Go Back

Lin

AAPL

The AI Buildout Is Far From Done

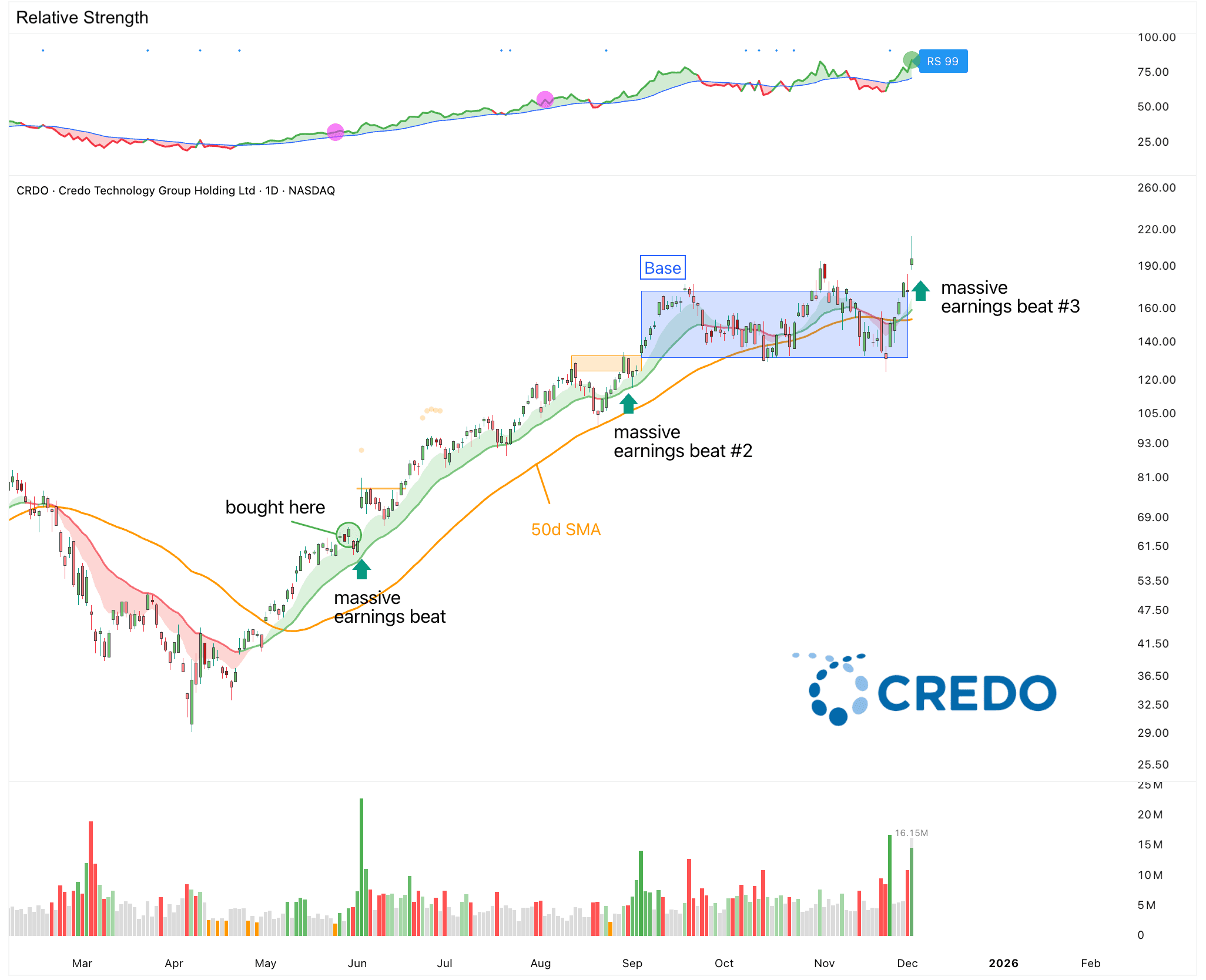

Credo just delivered the strongest quarter in the company’s history.

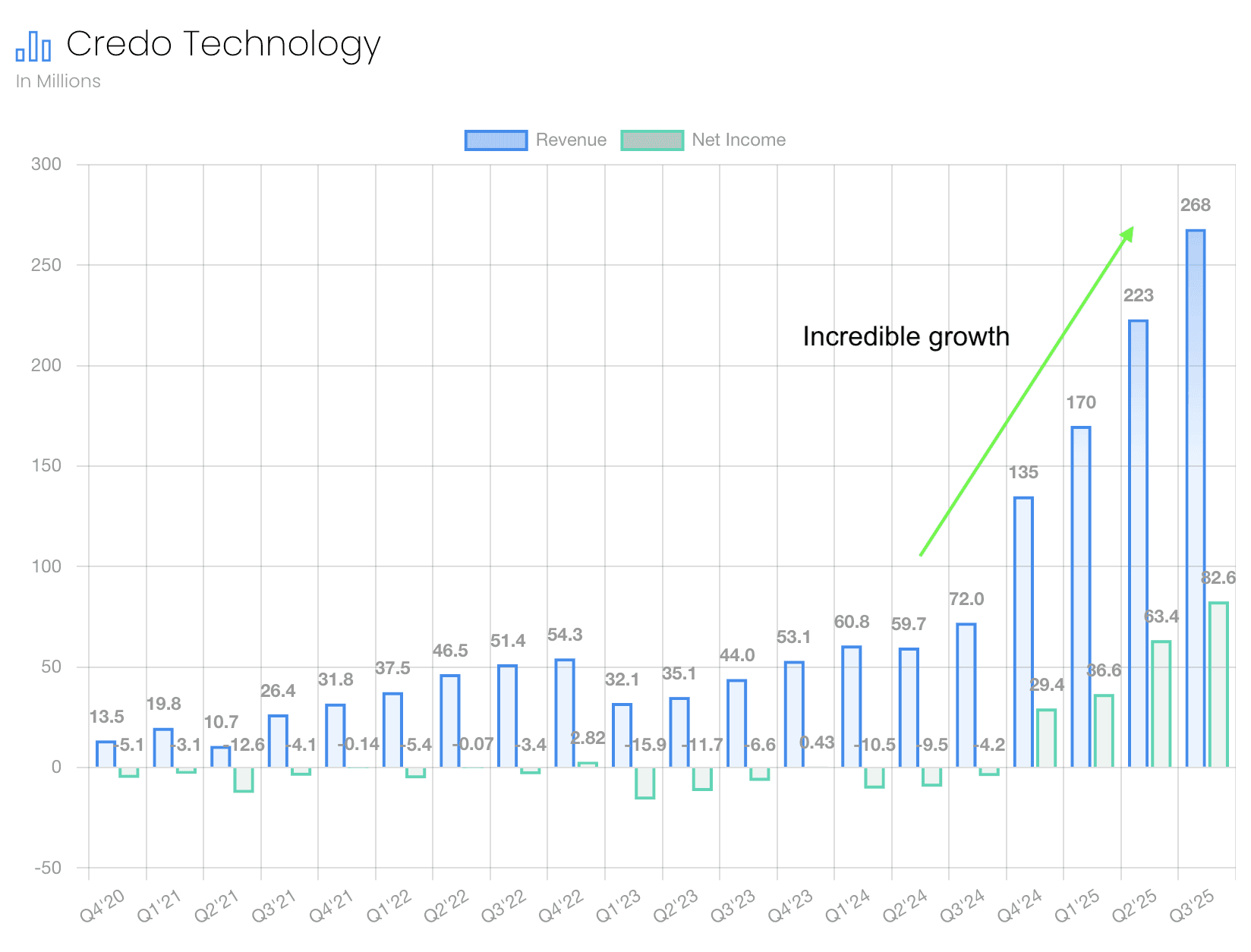

Q2 revs of $268M vs $235M est. (+14% beat)

Q2 revs up +20% QoQ and +272% YoY

It has been one of our core positions for a while. This is now the third record breaking quarter. And this quarter makes one thing very clear. The build-out of the biggest AI training and inference clusters in the world is nowhere far from done.

It is always the same. Every few months investors get skeptical about the AI buildout. And every time the data proves them wrong.

Credo also gave an incredible outlook.

Guidance:

Q3 revs of $340M vs $247M est. (+37% beat)

Q3 revs guidance implies +27% QoQ and +152% YoY

It's safe to assume CRDO will beat their Q3 guidance which means they probably do at least $365M+ which would be +36% QoQ and +170% YoY.

There is a reason why it’s up almost 300% and one of the best performing stocks over the last year.

It’s not a cheap stock by any means but they deserve to trade at a premium with these growth numbers plus 31% net income margins and gross margin guidance coming in 120+ bps above street estimates.

These numbers tell a pretty clear story.

But I keep seeing discussions about AI that focus almost only on chatbots and demand is limited. That view is too narrow. When you look at what is happening inside data centers and large tech companies, the long-term demand for AI compute is coming from areas that are rarely part of the public conversation.

The first area is basic data center compute. This is already close to $100B dollars per year. It includes data processing, pipelines, analytics workloads, risk models, and internal machine learning jobs. None of this feels new or exciting, but much of it will move to accelerated architectures over time because they offer better speed and lower cost. Even without consumer-facing AI, this creates a large and steady demand for AI-class hardware.

The second area is recommender systems. This is the part of the internet that drives most of the revenue. Examples include Google Ads, YouTube, Instagram, TikTok, Amazon search, Spotify, Netflix, and e-commerce funnels. The economic value here is in the range of a few hundred billion to around one trillion dollars. The next generation of these systems will use GenAI models rather than older methods. This shift is not a small change. It affects the core business models of trillion dollar platforms.

The third area is physical AI. Robotics, autonomous systems, warehouse automation, delivery robots, agricultural machines, drones, and home devices all fall into this category. These systems rely on continuous real-time inference. The compute load is very high and can exceed chat-style workloads by a wide margin. If this sector grows as expected, it could become the largest source of demand for AI compute.

When you consider these three areas together, it is clear that the AI story goes far beyond chatbots. Large parts of modern computing are shifting toward models that need far more acceleration. And there is almost no limit for the AI compute. Text, images, videos, simulations, science. There are so many use cases that are not quite feasible or that could use billions of tokens of compute.

The AI buildout is just getting started.

Previous Updates

View All

- Weekly Market Update: All Eyes On the Mag 7

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character