Go Back

Lin

Weekly Market Update: Momentum Reset

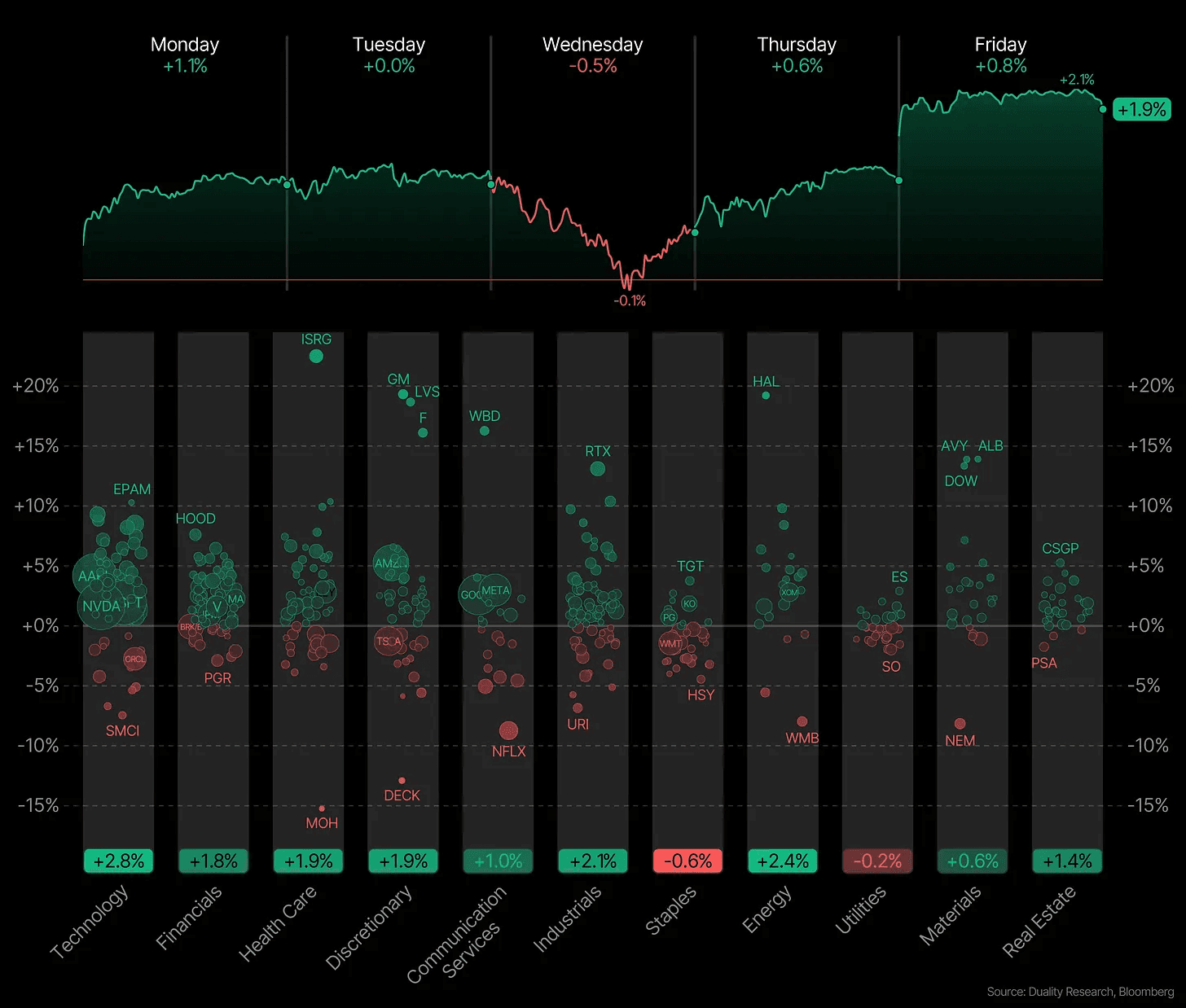

The S&P 500, Nasdaq, and the Dow all closed at new all-time highs this week.

And while the headline indices looked calm, the path to get there was anything but. We saw some real volatility mid-week, especially in momentum and growth names, before the market recovered.

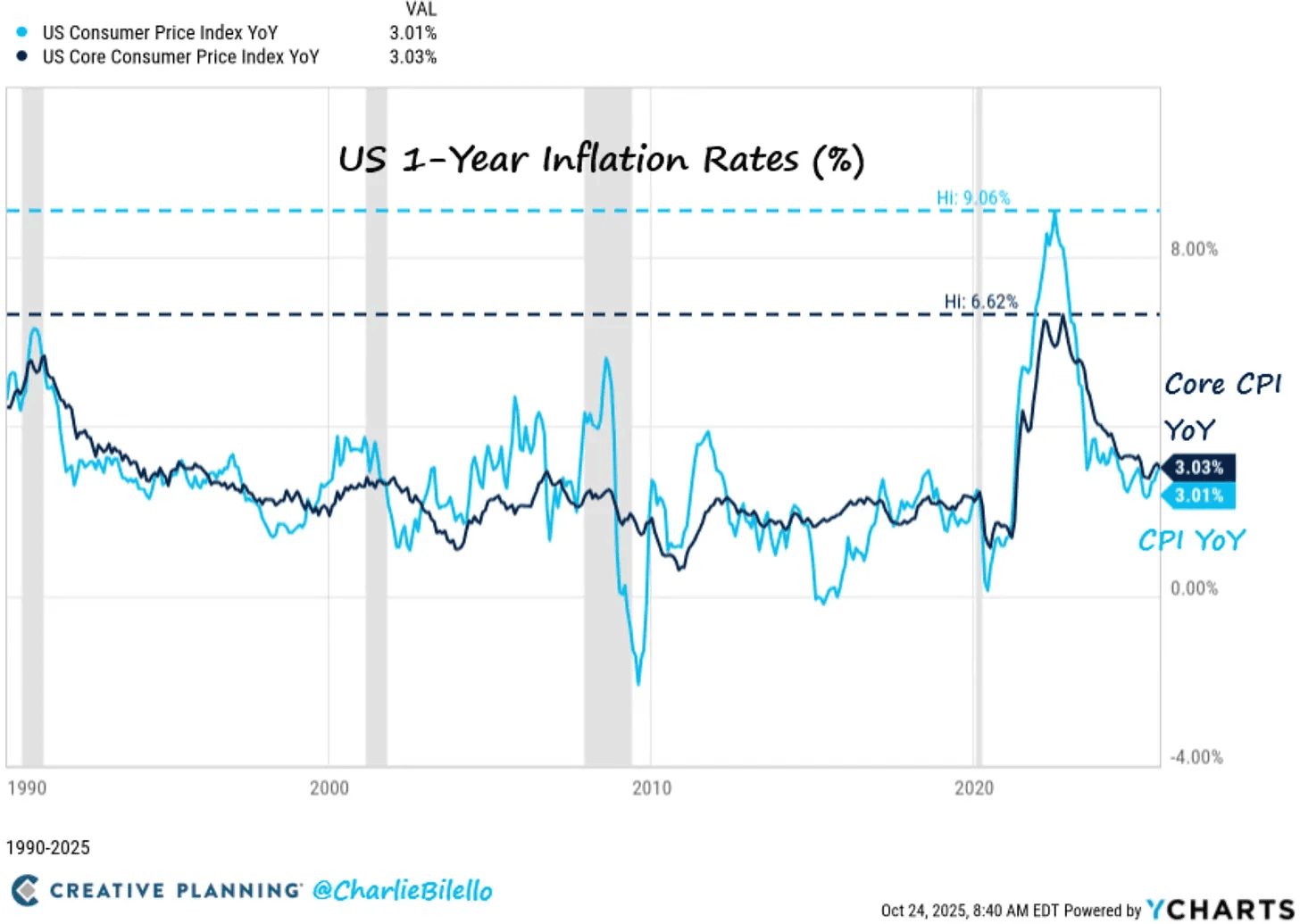

A big driver was the latest inflation report. CPI came in at 3.0% year over year in September, slightly below expectations. It’s still higher than the Fed would like, but the direction matters more than the level here. The trend is still moving lower, and markets are treating that as confirmation that the Fed can continue to cut rates.

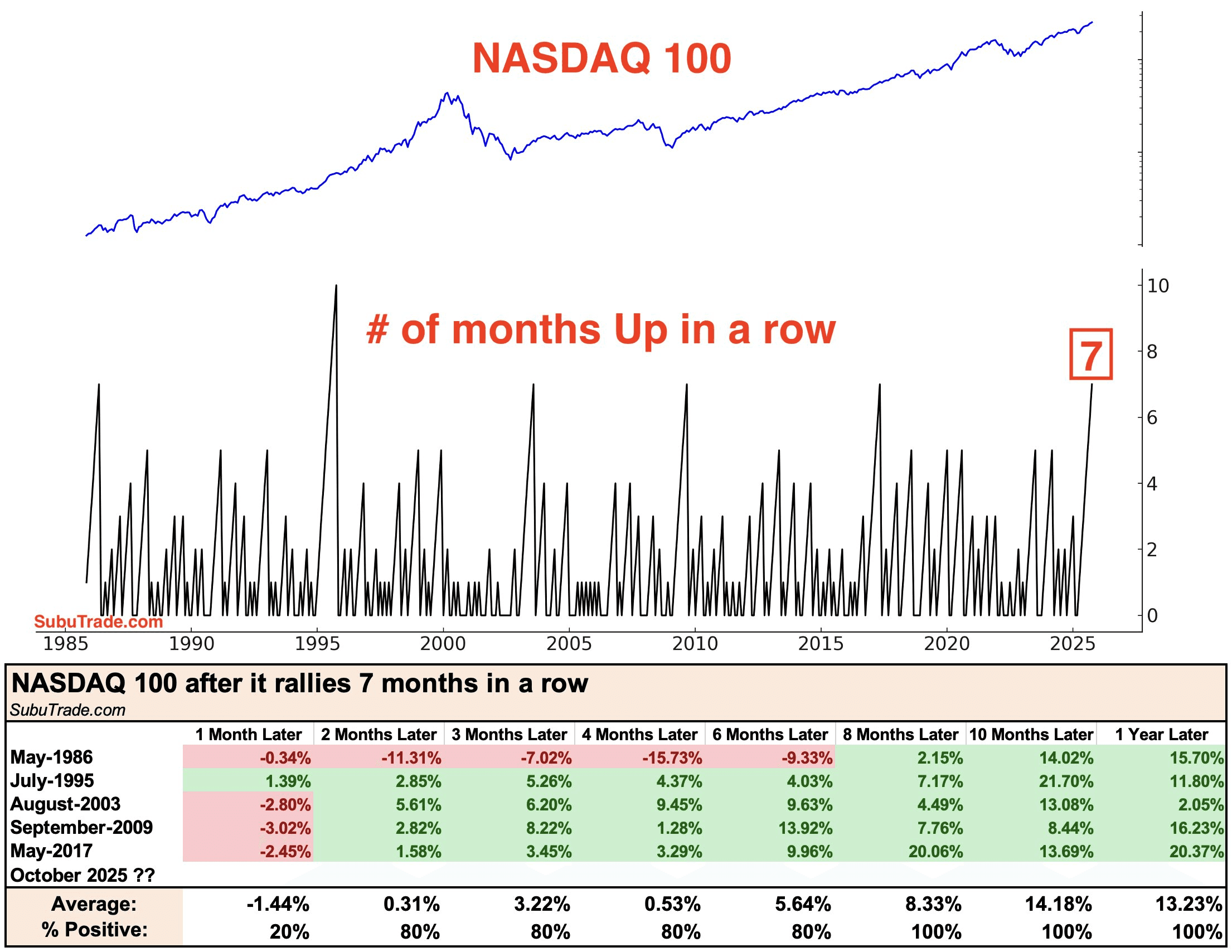

The NASDAQ is now on track to finish its 7th straight positive month. This doesn’t happen often. Historically, when the NASDAQ has rallied for seven months in a row, short-term returns have been mixed, but looking out a few months and especially a year later, it has been higher every time.

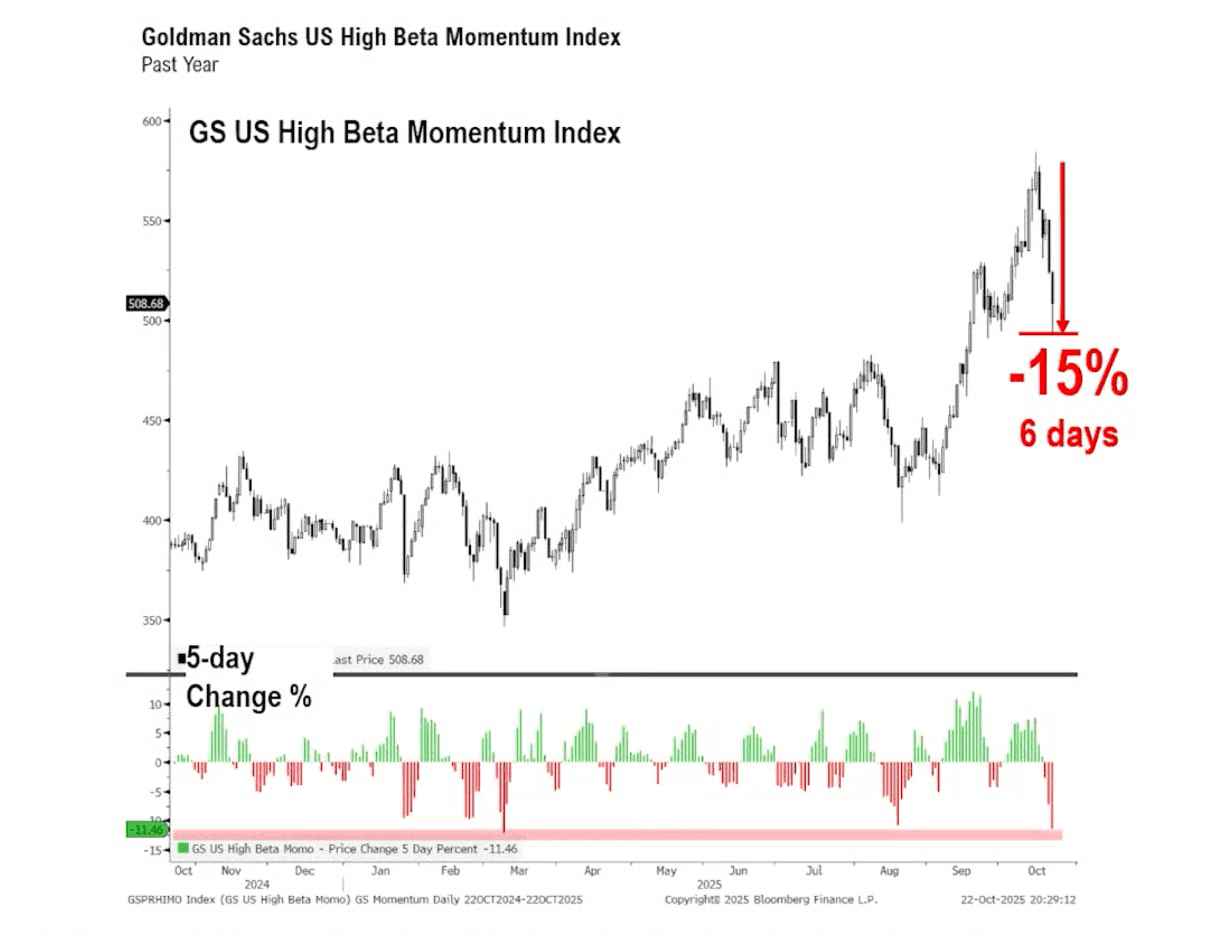

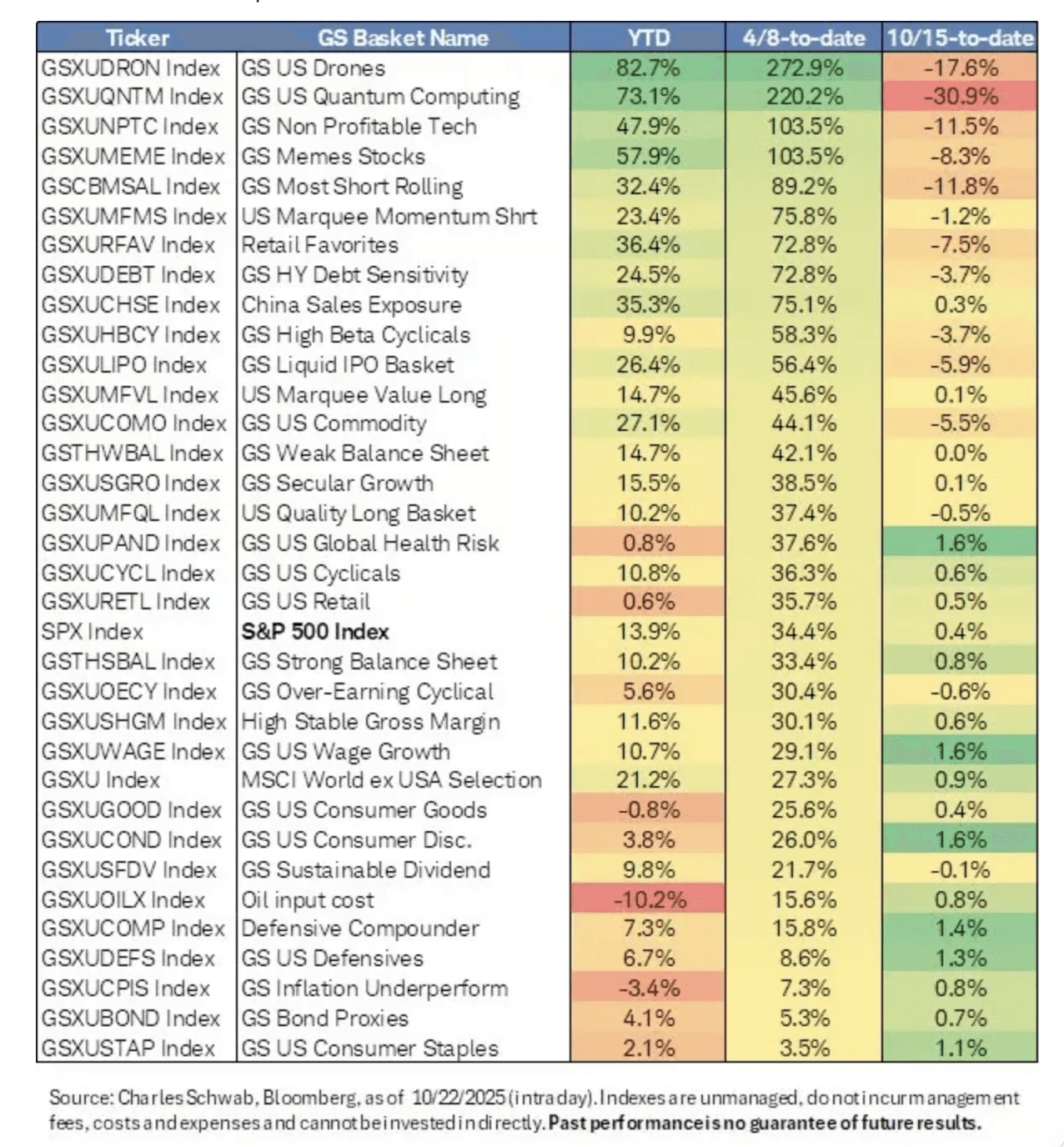

But while the major indices barely moved, we just saw a sharp pullback under the surface. The Goldman Sachs Momentum Index dropped about 15% in six days, and a lot of individual names fell 30–40% during that stretch. The selling was fast and concentrated. But the chances are high that this might be the end of the pullback. This type of sharp reset usually clears the excessive leverage, which increases the likelihood that the pullback is nearing its end.

Here’s another way to look at it: Investors rotated out of the high-flyers and into more defensive names. That’s actually a healthy sign. Strong bull markets tend to move in waves, not all at once.

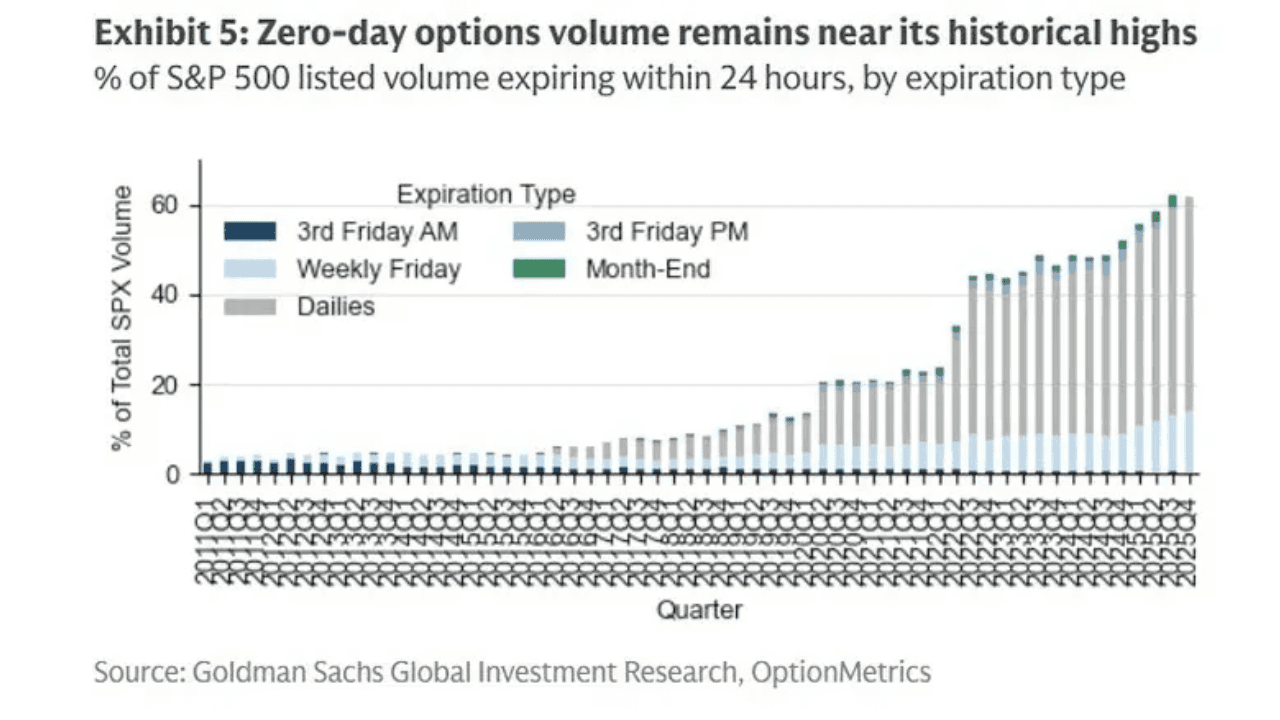

Speculation is still very present. Zero-day-to-expiration options trading remains extremely heavy. These are essentially ultra-short-term leveraged bets. They add fuel on the upside but also increase fragility if news turns suddenly.

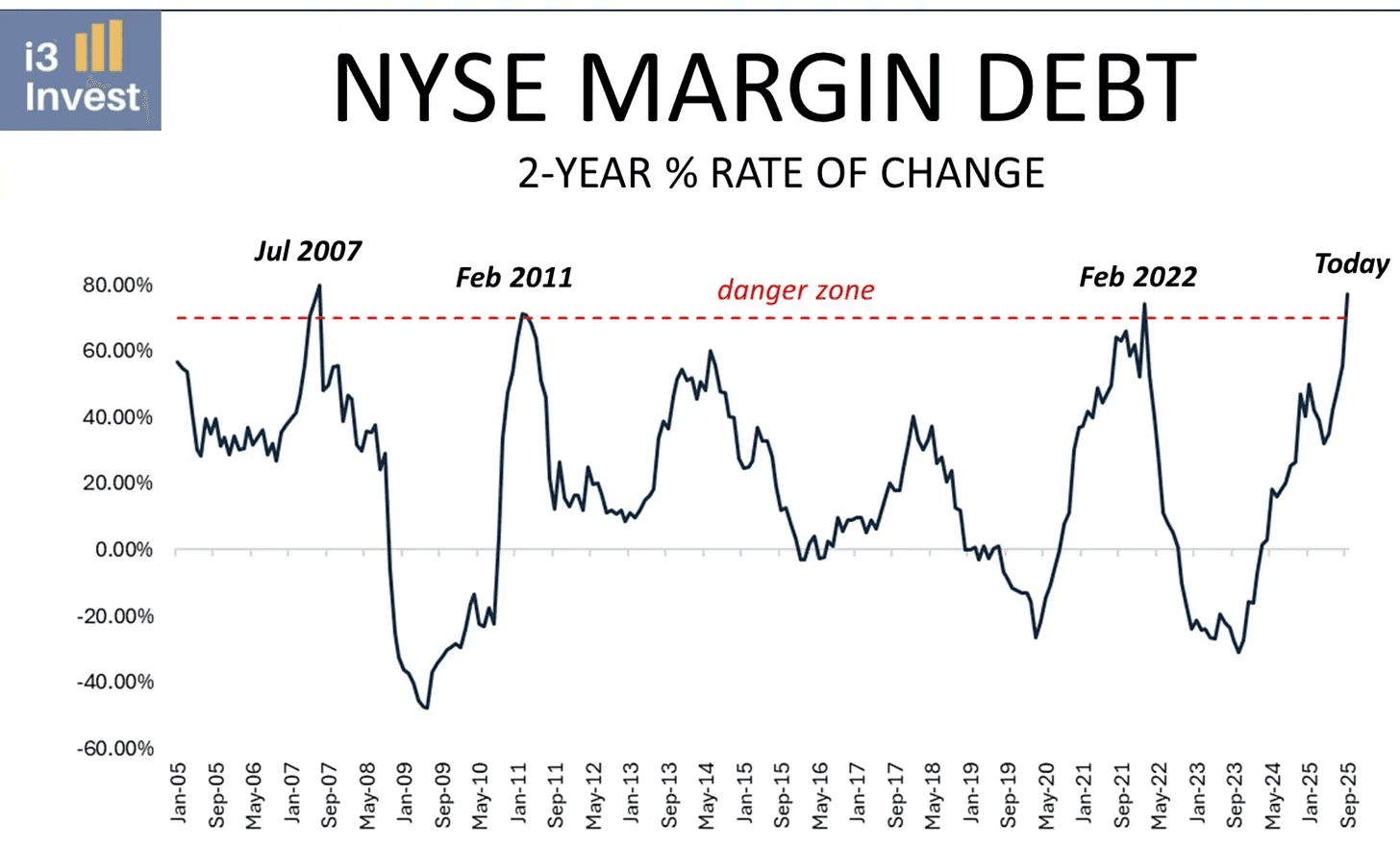

Margin debt is also rising. Rising leverage doesn’t kill an uptrend on its own, but it does make the market more volatile.

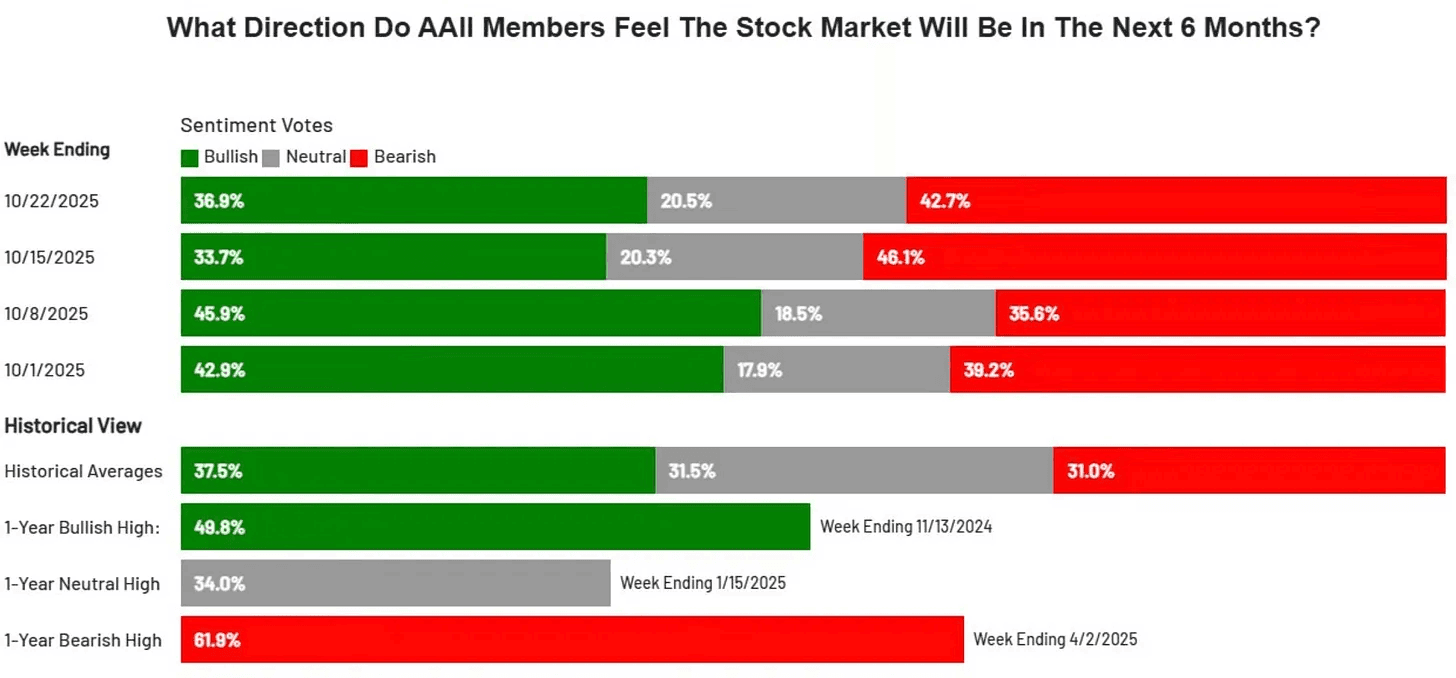

What’s interesting is that even as the market hits new highs, sentiment isn’t euphoric. The AAII investors survey still shows more bears than bulls. In other words, a lot of people still don’t believe in this rally. Historically, bull markets tend to end when everyone becomes overly confident. We’re definitely not there.

If you wanted one single signal as to why this bull market likely isn’t over, this is it.

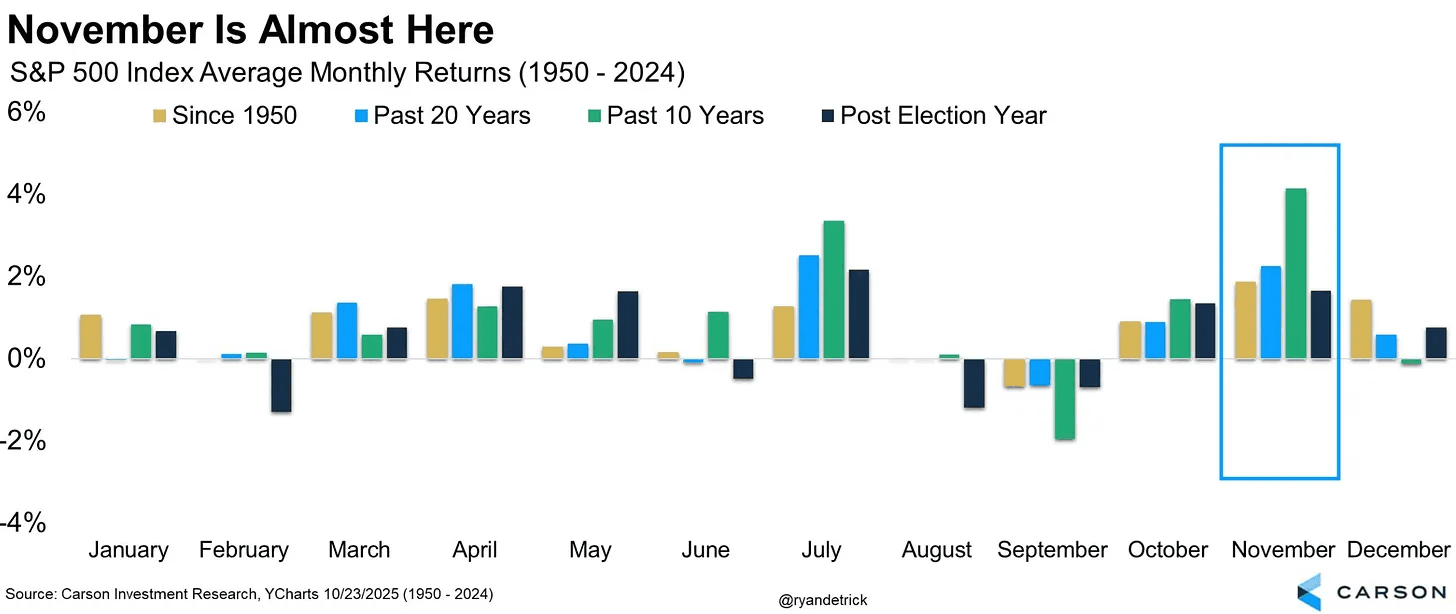

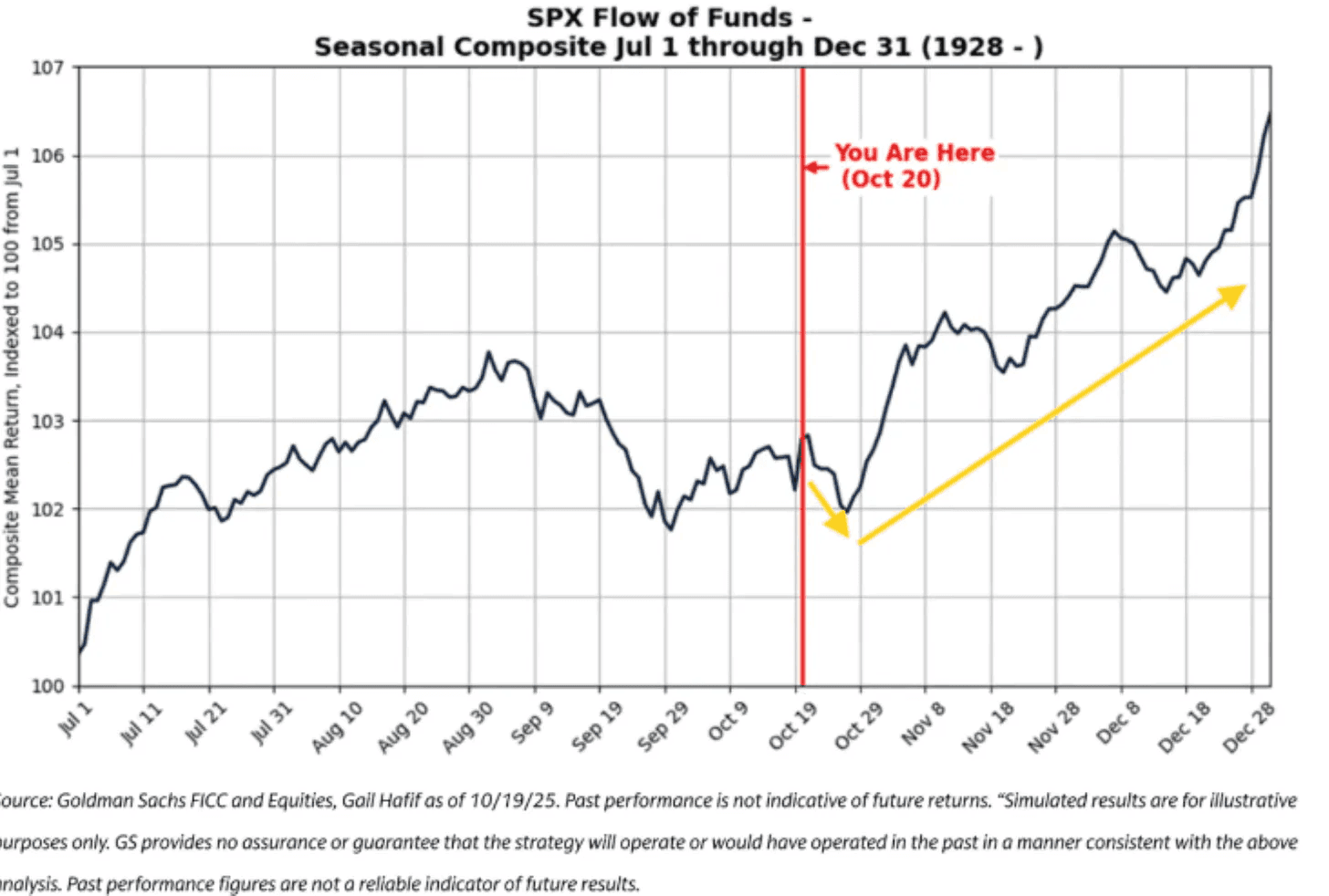

Seasonality is also in play now.

November has historically been the best month for the S&P 500 on average since 1950.

This aligns with the typical year-end pattern in which institutional investors, funds, and asset managers reposition portfolios before the close of the calendar year. This is the time when funds start looking at their performance and don’t want to be caught underexposed. That often leads to more buying and “chasing” into year-end.

That’s because history shows that capital often rotates toward equities in the final months of the year. The “year-end chase” is a real and recurring pattern going back nearly a century.

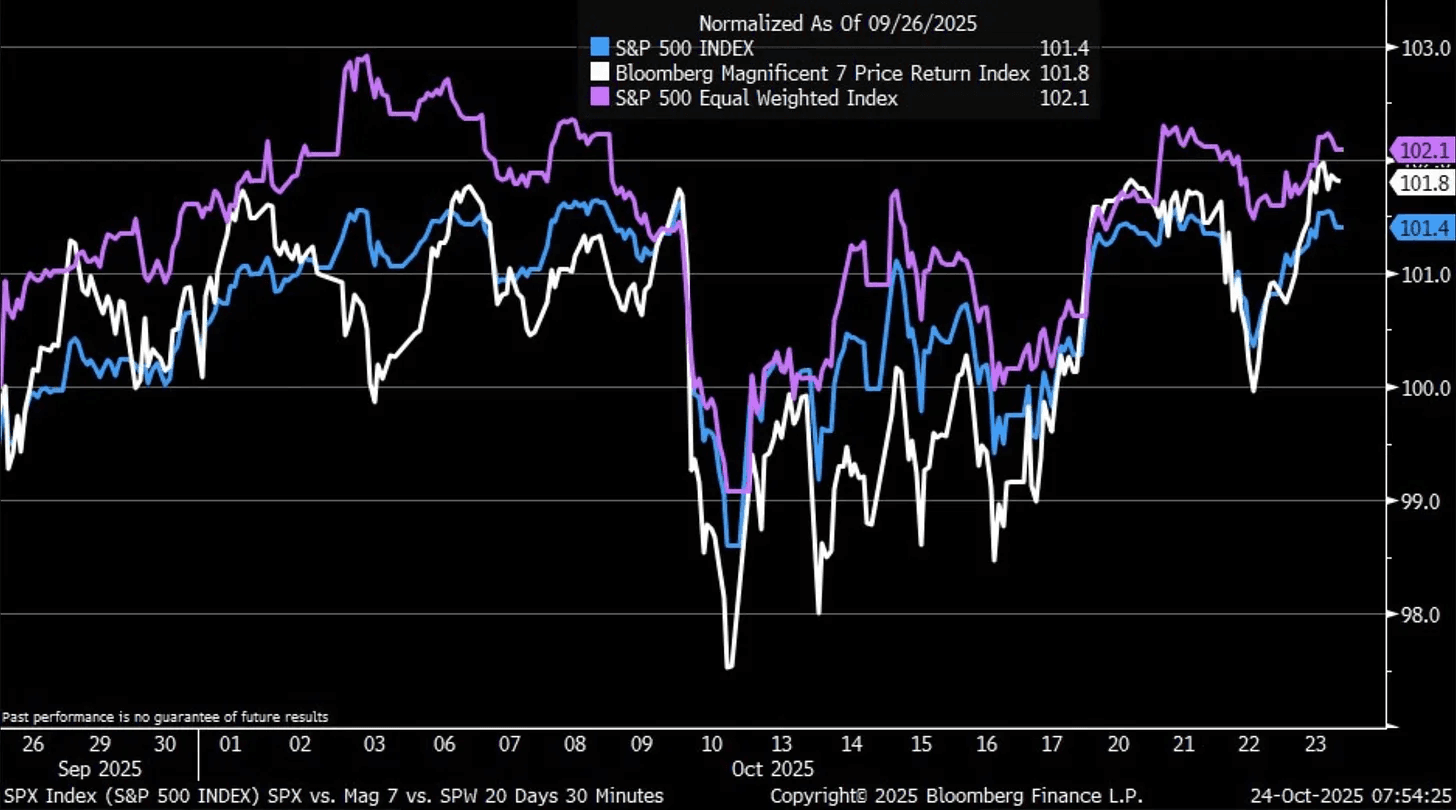

Under the surface, market breadth is improving. Equal-weighted versions of the S&P 500, Nasdaq, and Dow have also hit new highs. That’s a healthy sign because it means the rally is broadening beyond just a few mega-cap tech stocks.

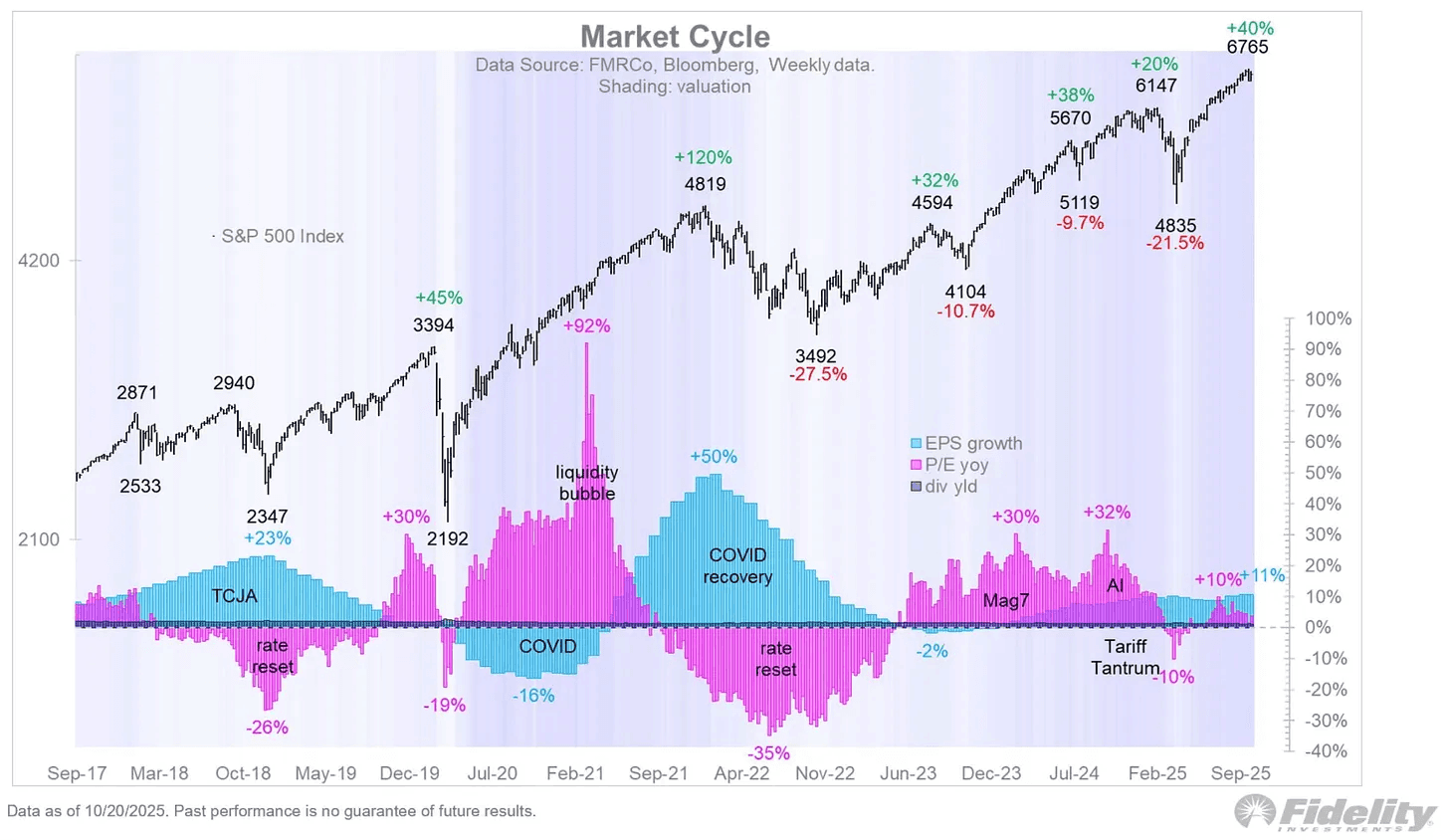

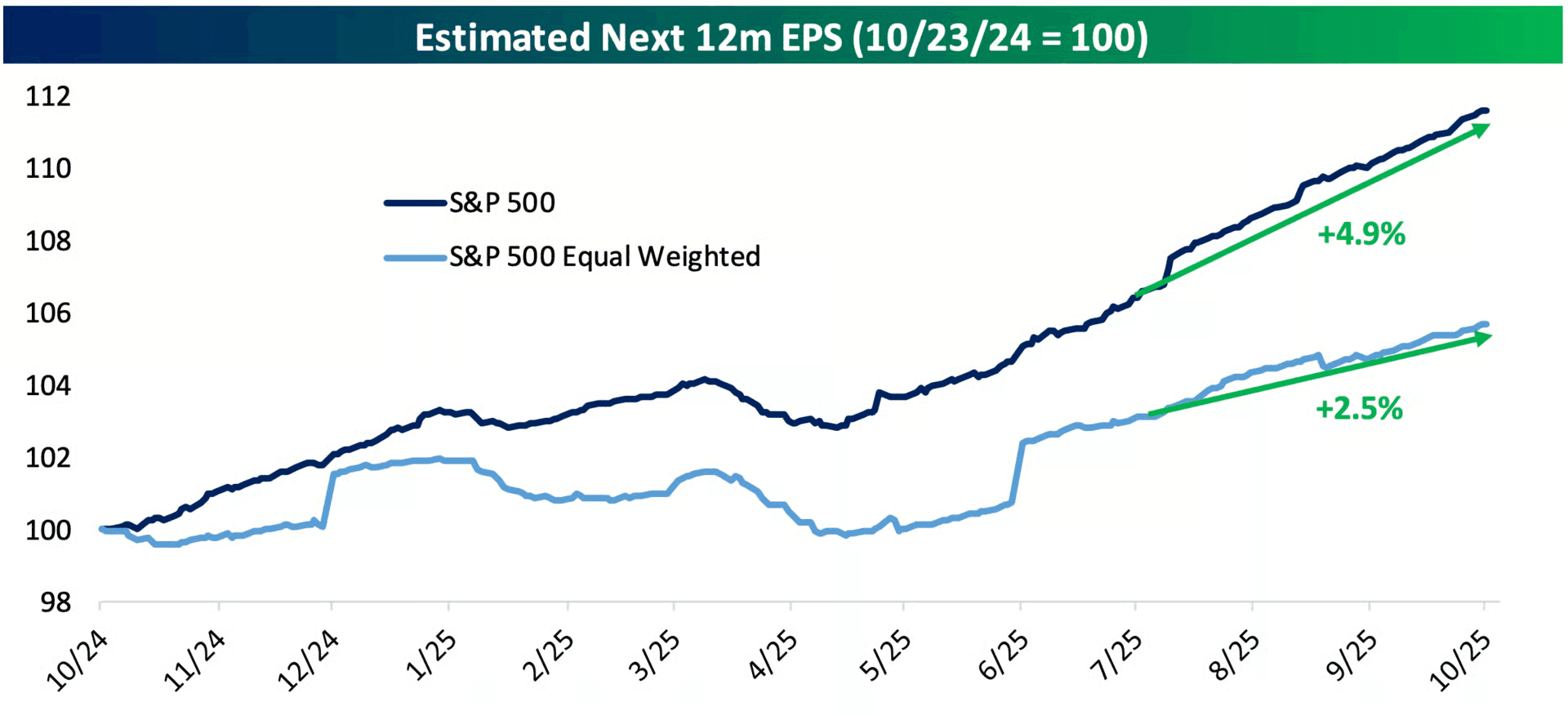

The biggest driver continues to be earnings.

Companies are generally reporting better numbers, and analysts have been raising their estimates. The current rally is being powered by actual profit growth, not just speculation. This is the key difference between a genuine bull market and a hype-driven bubble.

Over time, earnings are the most important driver of long-term returns. Don’t let anyone try and tell you otherwise.

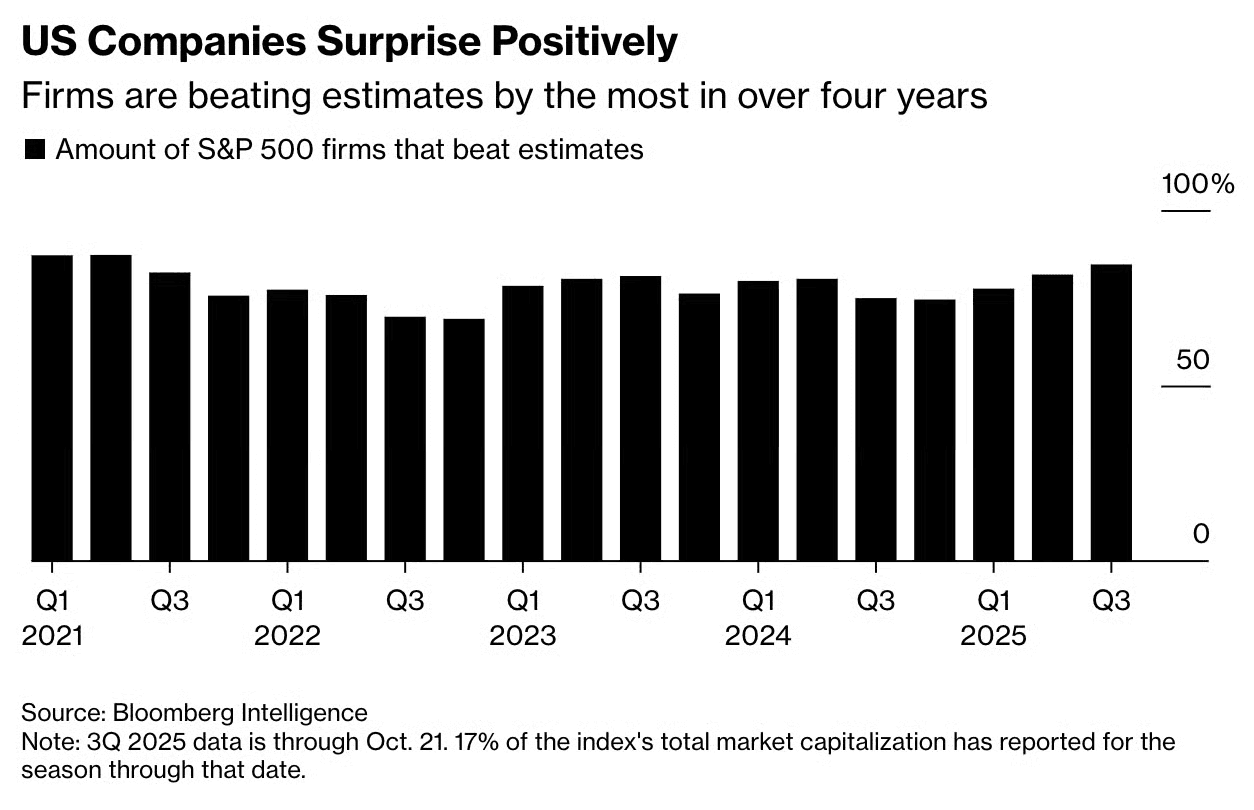

This earnings season has been especially strong. About 85% of S&P 500 companies that have reported so far have beaten expectations. This is the highest beat rate in over four years.

Profit margins are holding steady or improving, and earnings revisions are trending higher for both large-cap leaders and smaller names.

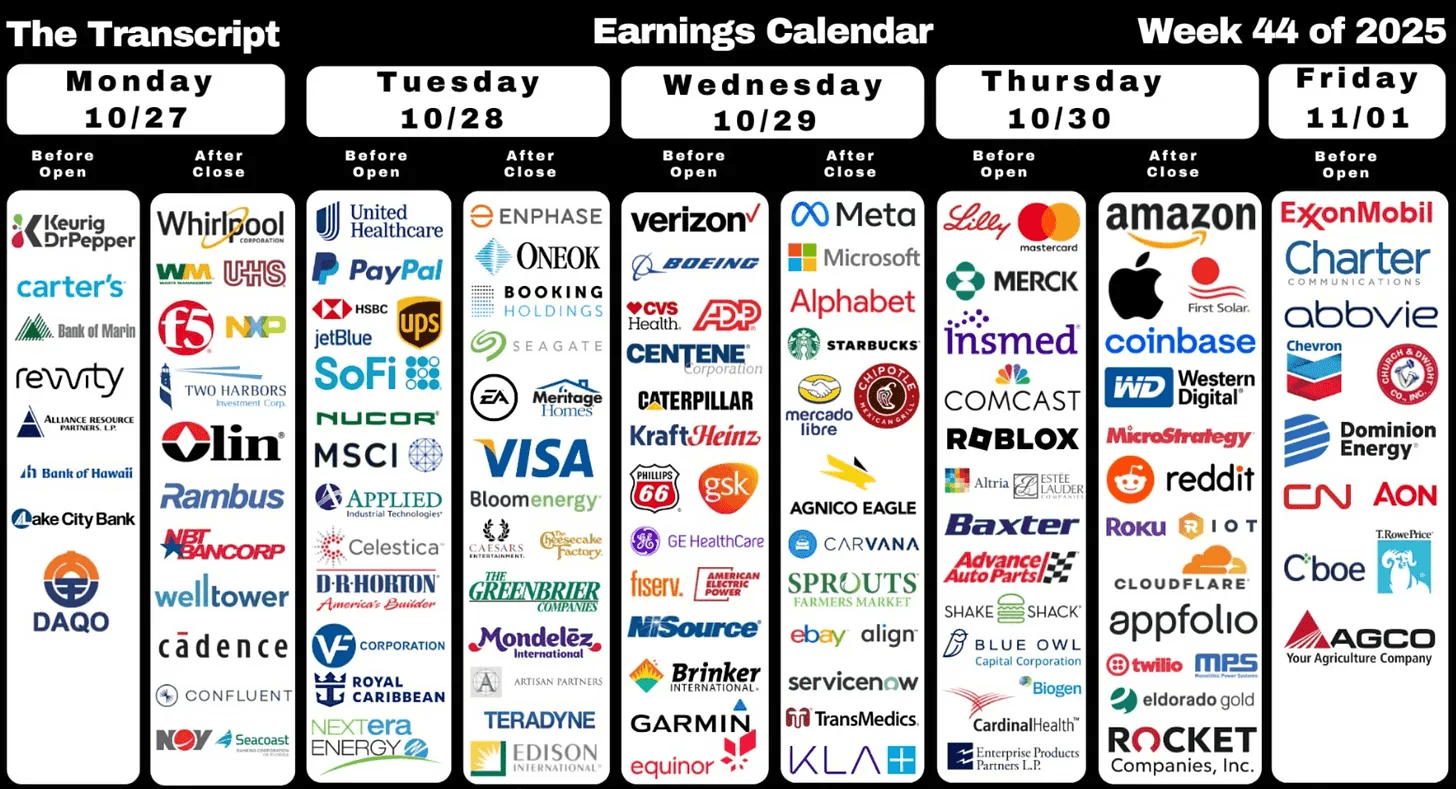

The next big catalyst is earnings from the largest tech names. Meta, Microsoft, Alphabet, Amazon, and Apple report this week. Their guidance and tone will have a major influence on how the market is going to perform in November and December.

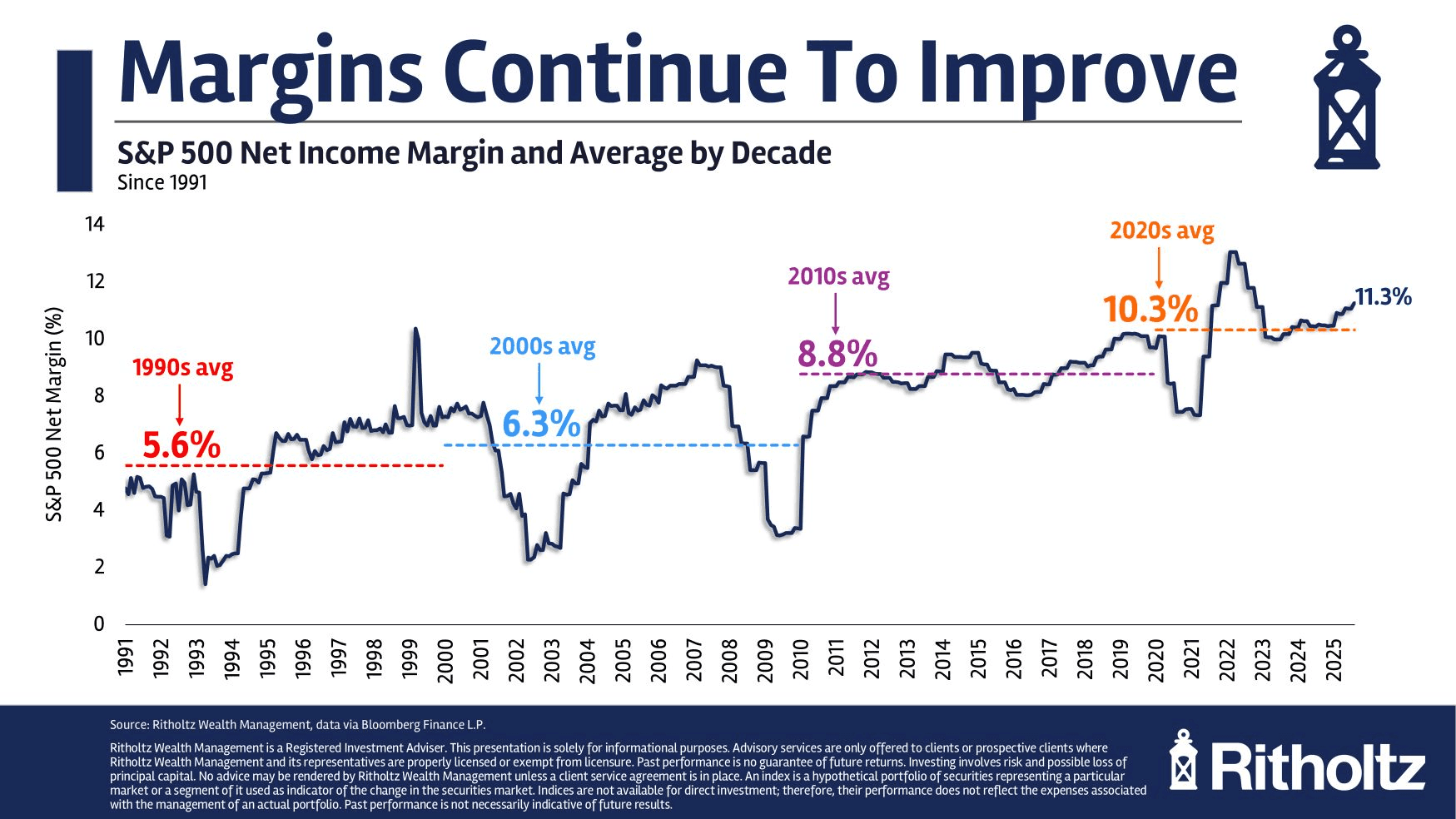

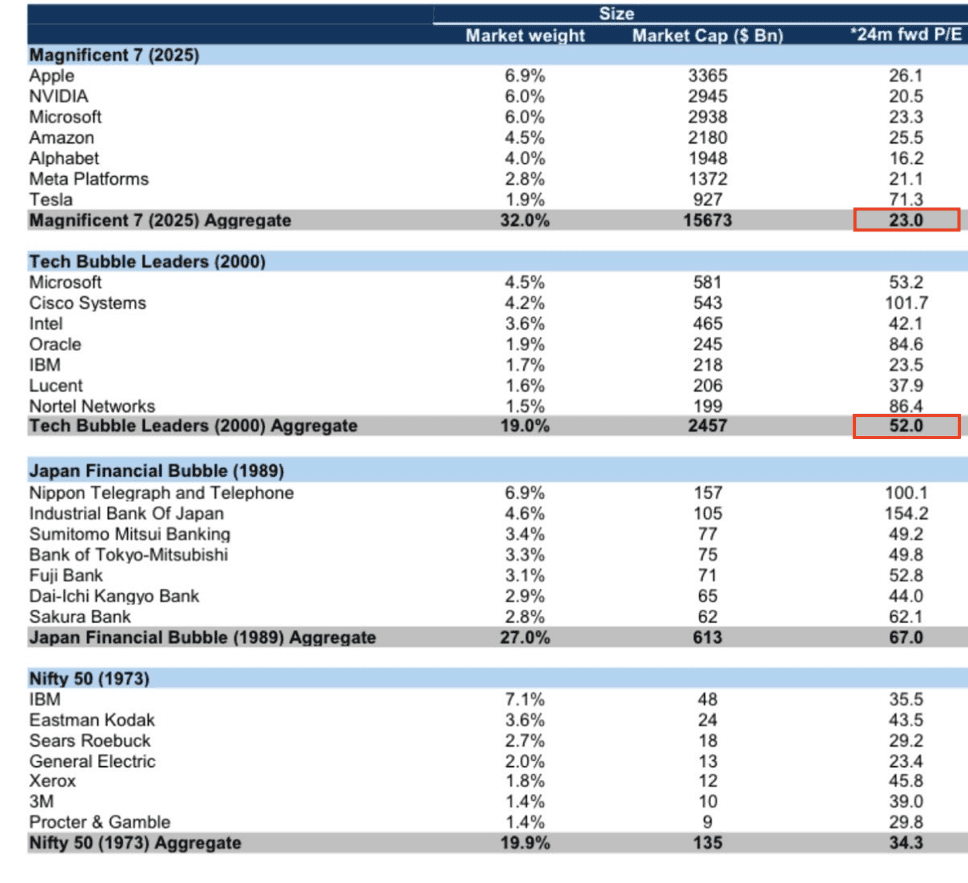

There’s been a lot of “bubble” talk lately, but it’s important to keep perspective. Real bubbles are rare and take years to form. Tech’s influence on the market today is large, but so is its role in the economy. Although some parts of the market are definitely frothy, it’s hard to call the entire bubble when the fundamentals continue to improve.

The Mag 7 aren’t expensive relative to their earnings right now (Tesla is the outlier, but that’s always been the case). Back in 2000, the biggest market leaders were trading at 50–100x earnings with far weaker balance sheets and way less predictable revenue. Today, this group trades around 23x forward earnings while generating massive free cash flow, and continuing to grow.

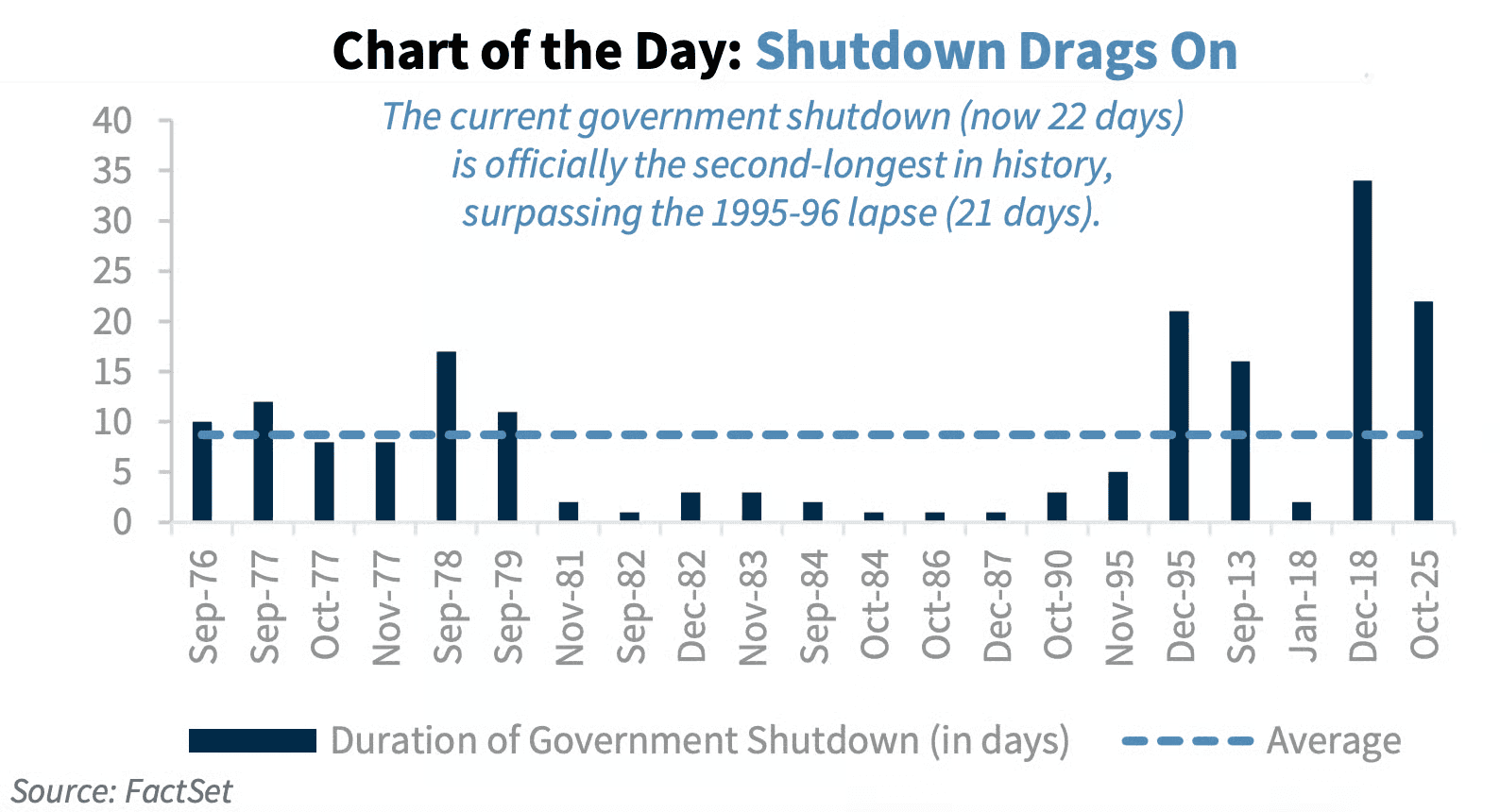

Meanwhile, the US government shutdown just became the second-longest in history. The longer it drags, the more pressure there is politically to resolve it. So, we’re getting closer we likely are to it ending.

Big picture, nothing really changed. This bull market is still alive and well.

• Rate cuts are on the horizon

• US–China trade talks are improving

• Investors are still skeptical, not euphoric

• The government shutdown likely ends soon

• Earnings continue to hold up and even accelerate

• And we’re now moving into the strongest seasonal period of the year

Previous Updates

View All

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap

- A Few Portfolio Changes