Go Back

Lin

AAPL

Buy

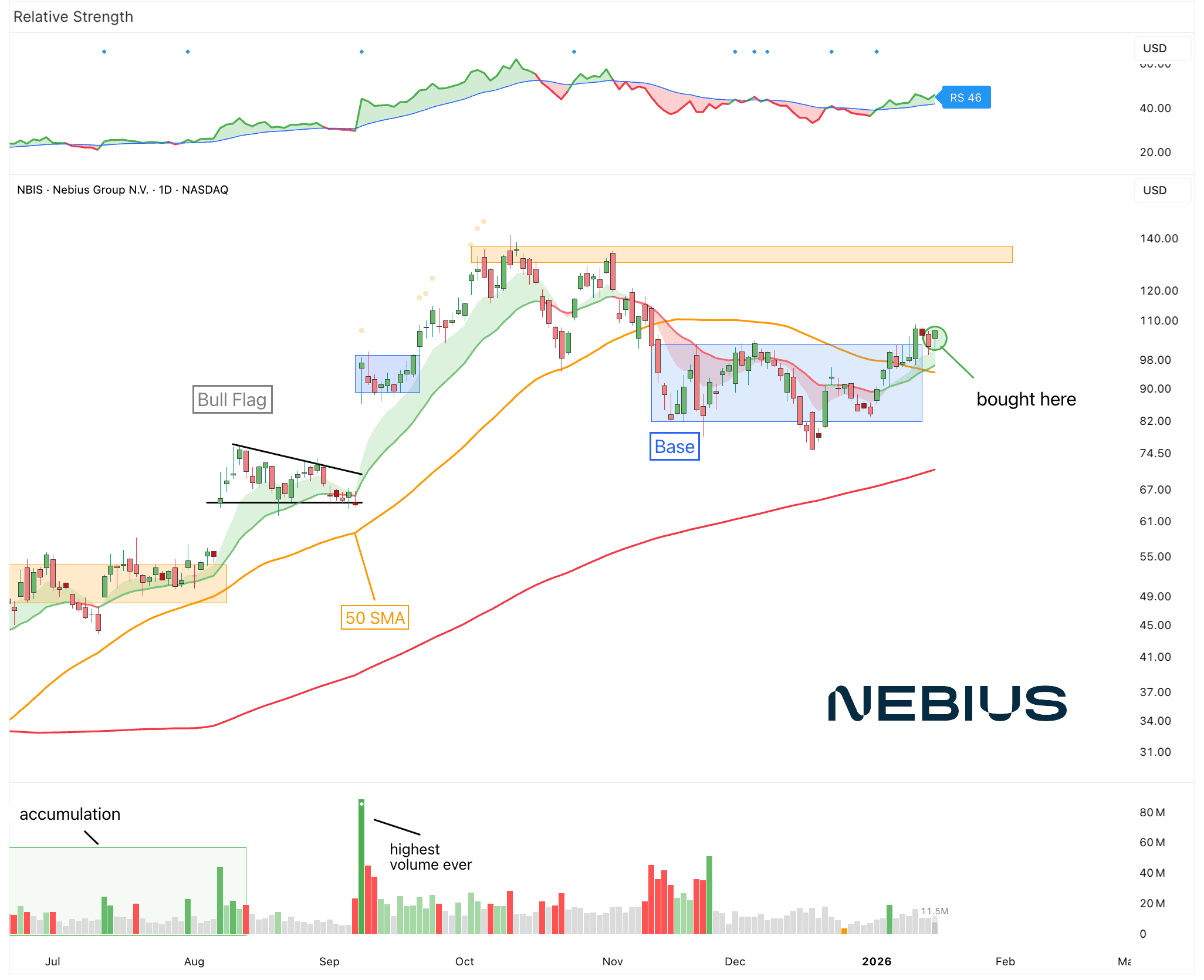

Buy: $NBIS

TSMC just had a great earnings report.

Gross margin came in at 62.3%, above the 59% to 61% guide. Q1 2026 guidance is even stronger at 63% to 65%.

2026 capex is guided at $52B to $56B, up from $40.9B in 2025.

TSMC expects supply to finally catch up with demand in 2028 or 2029.

The key takeaway from the TSMC earnings call is simple.

AI demand is not just strong. It has changed how the whole chip industry works. The numbers prove this. In Q4, TSMC made $16B in net income and posted a gross margin of 62.3%. That was better than most investors expected.

But even more interesting, capex is set to rise significantly.

For 2026, TSMC plans to spend $52B to $56B on new fabs. That is about 31% more than last year and well above expectations. It’s important to note that this behavior is not typical for the company. TSMC is known for being careful with spending. It does not invest this much unless it sees very clear demand years ahead, which means the AI cycle is not even close to a peak. Demand is incredibly high and supply remains the bottleneck.

In short, 2026 looks like a phase of acceleration, not slowdown, for AI.

This of course spills down to the entire value chain. That’s precisely why I highlighted AI infrastructure as one of the key sectors to watch this year.

I want to be positioned in the entire value chain: fabs, chips, equipment, networking, data centers, energy, materials and co.

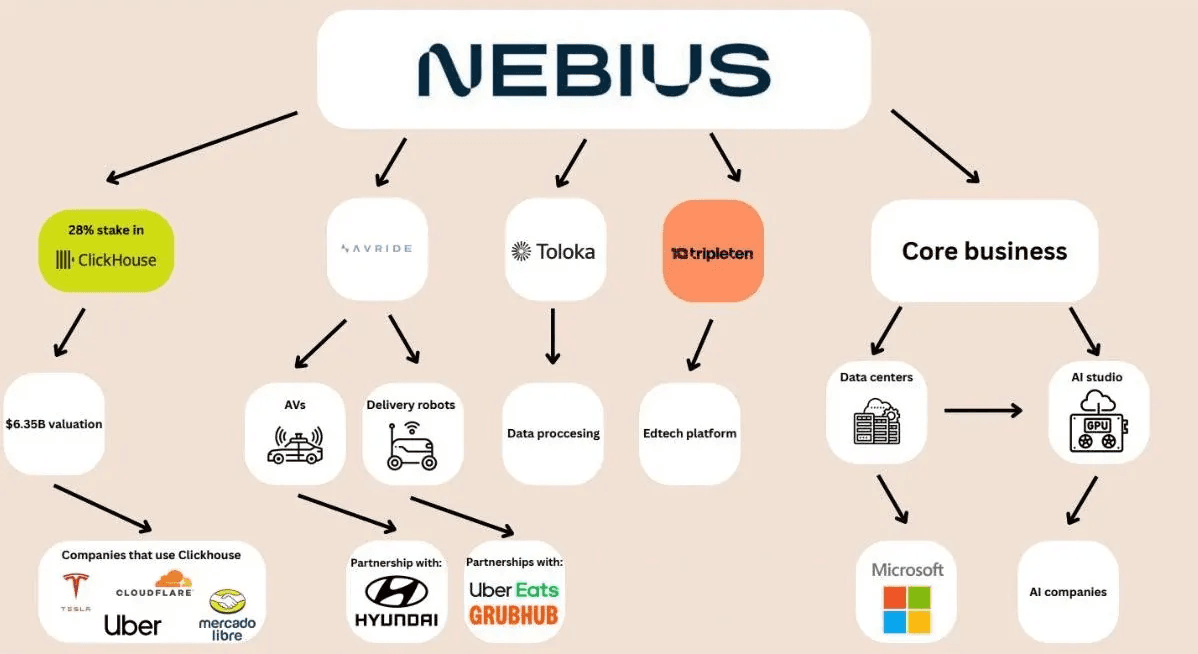

This is why I’ve just initiated a position in Nebius.

It’s one of the fastest growing companies in the market.

Nebius is a spin-out of Yandex (Russia’s equivalent to Google), so their tech comes with years of handling internet-scale search and data. Now they’re putting that experience into powering Europe’s AI ecosystem.

They are not trying to be the next AWS or Azure. They focus on the boring but critical parts that actually make AI work. Things like compute, infrastructure, and reliability. That is the kind of work you cannot skip if you want AI at scale.

Data centers built specifically for AI training

Liquid cooling that keeps GPUs running at full power

Cloud services tuned for speed and cost, not just storage and hosting

But it’s not just about providing raw compute. The focus goes far beyond performance alone, extending into areas like autonomous vehicles, database management, and agentic AI.

Now it’s setting up again. It’s been consolidating for the last few months. And it’s starting to break out of this base.

Additionally, an important variable to watch is how the rest of the sector is doing. That gives you a good indication of whether the move is driven by randomness or by institutional demand. You want the entire sector to perform well, not just a single name.

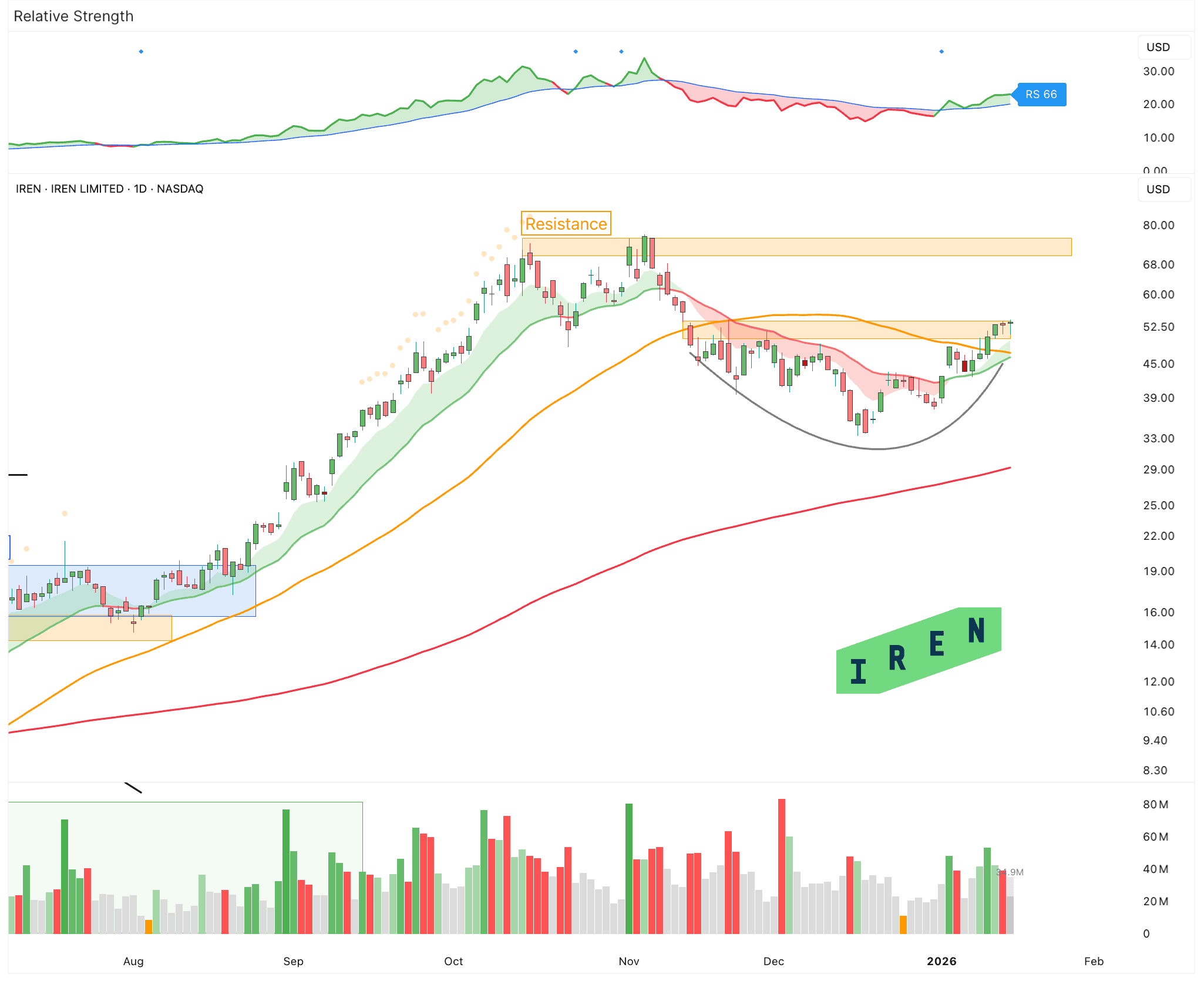

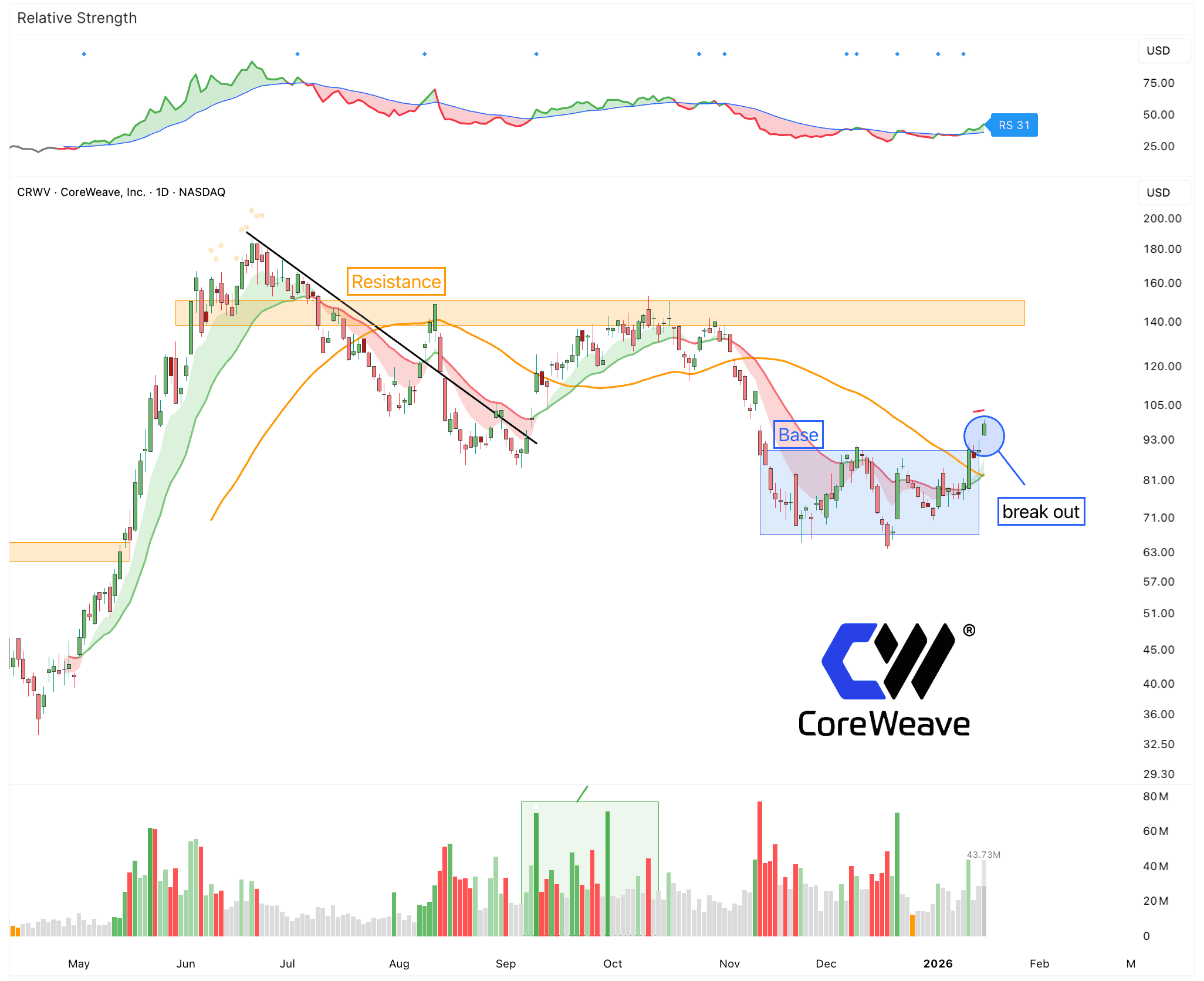

The two key competitors are IREN and CoreWeave. Both started as Bitcoin mining companies but quickly pivoted into high performance compute infrastructure for AI. Today, they offer compute, storage, networking, and managed services mostly for hyperscalers.

Both names had very strong upside moves, followed by long digestion phases. They spent months going sideways. CoreWeave even went through nearly a full year of consolidation. Now that they forming clean bases, and starting to move out of those bases. And the risk reward is starting to look very attractive for another leg higher.

Previous Updates

View All

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap

- A Few Portfolio Changes