Go Back

Lin

Weekly Market Update: The Price of Admission

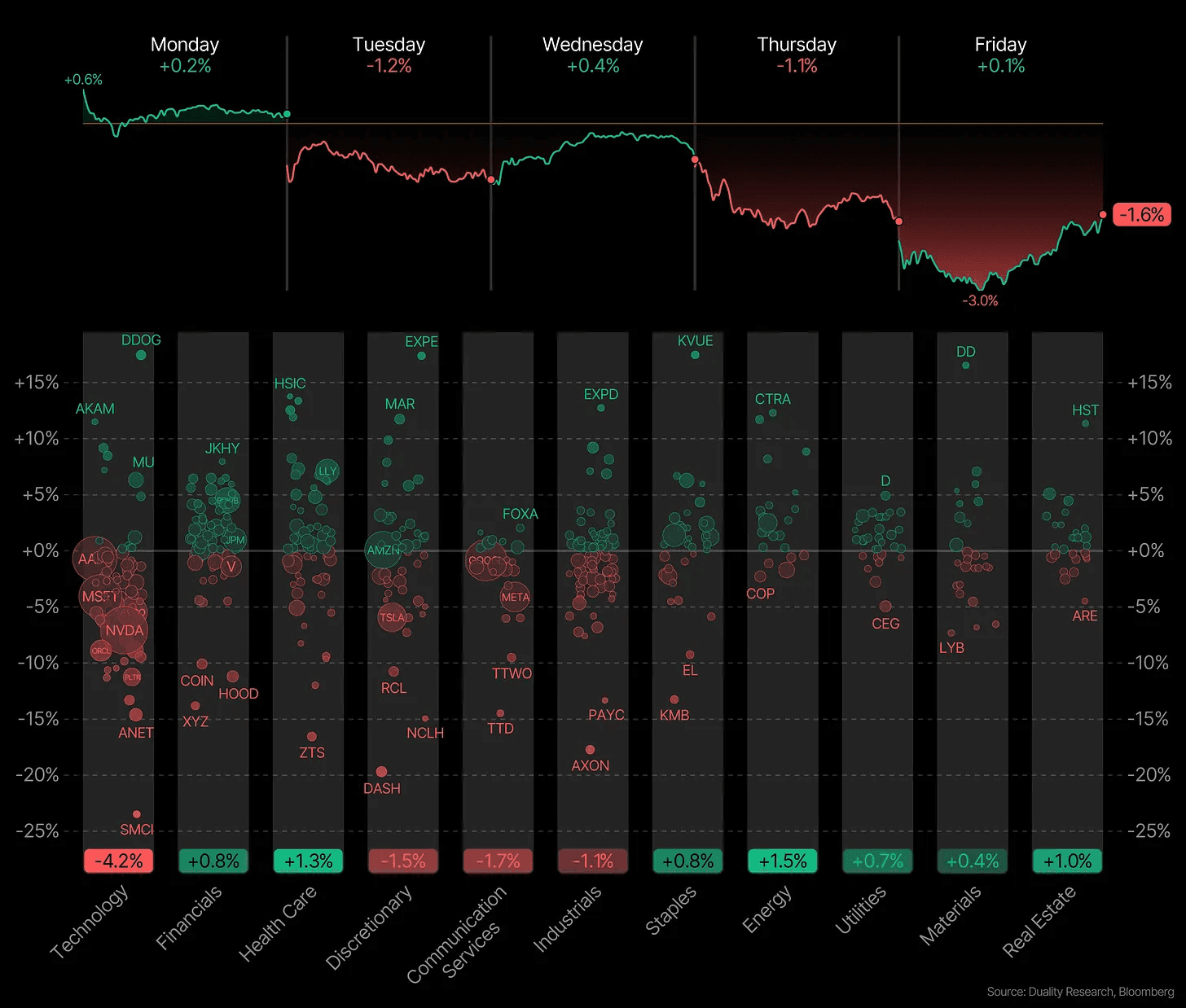

What a week.

Monday opened strong and sold off. Tuesday gapped down. Wednesday recovered. Thursday gapped down again. Friday opened lower but finished flat. In the end, the S&P closed the week down about 1.6%.

But the index is hiding what’s happening underneath.

The S&P 500 is down at the lows 4% and 6% for the Nasdaq 100.

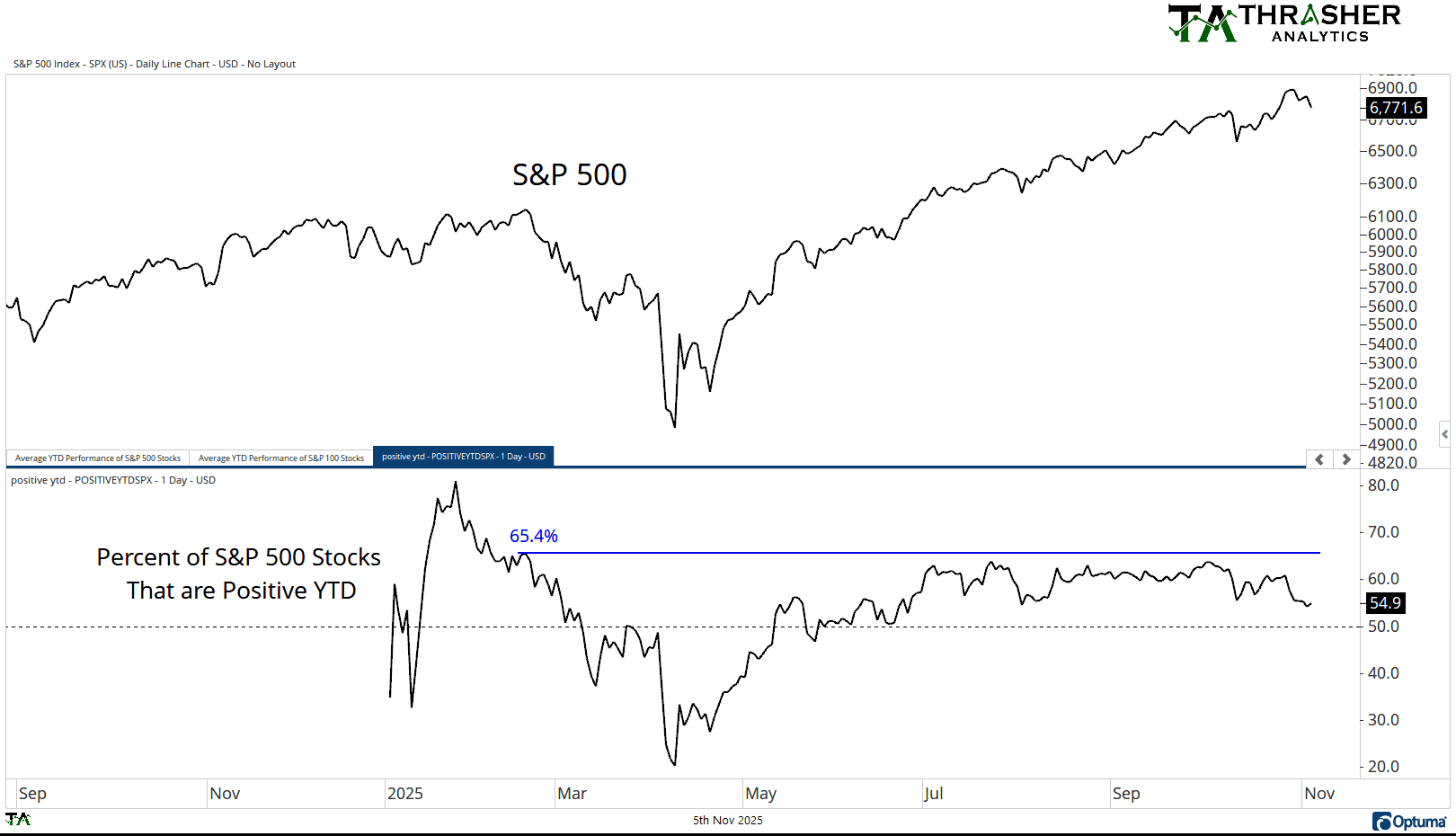

Earlier this year, roughly two-thirds of the index was positive year-to-date. Now, even with the index still close to its highs, only about half of the stocks are still up YTD. A smaller group of names is doing most of the work.

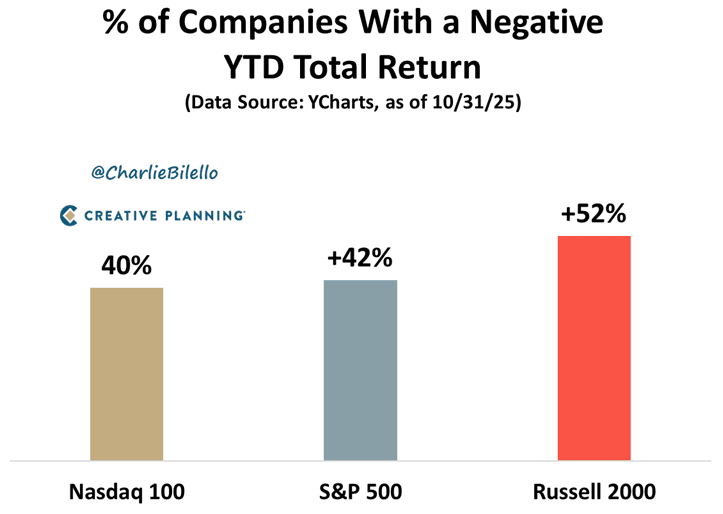

This isn’t new. In October, the major indices hit new highs while a large share of individual stocks did not. About 40% of the Nasdaq 100, 42% of the S&P 500, and more than half of the Russell 2000 were negative for the year at that point. The market has been getting narrower for months.

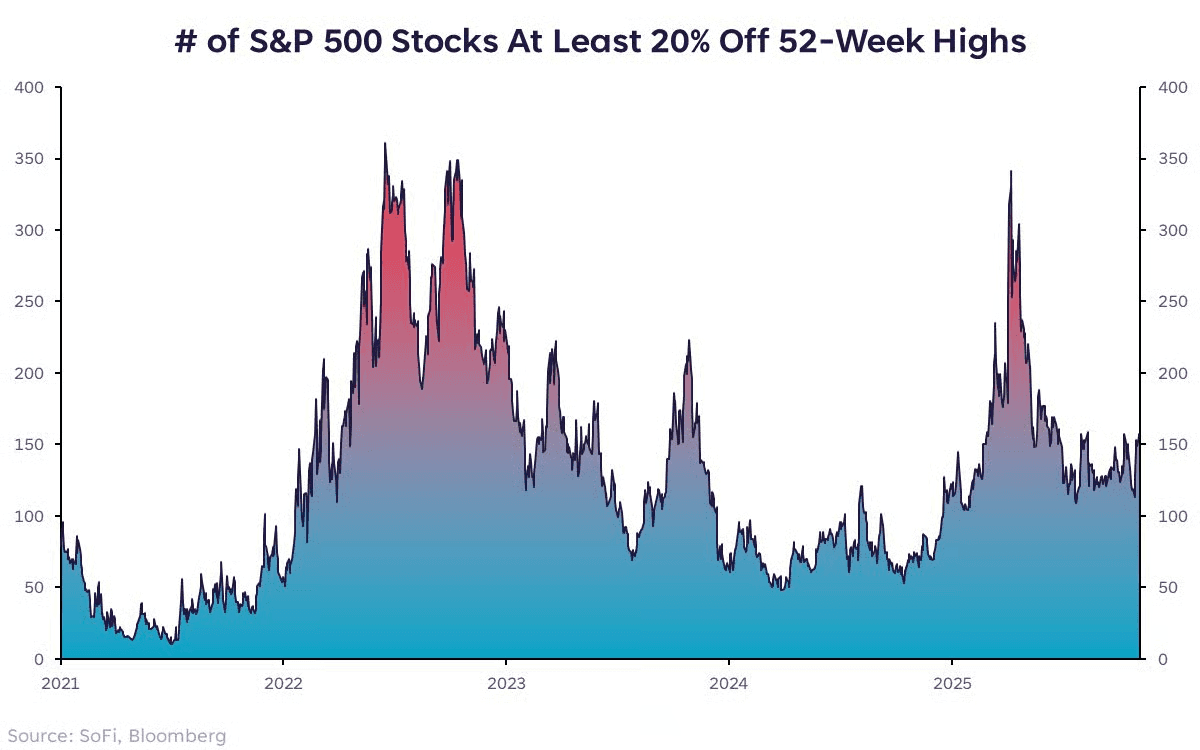

You can see it in the decline from recent highs. More than 150 stocks in the S&P 500 are down at least 20% from their 52-week highs. That is nearly double what we saw last year. Leadership is concentrated in only a handful of names.

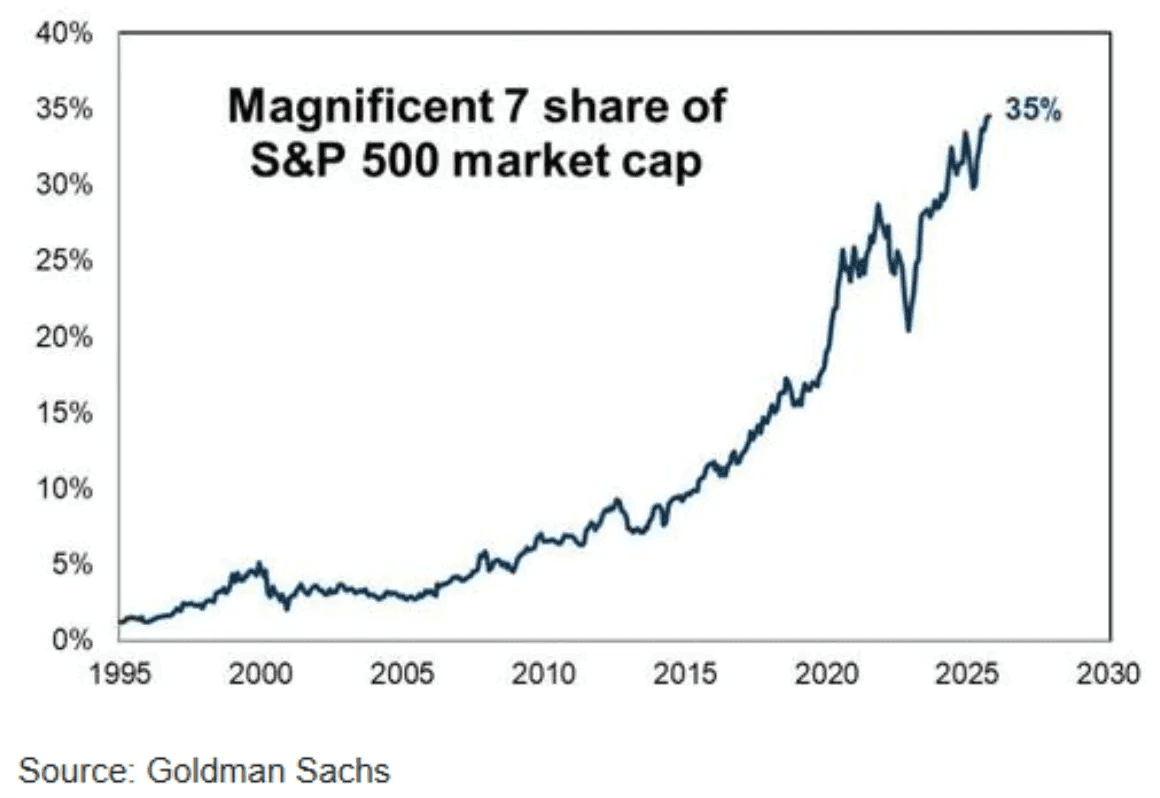

The market has been carried by just a few giants. The Mag 7 now make up more than 35% of the entire index. But this is not the same as the market being held up by one narrow theme or one risky bet. These companies run huge, diverse businesses. They touch cloud, AI, chips, hardware, software, and massive consumer platforms. They are some of the strongest and most durable companies in the world.

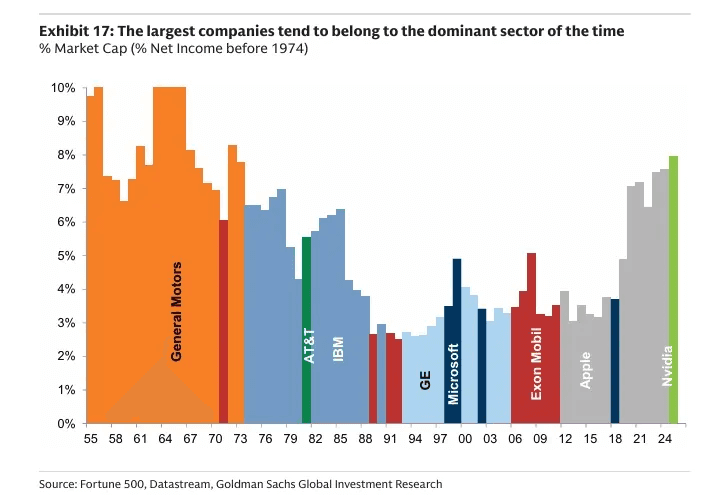

We’ve seen this before. When cars became popular, General Motors became the biggest company and stayed on top for years. When computers took off, IBM did the same.

If AI is a real, lasting shift, then companies like Nvidia will stay on top for a long time. The demand for AI chips and infrastructure is only just getting started. If this trend continues even halfway as expected, they remain the center of the new economy.

But when the market depends too much on just a few big stocks, the whole market becomes fragile. Those big names are basically holding everything up. So if they start to fall, the rest of the market usually follows. The Mag 7 just had their weakest week since April, falling more than 3%.

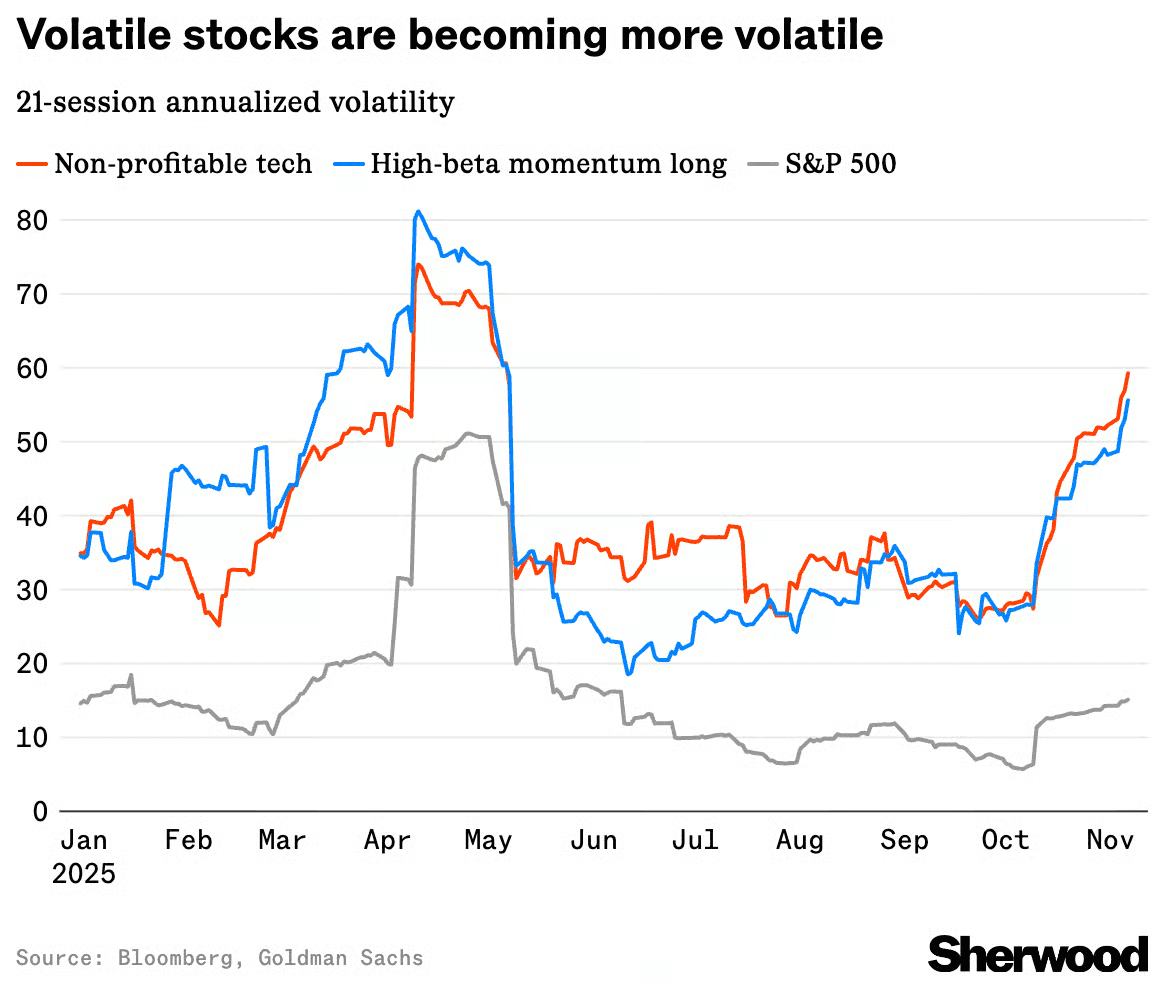

High beta and unprofitable tech stocks were hit even harder than the broad market. These are the names that tend to move the most when sentiment shifts, and this time was no different. Volatility in this group has jumped back to levels we last saw during the tariff shock years, because investors always pull back from the highest-risk areas first.

For many of these stocks, the declines have been sharp. It’s not unusual to see individual names down 15%, 20%, or even 30% in a matter of weeks or even days.

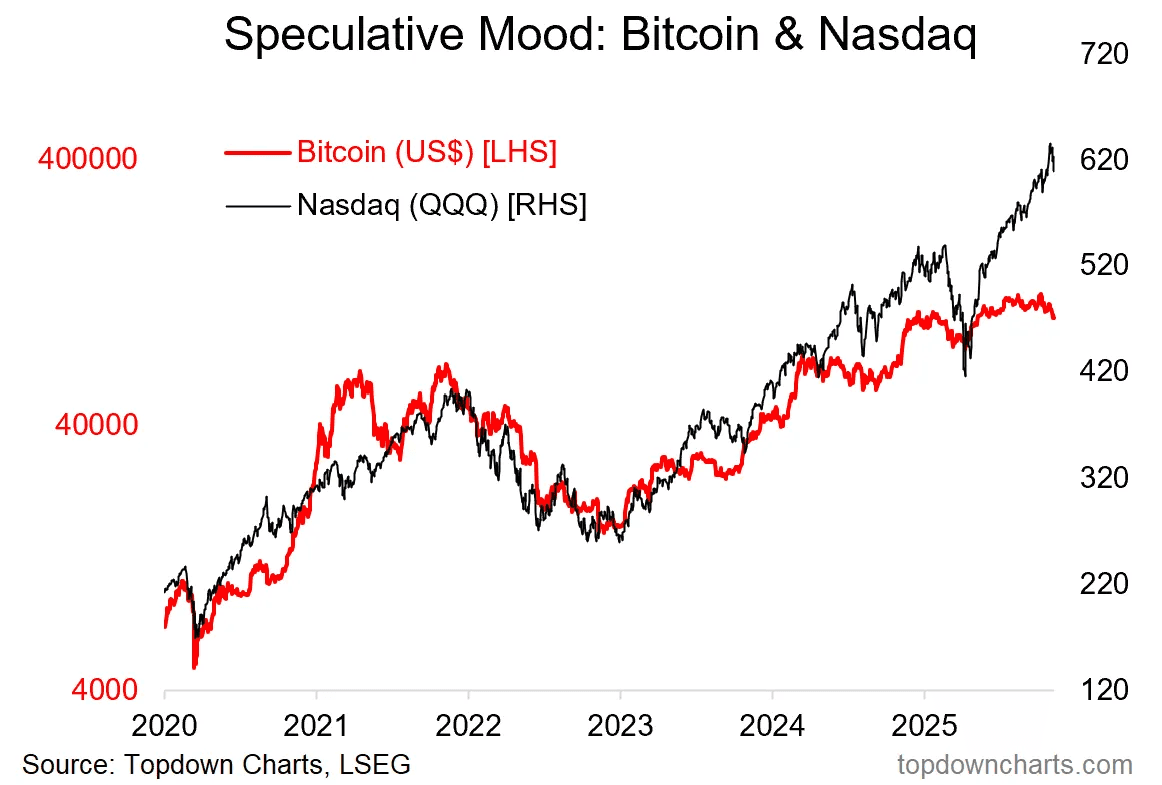

Bitcoin has been weak. It fell below its 200-day moving average and is now more than 20% below its recent peak. Bitcoin often moves first when investors become more or less willing to take risk, so this drop suggests risk appetite has cooled.

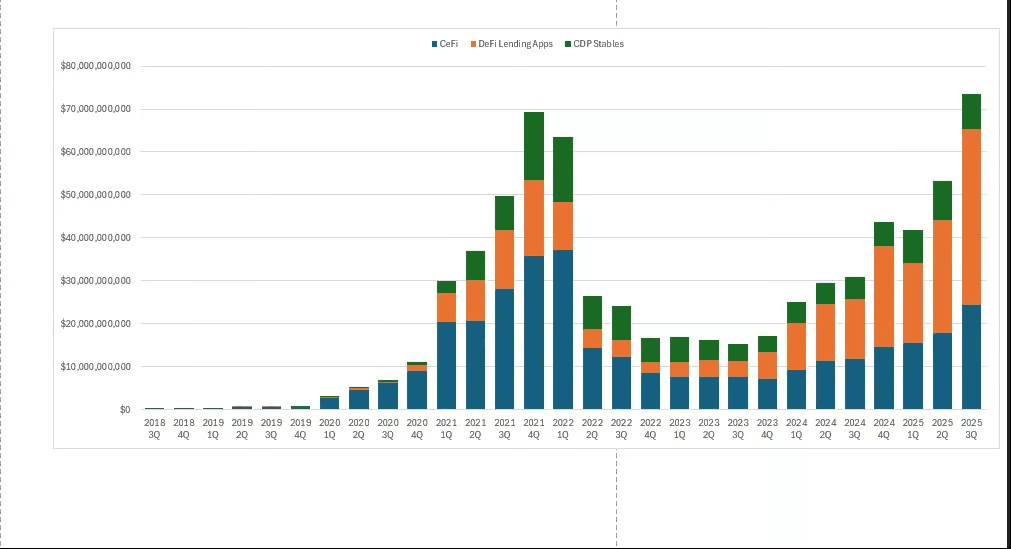

A big part of the decline came from leverage. Crypto borrowing surged, which means a lot of traders were using debt to amplify their positions. High leverage makes the market more fragile. When prices started to fall, those positions got liquidated, which forced more selling and made the drop worse.

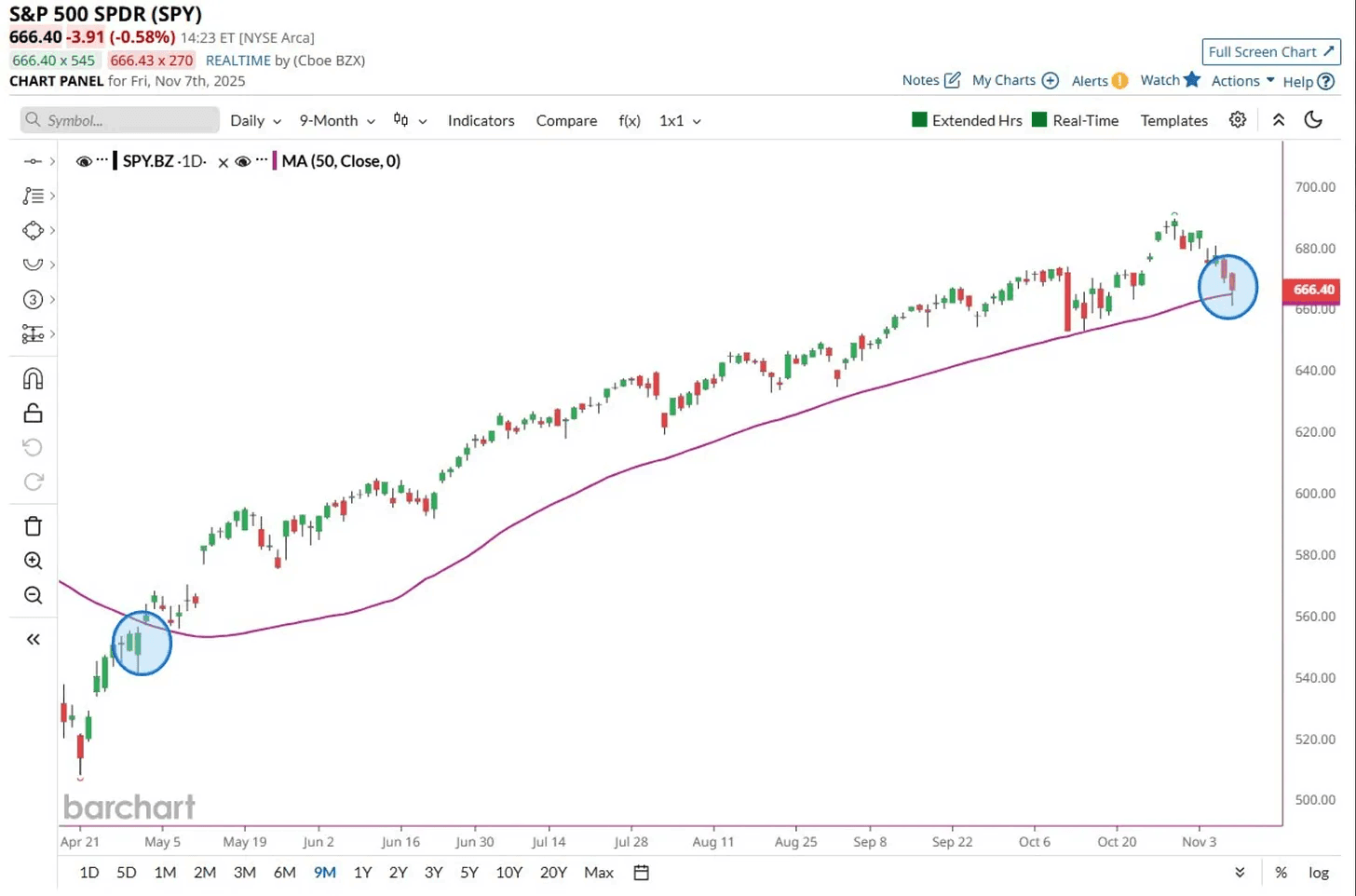

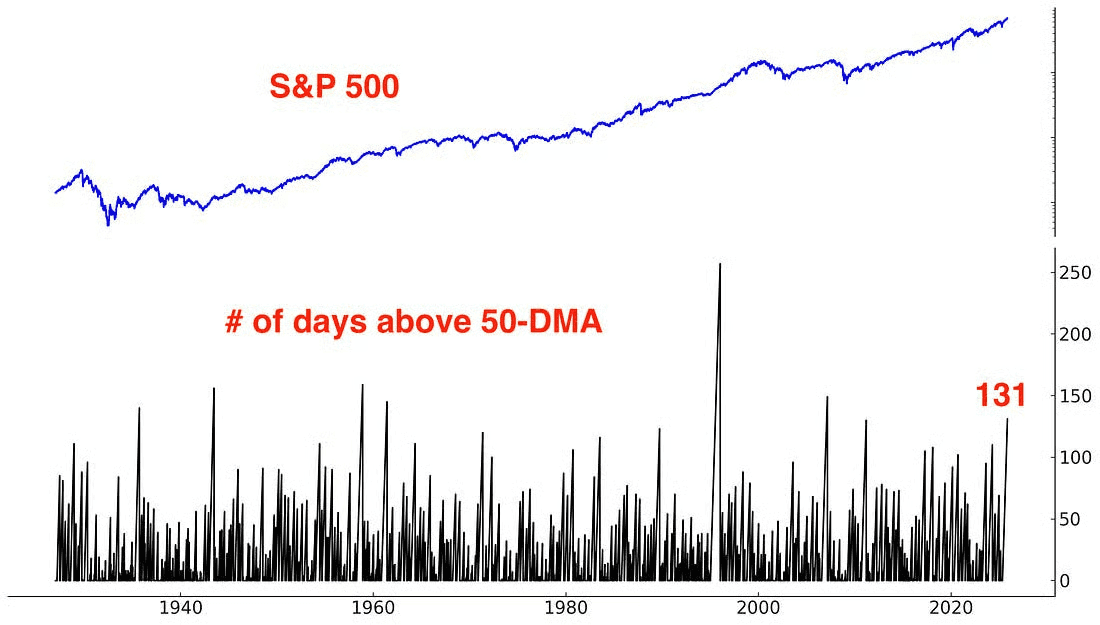

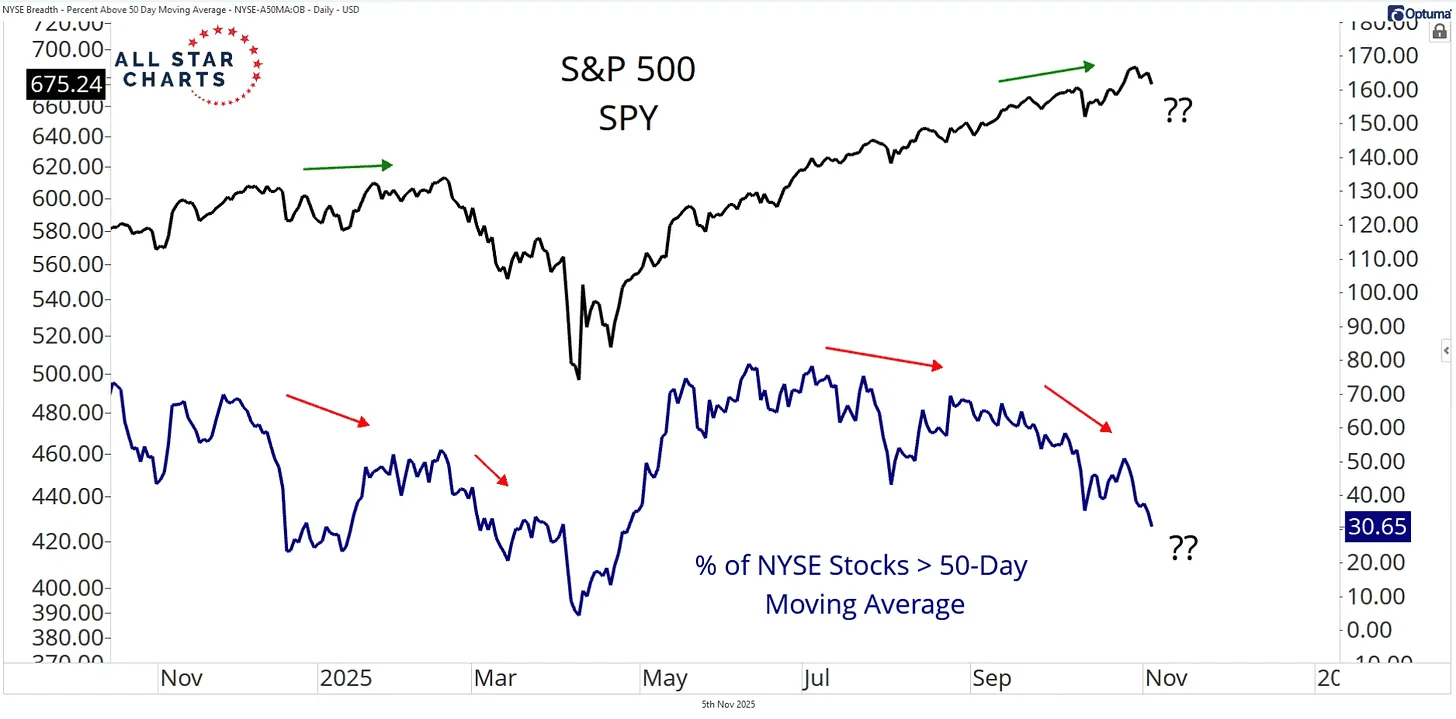

The S&P 500 had been above its 50-day moving average for 131 trading sessions. Streaks like that don’t last forever. On Friday, the index briefly broke below the 50-day for the first time since April. It did manage to recover by the close, finishing back above that level. Now we watch to see if this support holds. As long as we’re above there’s absolutely no reason to be bearish.

But at the same time, more individual stocks are slipping below their own short-term trends. The index has held up better than what’s happening under the surface. That’s not what you want to see. Ideally, more stocks would be participating on the upside. Right now, participation is moving the other way.

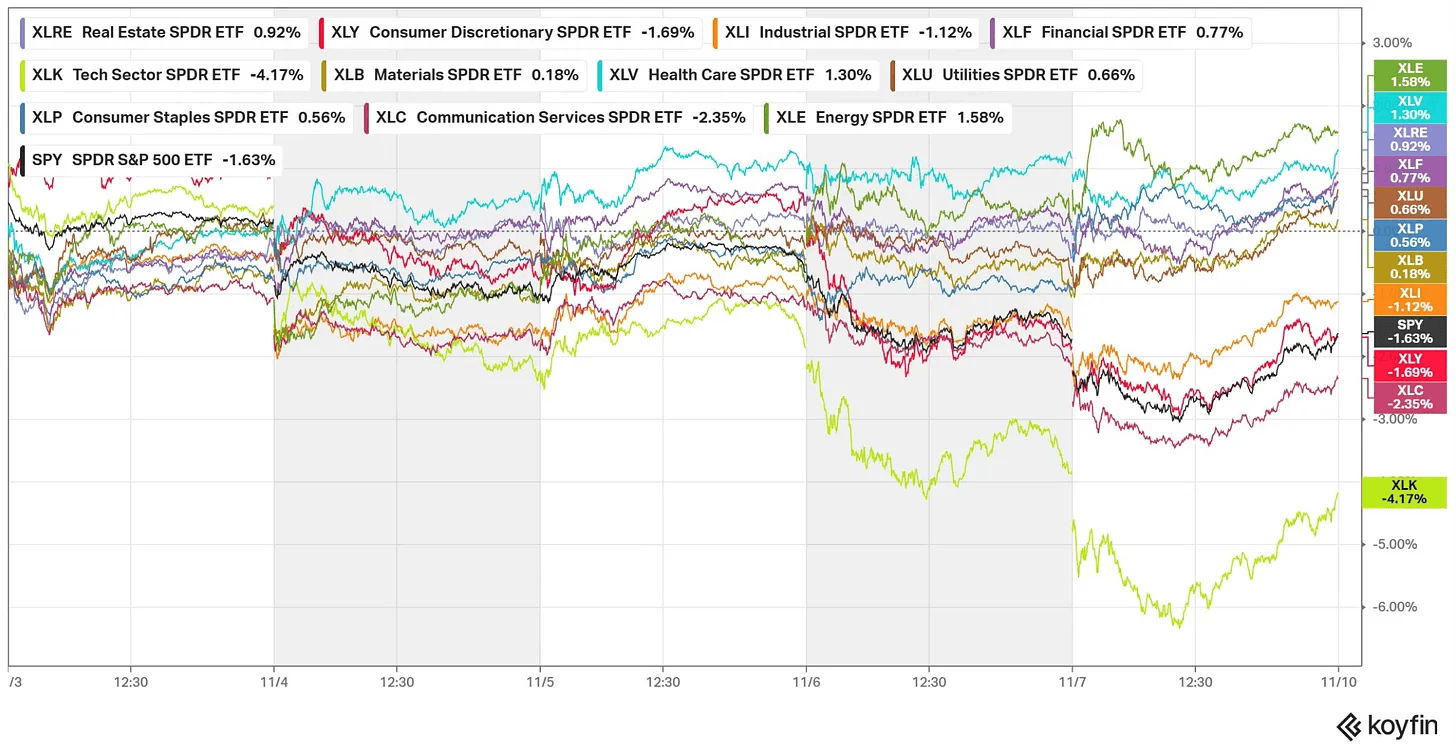

The good news is that money is starting to rotate. Tech was weak this week, but seven other sectors still went up. That means money is moving to new areas instead of leaving the market. It shows a shift in leadership, not a full market selloff.

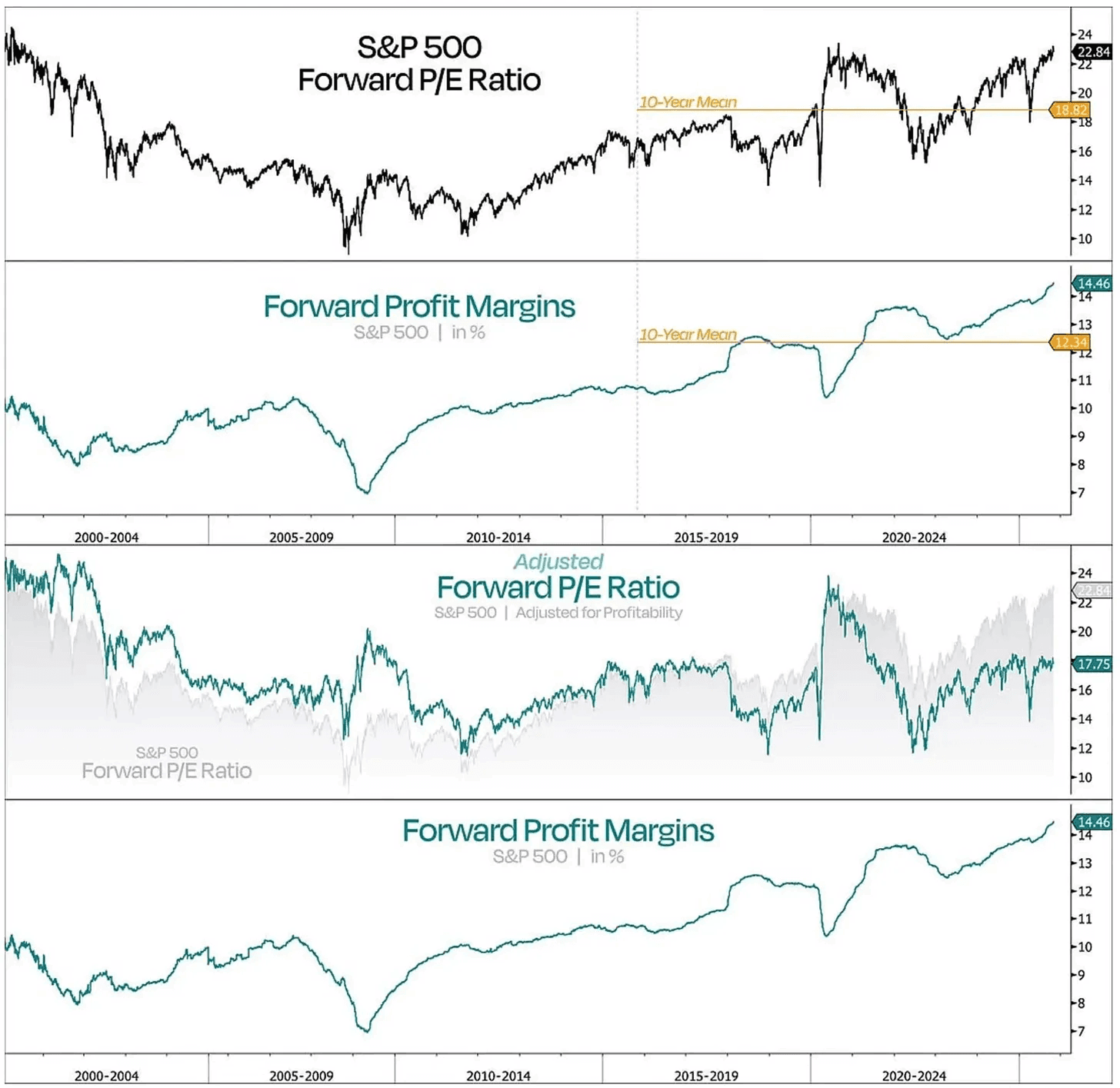

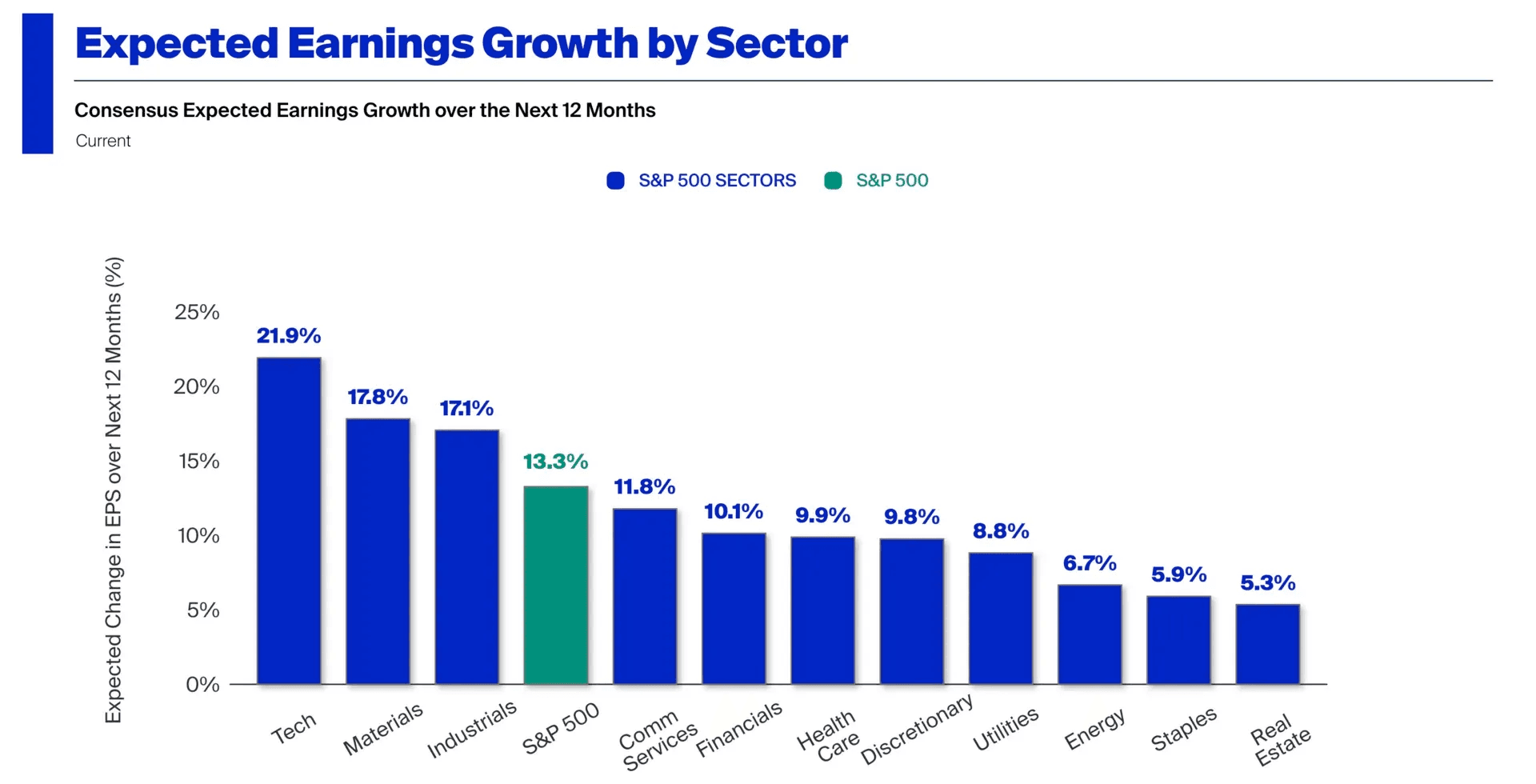

People love to yell “bubble” every time prices go up. But they usually leave out the most important part of the story. These companies are actually making a ton of money. Their earnings are strong and their profit margins are super high right now.

Earnings are beating estimates by 13.3% on average, the best margin in four years. That’s up from 8.2% last quarter. This should be a reason to be extra bullish, so you’d think.

Although, Q3 earnings are strong, it seems that the market doesn’t really care.

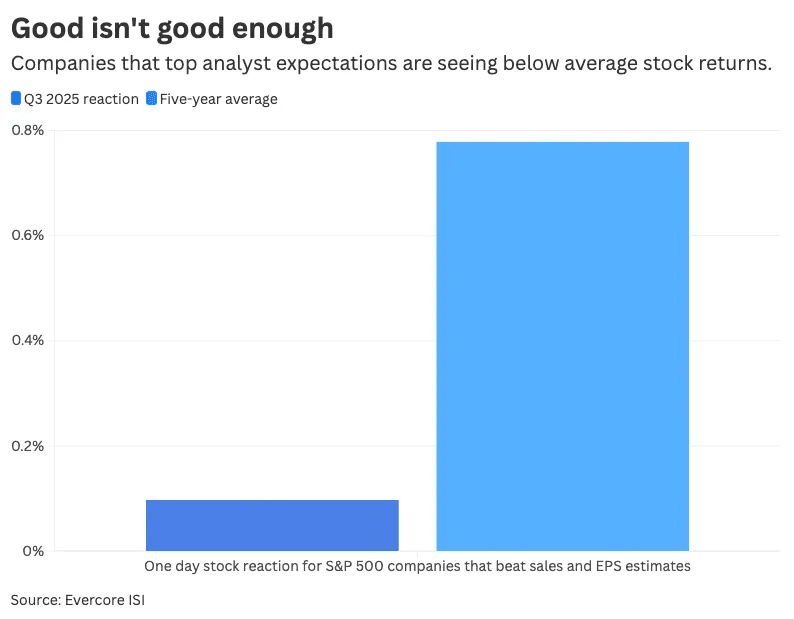

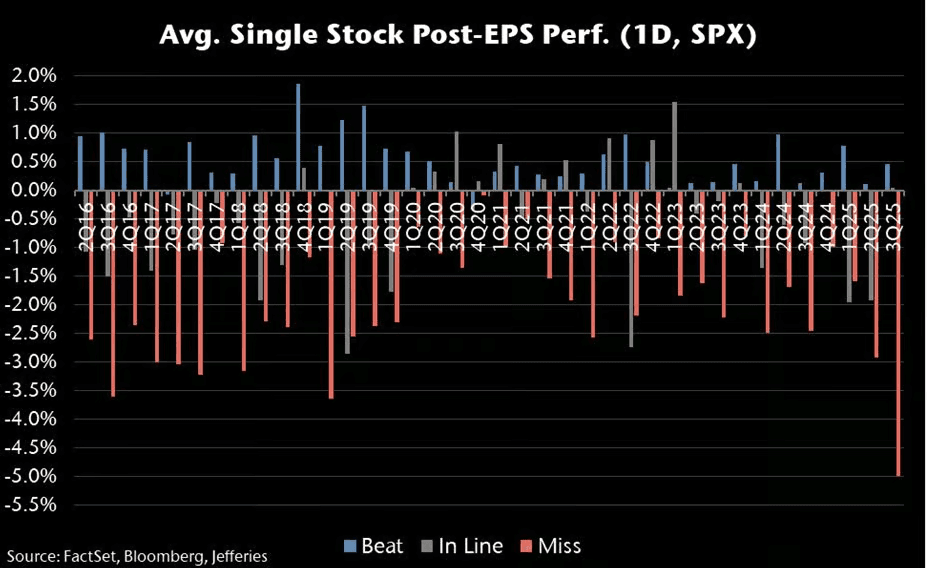

This is the best earnings season since 2021, with the highest percentage of companies beating estimates in years. Yet the reaction has been weak. Misses are getting punished hard. Beats are barely rewarded.

On average, an S&P 500 company that beats on both revenue and earnings is seeing just a 0.1% gain. Historically, that move has been closer to 0.8%.

At the same time, companies that mess up are getting punished. On average, when a company misses earnings, the stock falls about 5% the next day. That’s the biggest negative reaction of any quarter in the data. And that actually shows investors are paying attention. People are not blindly buying everything.

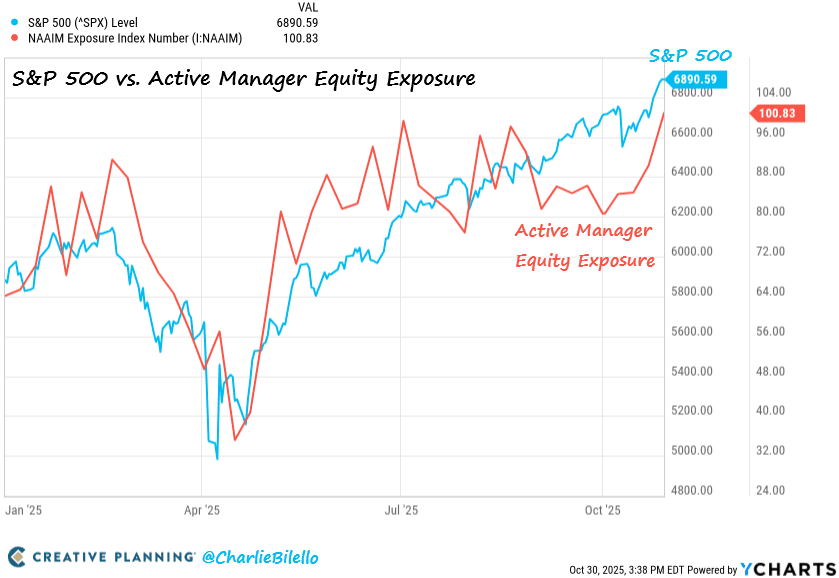

Positioning tells a similar story. Active managers went from underweight stocks in April to heavily overweight. The last time positioning was this stretched, the market corrected about 10% shortly after. That means the market is more vulnerable in the near term because everyone is crowded on the long side.

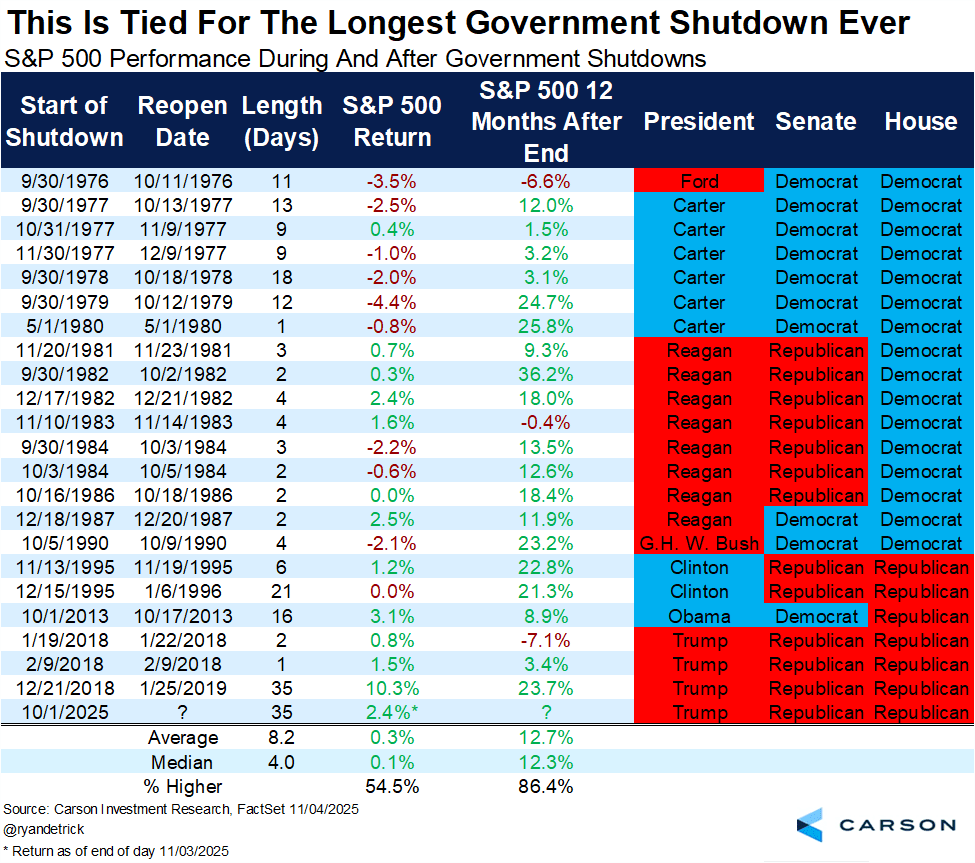

The government is still shut down, and it’s now the longest shutdown in history. The longer it continues, the more disruptions it will create. That becomes a risk for the market.

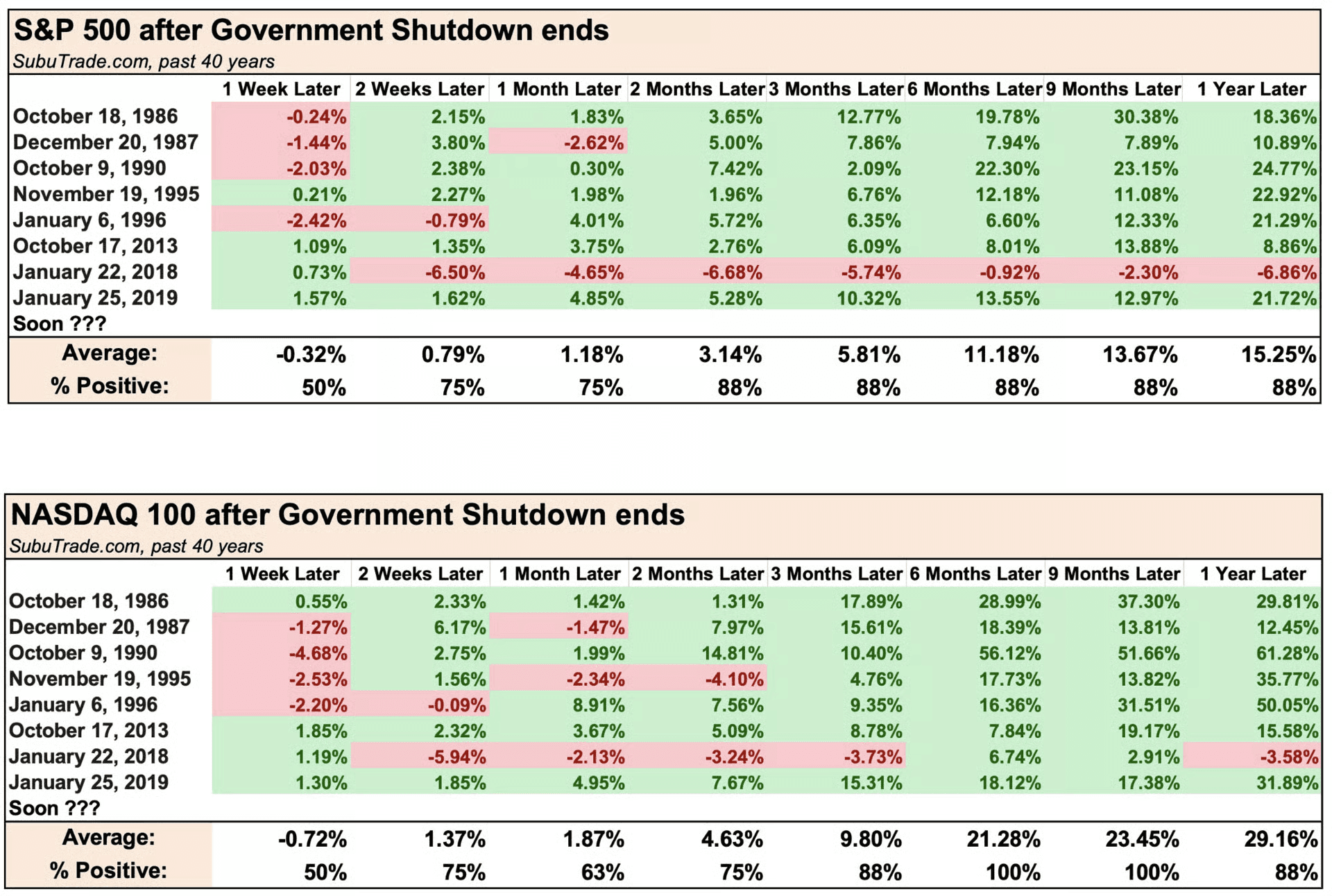

Historically, when government shutdowns end, stocks often rebound, even if the first week can be choppy. In past episodes, the NASDAQ 100 was higher 6 to 9 months later every single time.

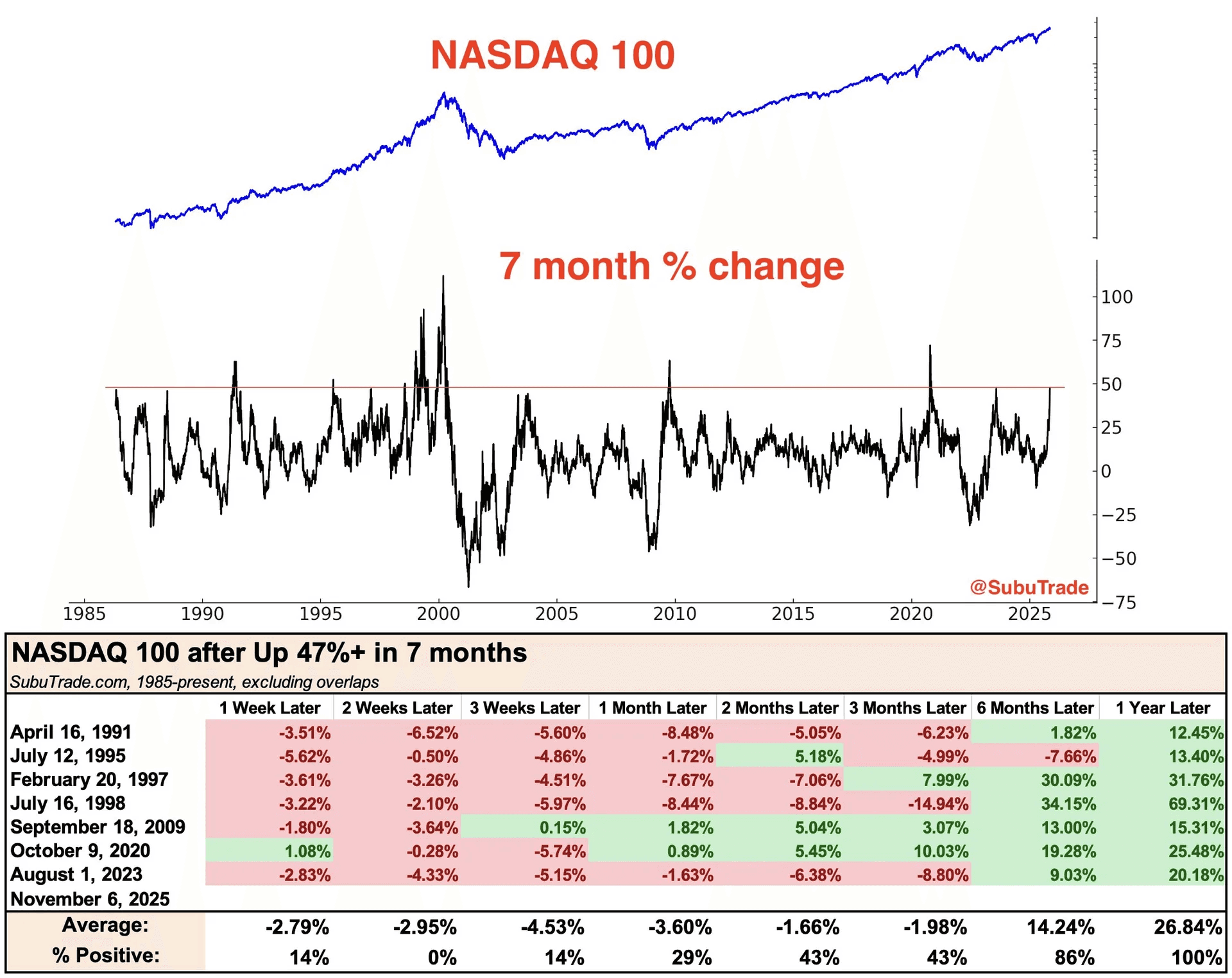

The NASDAQ 100 has had a big run, up 47% in seven months. Historically, rallies like this often pause with a short pullback near-term. But looking out a year, the index has always ended up higher afterward. So, it’s possible that we’ll be range-bound for the foreseeable future.

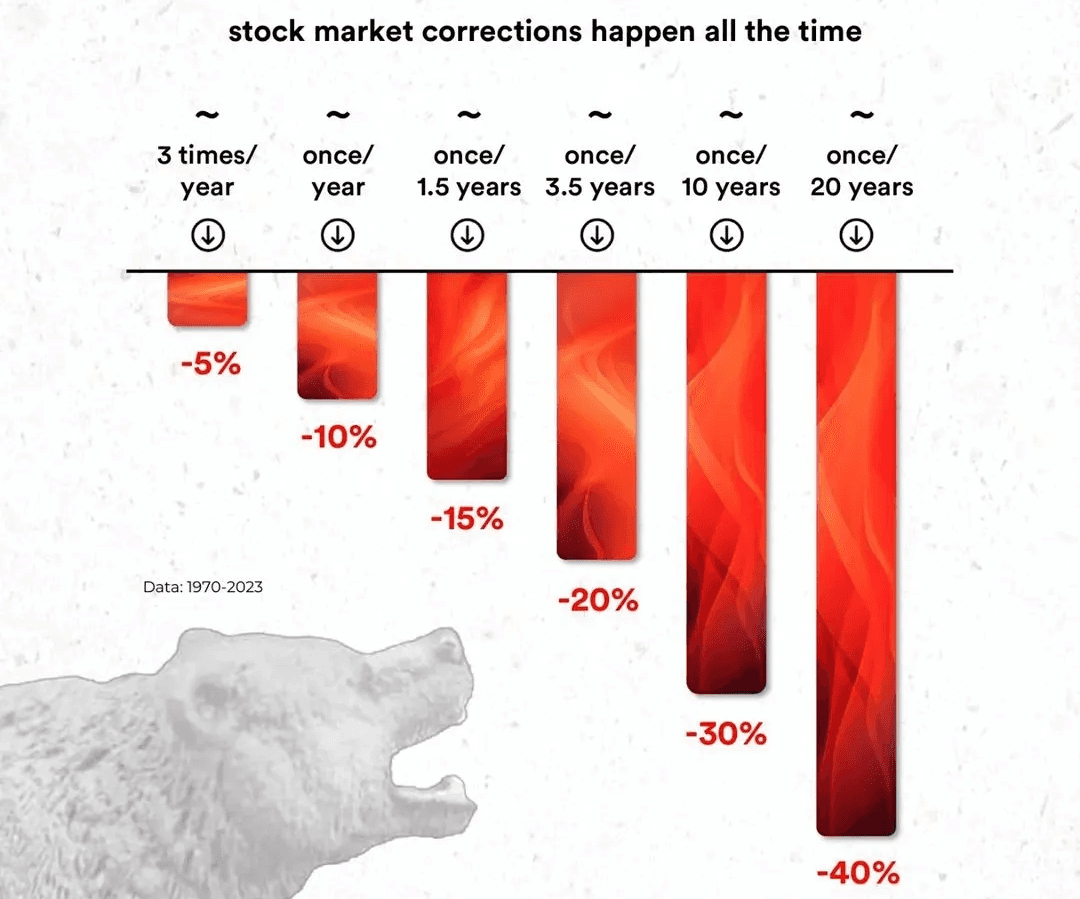

But corrections are completely normal. They happen all the time. Low volatility and record highs feel great, but they can make you forget that markets don’t move in straight lines. Every market goes through drawdowns. That’s part of the process, not a sign that something is wrong. So far, this is a pretty standard dip for the overall market.

Even though the market has been really volatile and there are some signs to be a little cautious in the short term, the fundamentals haven’t changed. Nothing important has broken. So far, this looks like a normal pullback. Markets never go straight up. This kind of pause is part of every long-term move.

Investors have just forgotten what a pullback feels like. We haven’t had a meaningful one since April. The market has mostly gone straight up since spring. When things go up for a long time, even a small drop can feel worse than it actually is. But this is part of a normal market cycle. That is the price of admission to being in the market.

But accepting pullbacks doesn’t mean you just sit there and take every hit. The key is to limit drawdowns. You don’t need to call the exact top or bottom. You just want to avoid the big, painful losses that take forever to recover from.

Previous Updates

View All

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap

- A Few Portfolio Changes