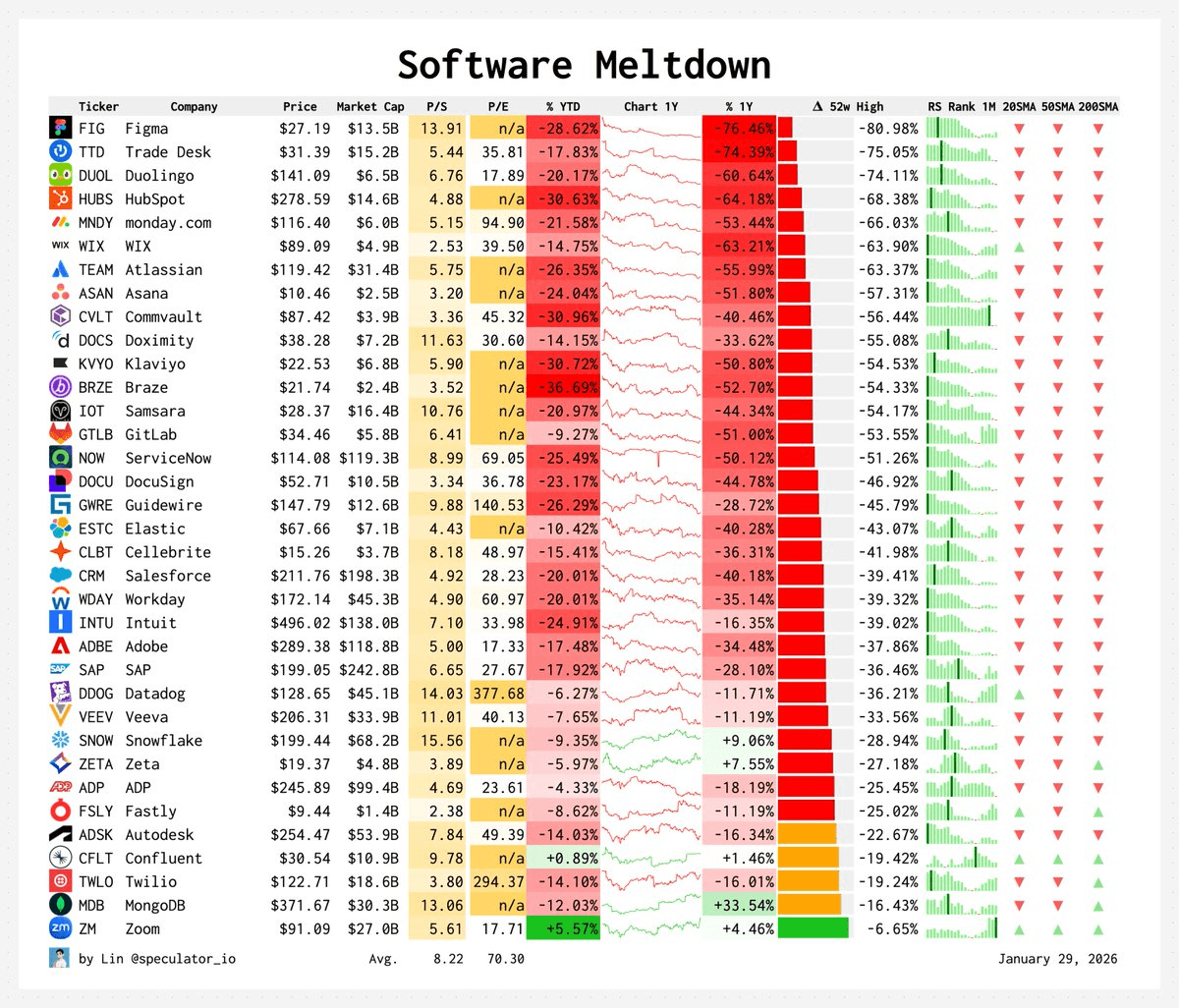

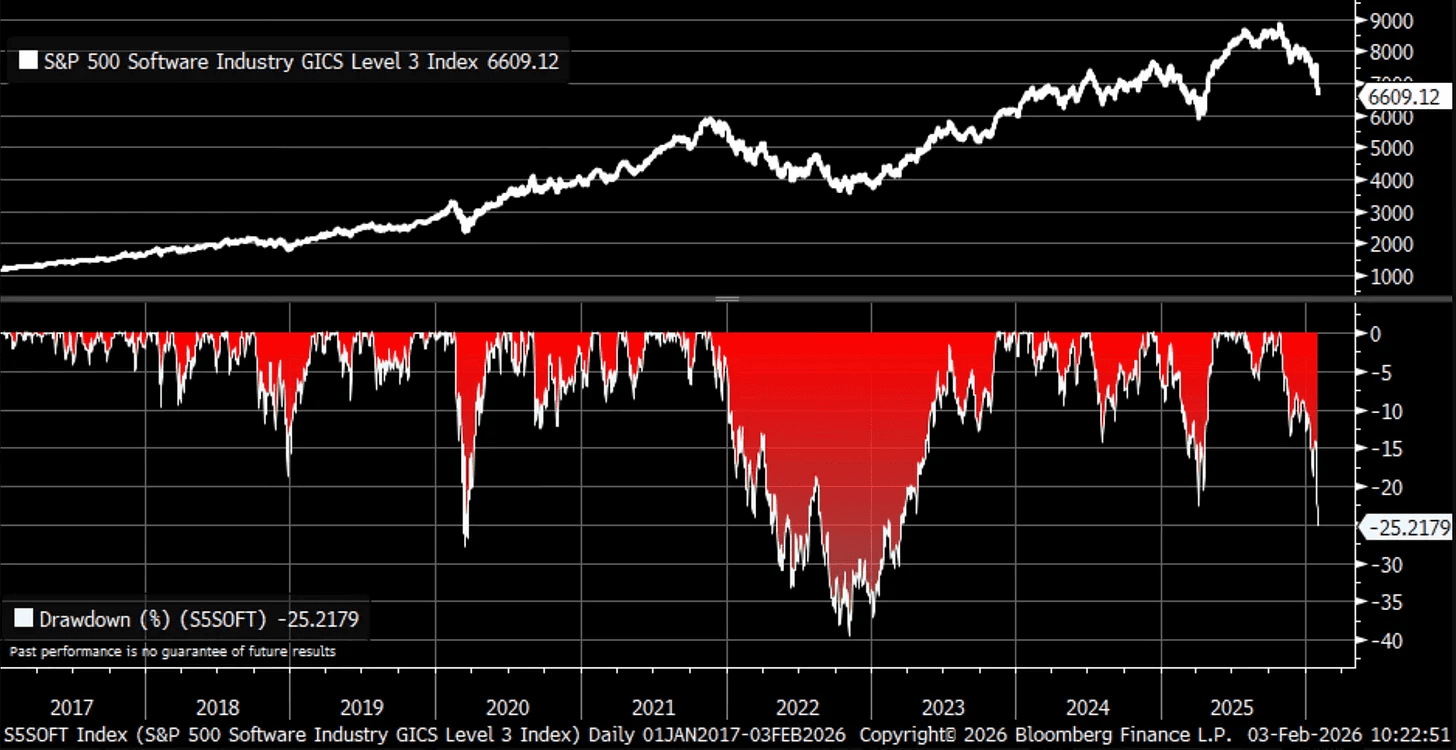

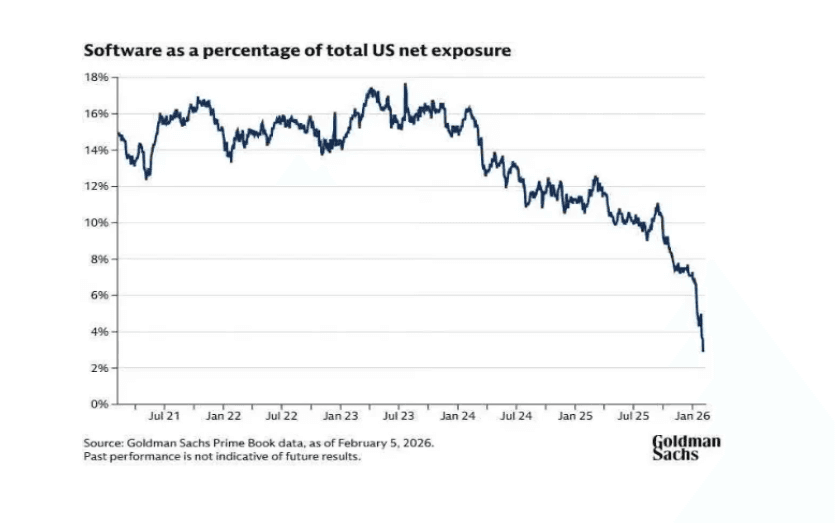

Software has been one of the weakest sectors this year. The drop was fast and deep, like what you usually see in real bear markets. For many software stocks, it felt like pure armageddon.

A big reason for this selloff is fear. Fear that new AI players like OpenAI and Anthropic could disrupt the whole software industry. It’s clear that new tools like AI agents are completely changing how developers work.

And OpenAI and Anthropic are clearly going not just after developers but almost all white collar jobs.

That’s why software stocks just had their worst week since 2008.

The IGV Software ETF fell more than 11% for the week and is now down over 24% to start 2026. Names like Salesforce, ServiceNow, Figma, and Hubsspot have been crushed.

No one wants to own software right now.

It feels like everything has been thrown out with the bathwater. That is also what creates opportunity. Investors are selling first and asking questions later. But you have to be very selective here.

Not every software company will come back. Some business models will truly get disrupted. Others will adapt, integrate AI, and come out stronger. (More on the latest AI developments in a later market update.)

I have been very bullish on AI for a long time. It will change almost every industry. That is why it is so important to spend time understanding it and actually using it. This is the biggest tech shift we have seen.

What happened in software makes one thing very clear. You want to be in the sectors that benefit from the AI buildout and avoid the ones that are most at risk of being disrupted.

And if you invert the chart above, you see the other side of the story. It has been all about semisconductors. And of course for good reason. They are the most critical part of the trillion dollar AI buildout.

Now onto crypto.

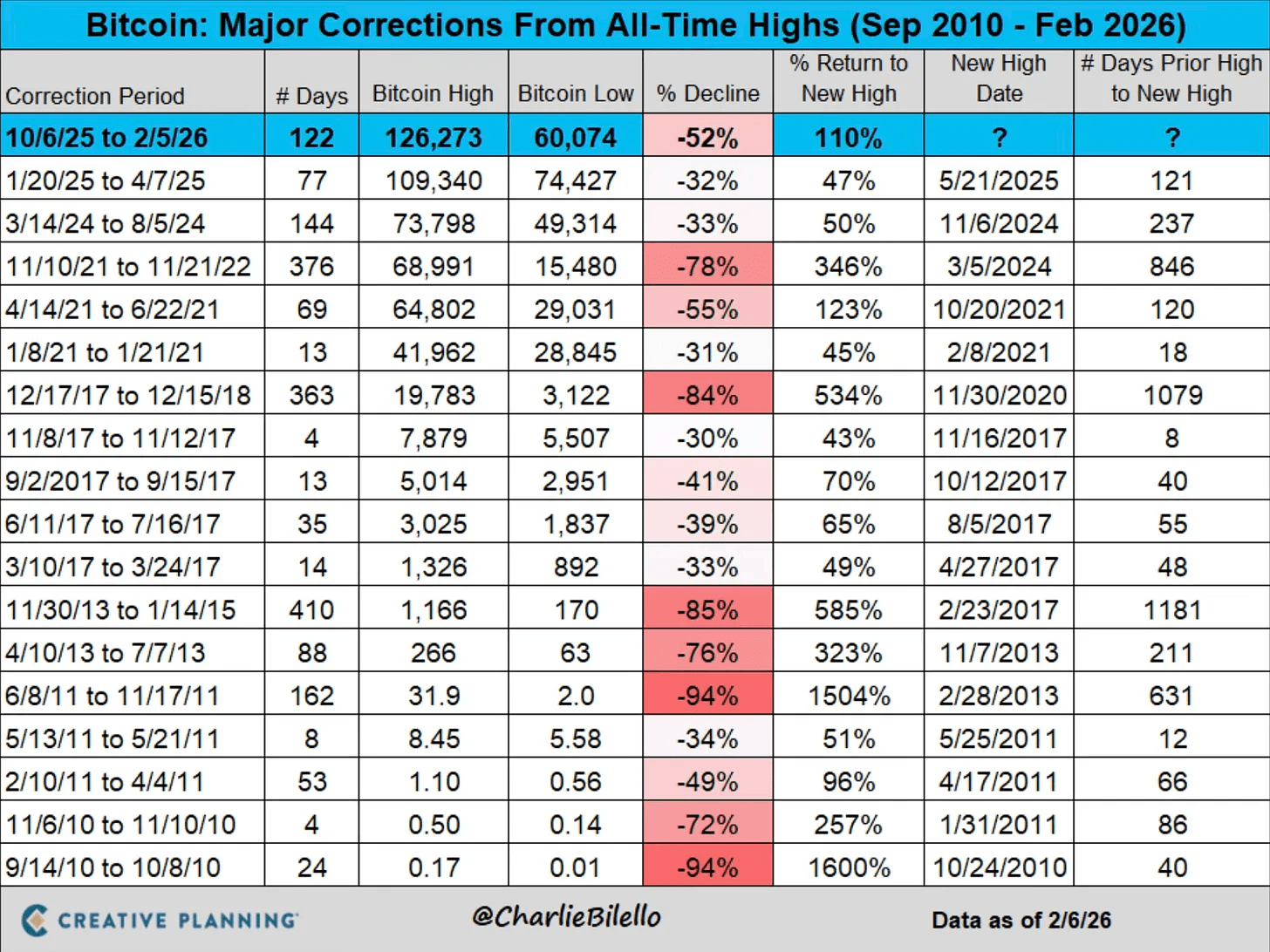

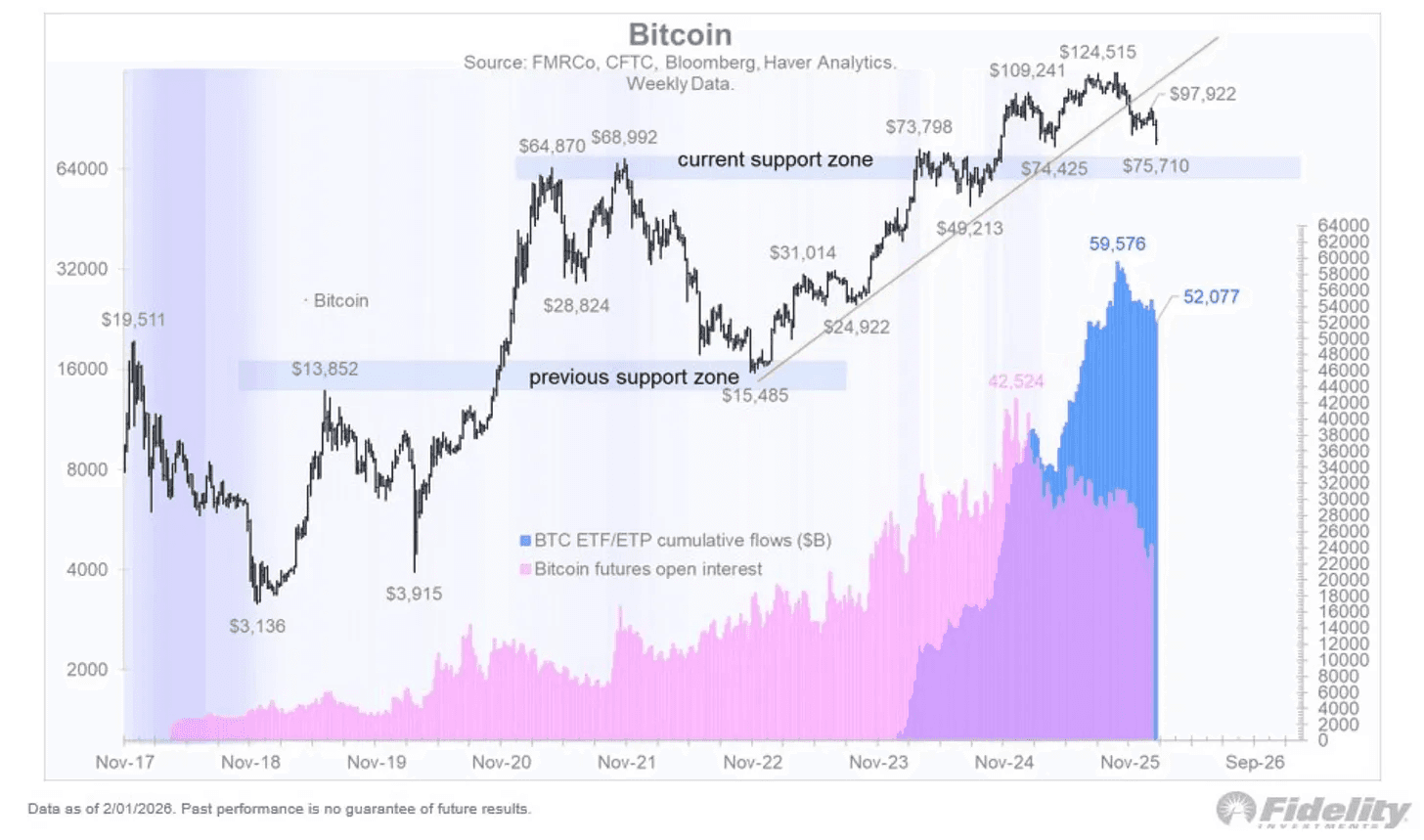

Bitcoin fell by over 20%, its worst weekly loss in a long time. This drop already far exceeds the decline it saw in April 2025 during the tariff wars.

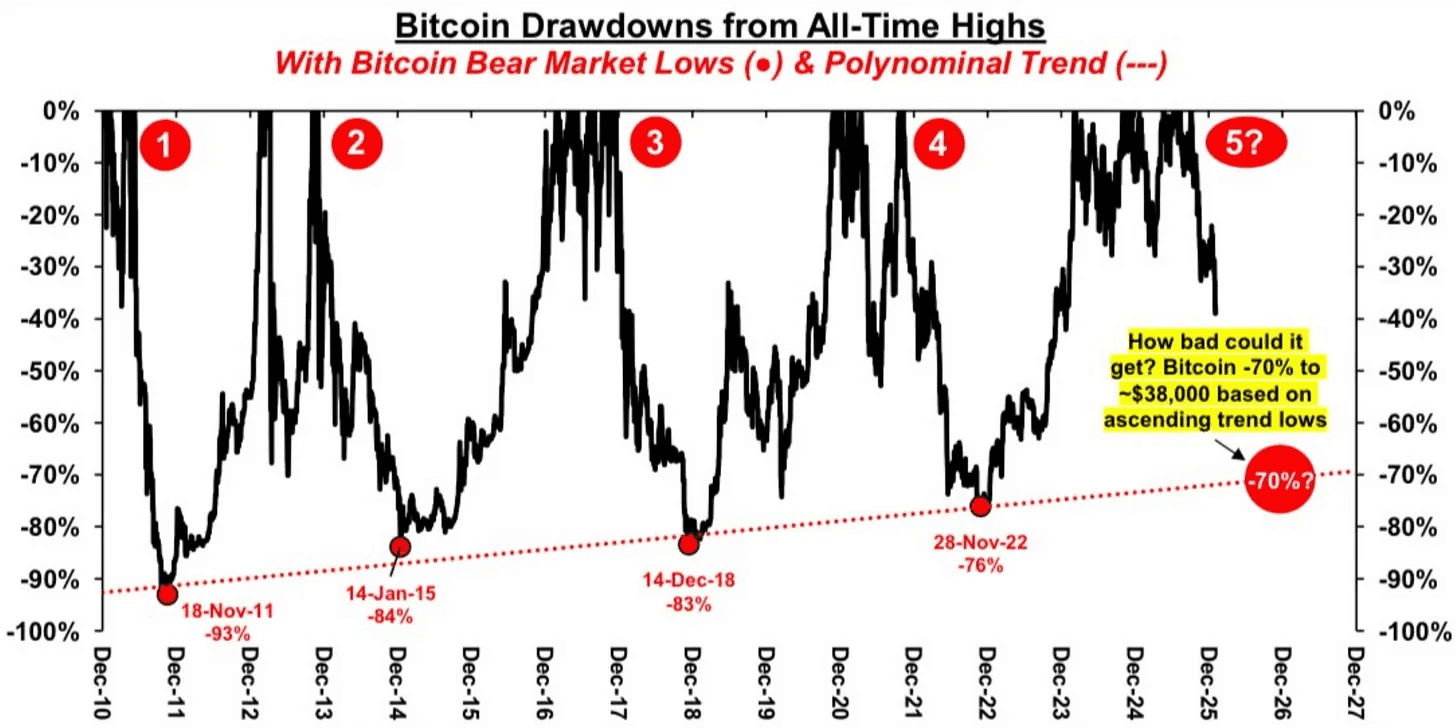

Big drawdowns are nothing new for Bitcoin.

It is now down about 50% in just a few months. It literally got cut in half. This is the worst drawdown since the 2022 bear market. Most other cryptocurrencies did even worse. As strange as it sounds, 50% swings are almost normal for Bitcoin and just a “routine” correction.

Now the real question is this. Does this turn into another 80% bear market, or is this the end of the correction?

If Bitcoin follows the pattern from past crypto winters, it could even fall toward $50,000 or $40,000. In previous cycles, Bitcoin saw drawdowns between 70% and 80% from its all time highs during major bear markets. Of course, this is not a projection, but merely a possibility.

Now that was the extreme scenario. If this is just a routine correction, we could be closer to a low.

Last week we saw record put volume in Bitcoin ETFs. That shows extreme fear, heavy hedging, and panic all at once. Traders rushed to protect against more downside. Many investors exited positions. This kind of action often happen near exhaustion points close to the lows, where most sellers are already out.

Whichever way this goes, there is no reason to try to time the exact bottom. One key principle I advocate is to focus on the strongest assets, not the weakest. There will be plenty of chances to buy IF it starts to turn around.

The problem is this. I do not see a clear catalyst. The “digital gold” story is broken. Gold is up 24% since last October while Bitcoin is down 44%.

For months, people pointed to Strategy and Michael Saylor as a weak spot. The idea was that Saylor could be forced to liquidate and flood the market with Bitcoin. That fear was addressed on the latest earnings call.

Management said they are not at risk of liquidation and that the value of their Bitcoin holdings would cover their debt as long as Bitcoin stays above $8,000. So, apparently there are no balance sheet issues unless Bitcoin collapses far below current levels.

That action spilled over into equities. Tech stocks, software, and other momentum groups started falling just as fast and just as hard as crypto.

There are a few reasons for that:

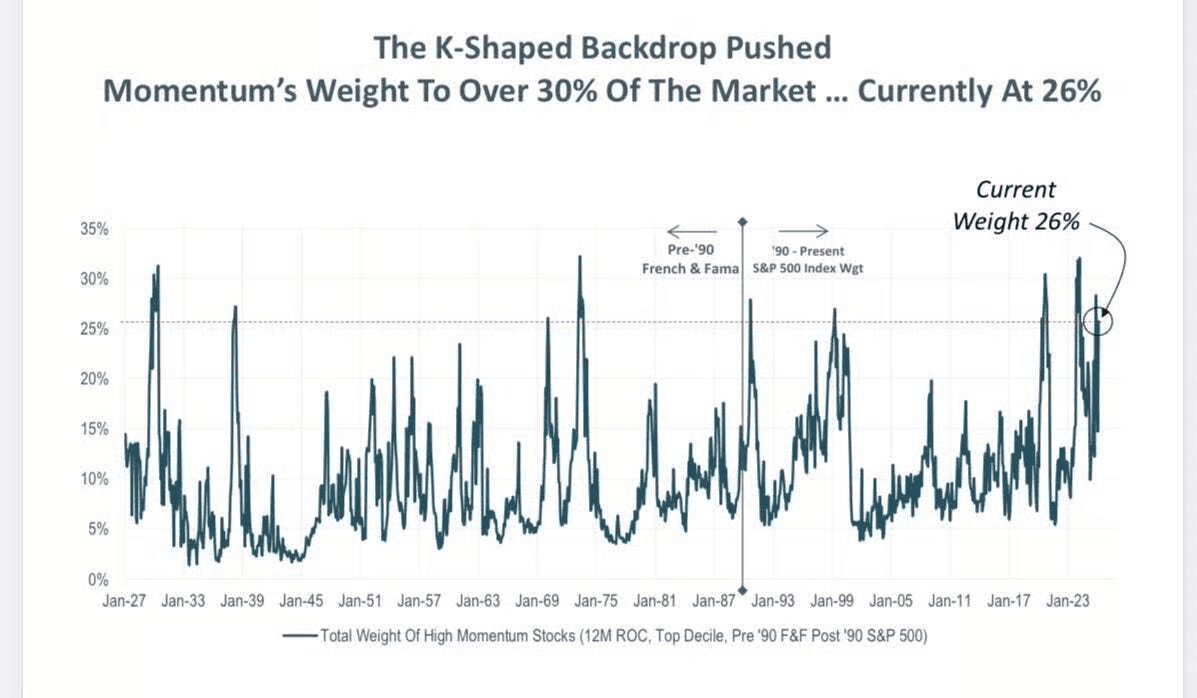

First, many investors are positioned in the same momentum names. Today, momentum makes up about 26% of the market.

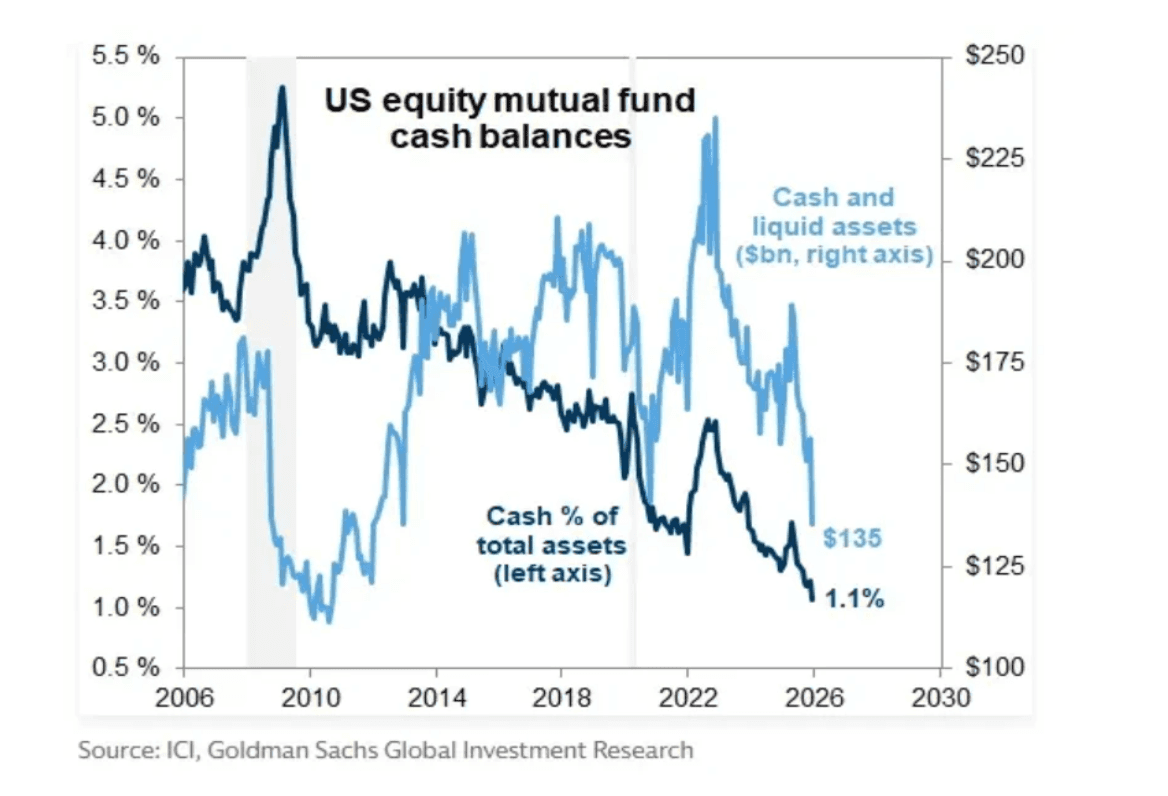

Second, fund managers are putting money into almost anything except cash.

That makes sense in a bull market like this. Cash levels usually get drawn down, especially during a period when the USD is actively being devalued. But if cash is not an option, the natural result is rotation.

The chart below shows a clear rotation inside the S&P 500. Performance is no longer driven by just a few mega cap names but by a much wider group of stocks. Instead of relying on a handful of leaders, investors are now rotating capital into the laggards.

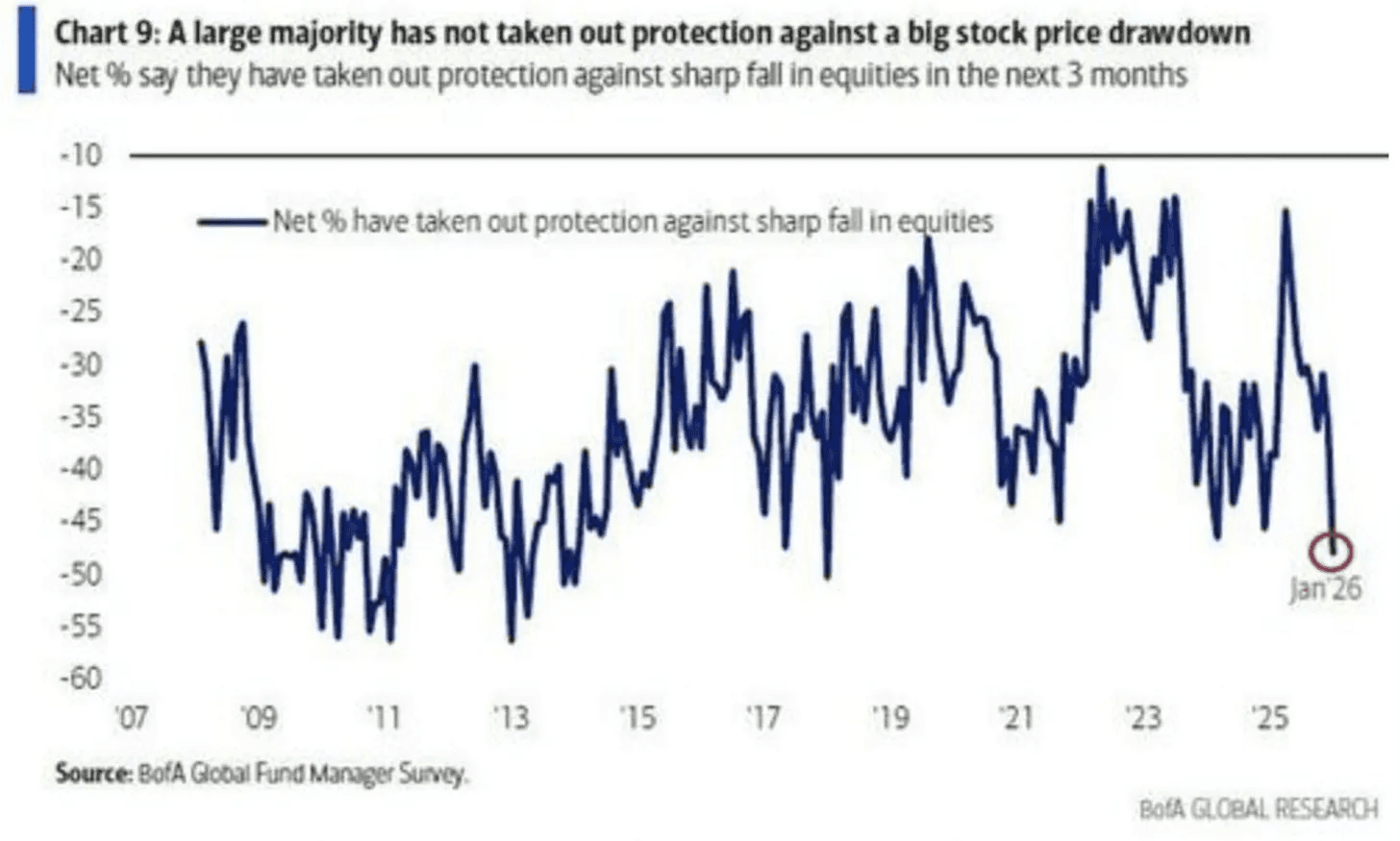

Third, it is not just low cash levels. Funds are also the least hedged in almost a decade.

They are fully exposed with very little protection if selling speeds up. Many portfolios now move almost 1 to 1 with the market.

When selling pressure increases, they cannot buy the dip because they have no dry powder. They also cannot rely on hedges to soften the fall. That leaves selling as the only option.

This triggers a chain reaction where selling leads to even more selling.

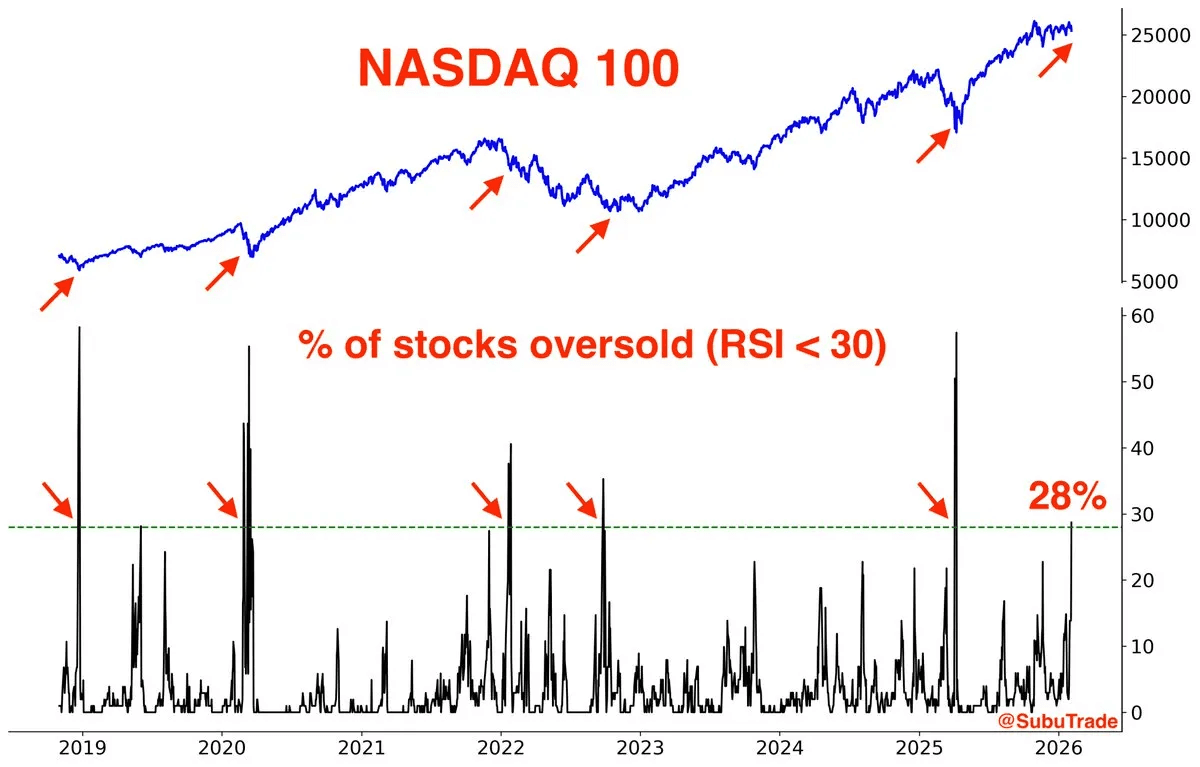

This is why we saw an extreme number of stocks with an oversold RSI this past week, the highest reading since the April 2025 tariff war lows.

If you look left on the chart, the last time before that was in 2022. Each time, the market still went a bit lower after the signal. So it did not mark the exact bottom. But it was usually very close to a low.

This supports the idea that we are not heading for a crash.

The action under the hood was brutal in some groups, but the S&P 500 held up well and many stocks still hit new all time highs.

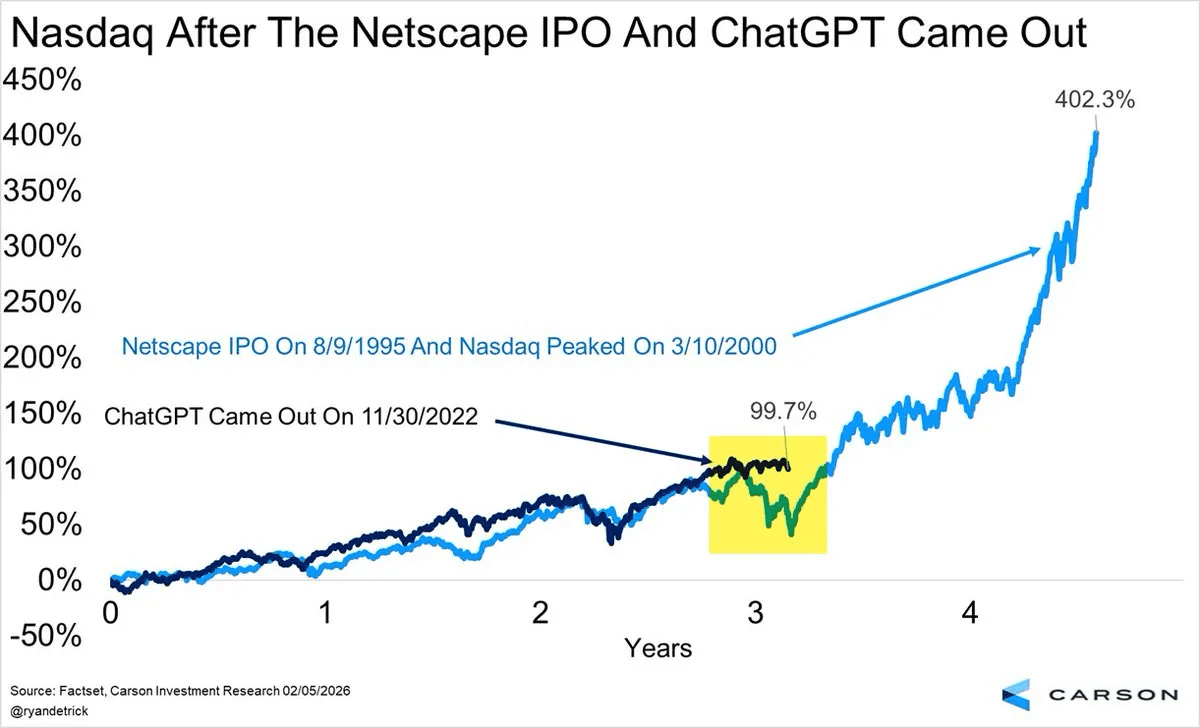

Everyone likes to compare the AI boom to the dot com era. So far, the path actually looks quite similar.

If this analog holds, what we are seeing now is normal for this stage of the cycle. Year 3 and moving into year 4, where we are now, was very volatile back then too. And a larger correction is still possible.

There is another important point. The biggest gains often come late in the cycle. That is when the real mania starts. That is the part most people remember about the dot com bubble. The final few months. Fortunes were made but unfortunately also lost.

If we see a wave of IPOs from names like OpenAI, Anthropic, and SpaceX, we could see similar behavior.

Catching even part of that move can be life changing. The key is to not give it all back on the way down. That is why risk management matters so much.

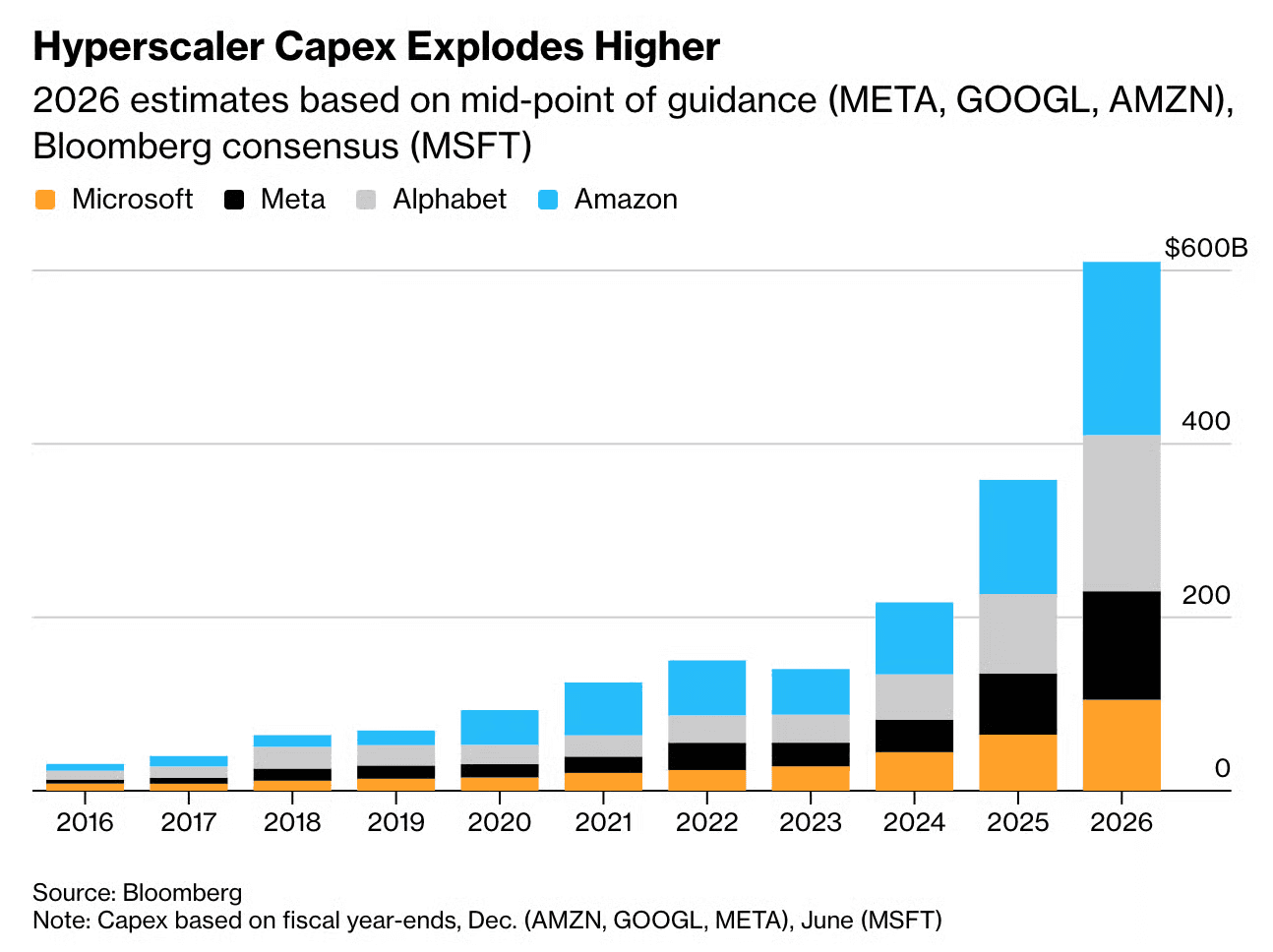

We are seeing mind boggling CAPEX numbers.

The four hyperscalers, Microsoft, Meta, Alphabet, and Amazon, are set to invest more than 600bn this year into data centers. And this is not likely to slow down soon. This is a global arms race.

You do not need to know when it ends. You just need solid risk management. You might miss part of the upside, but you avoid serious trouble.

Position sizing is one of the most important parts of investing. If you size wrong, you can get wiped out in a single week. We just saw that across crypto, software, and other speculative groups where normal selling turned into forced selling.

This does not mean you need to own 100 or more stocks. But it does mean that going all in on a small number of names carries real risk. When momentum turns, concentration works against you as fast as it worked in your favor. That’s why I’m a fan of increasing exposure and sizing when the markets are favorable and reduce exposure when the markets are deteriorating or much more volatile.

Speaking of volatility. There will be plenty of it over the next two months.

We are more than halfway through the Q4 earnings season. But there are still plenty of interesting names left to report.

This week was wild and I don’t think we’re out of the woods yet. I still believe we are in a bull market and recent action is just a bump in the road. Pullbacks and corrections are part of any bull market. But even so it’s important to not let a correction get out hand.

Crypto and software are still two groups to watch to see if sentiment and price action improve. Focusing only on the weakest groups while ignoring the strength in energy, blue chips, semiconductors, and other leaders does not make much sense to me, but it is still a useful indicator to track.

I also want to point out again that most individual stocks and themes are at the mercy of the broader market. If the market, and especially the Nasdaq, weakens, many themes and groups will likely weaken as well. The past month has not been very constructive for many momentum themes, which explains the poor performance from these areas.

It is important not to force positions in a choppy market. It is very difficult for a single theme to move higher when there is broad selling across speculative sectors. In the end, money flows often behave like one large trade. You need capital flowing into speculative areas for these themes to work, and that has not been the case recently.

Previous Updates

View All

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap