Market Opportunities

Market Opportunities

Actionable Real-Time Market Setups

Actionable Real-Time Market Setups

Lin

AAPL

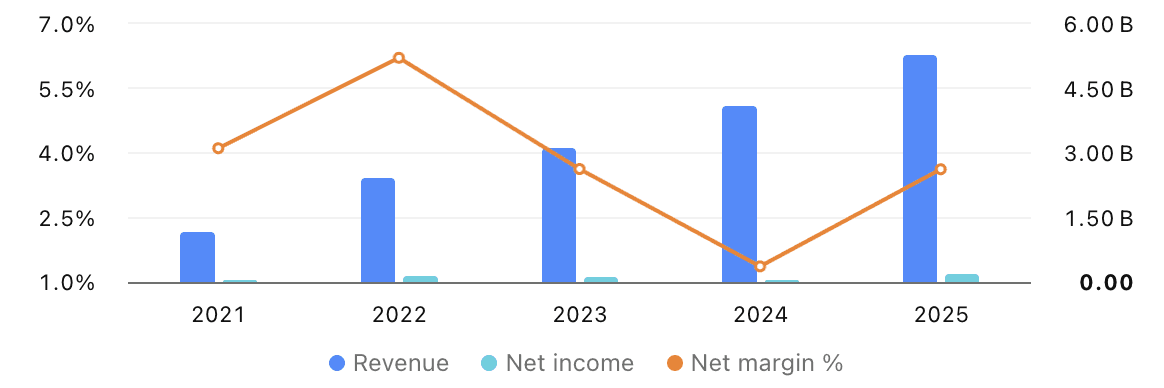

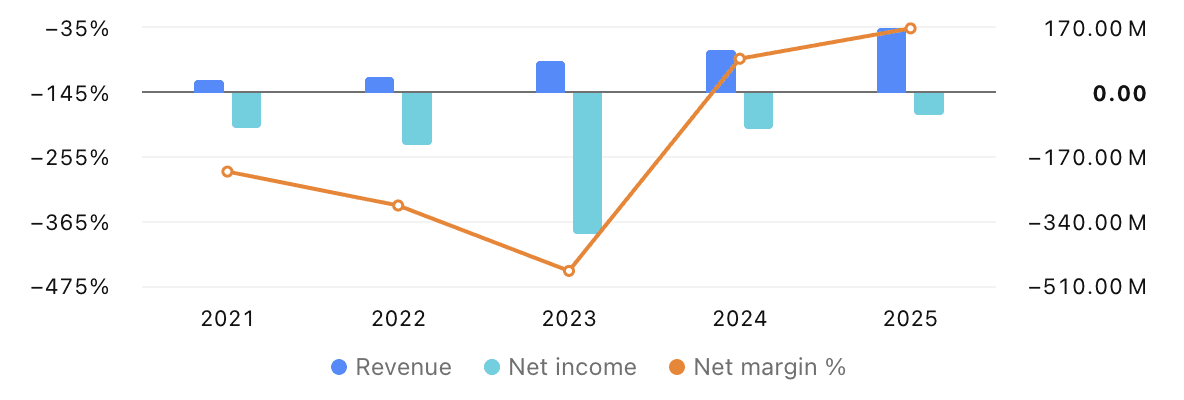

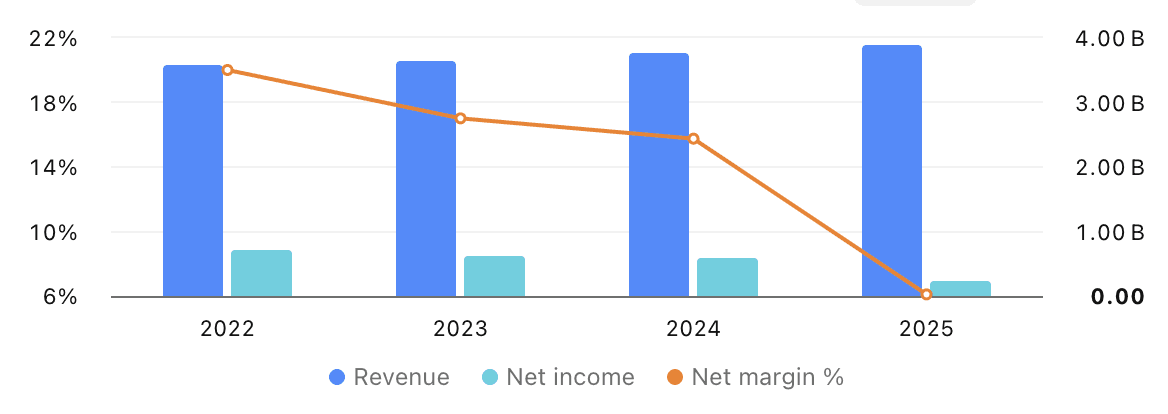

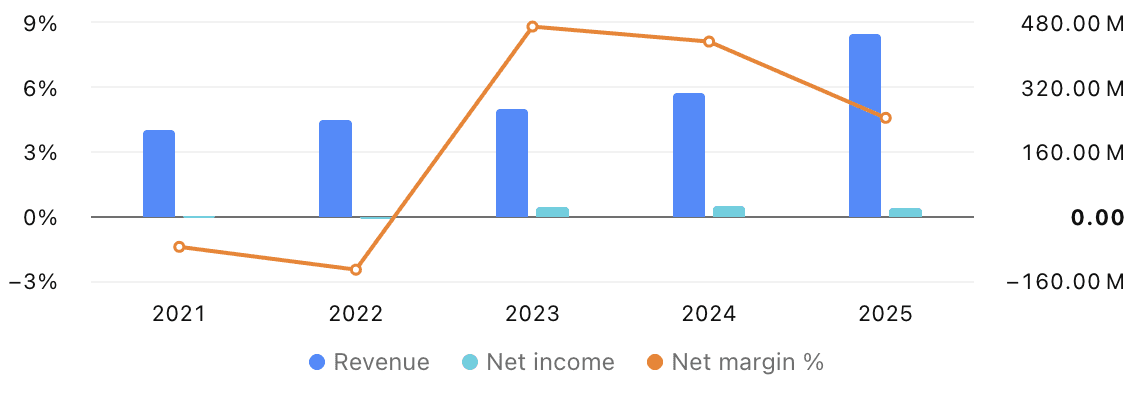

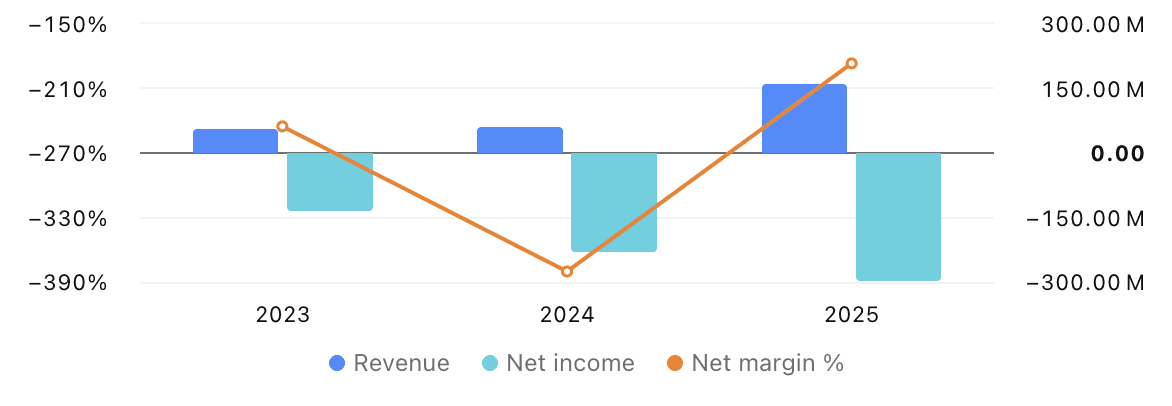

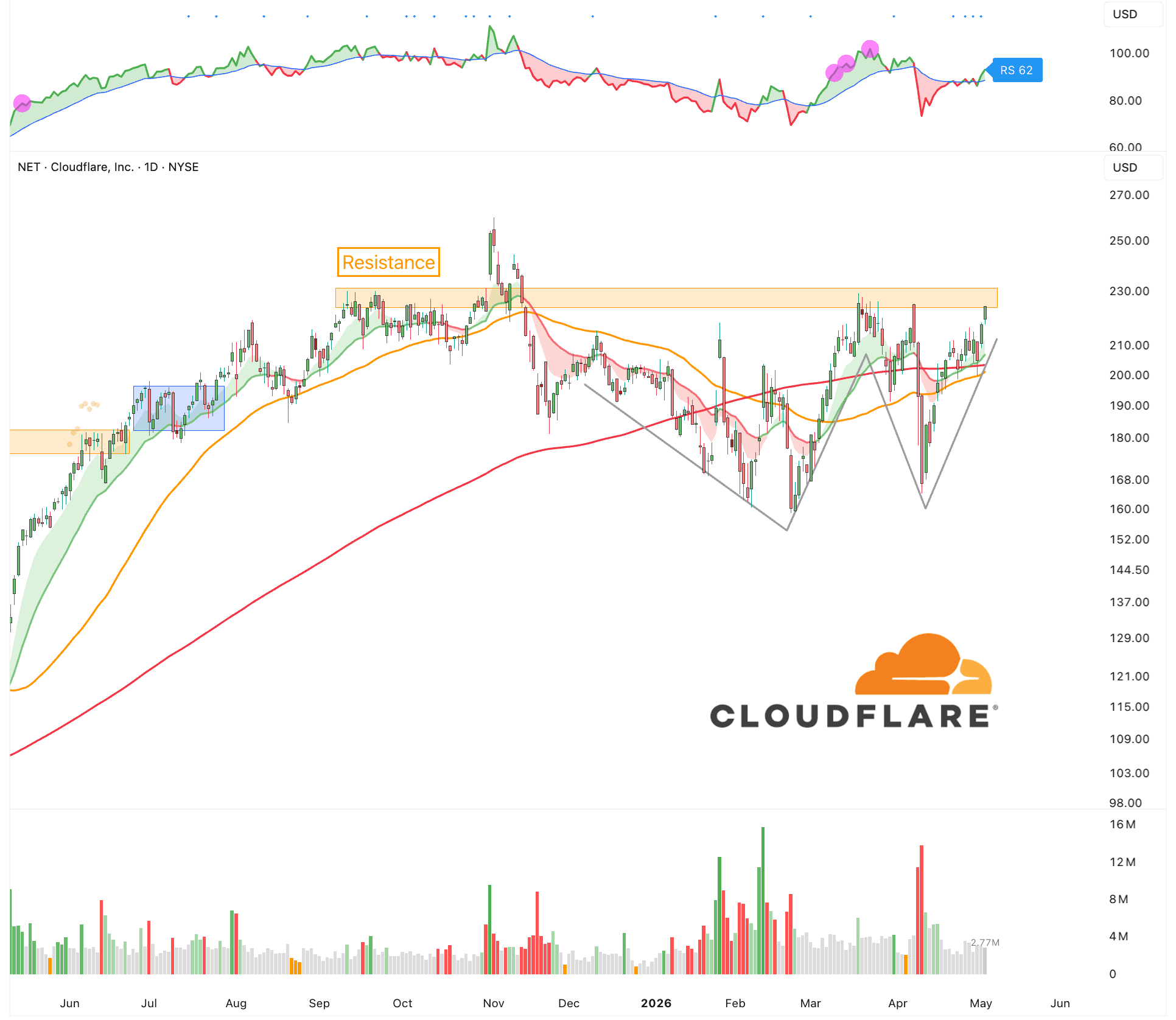

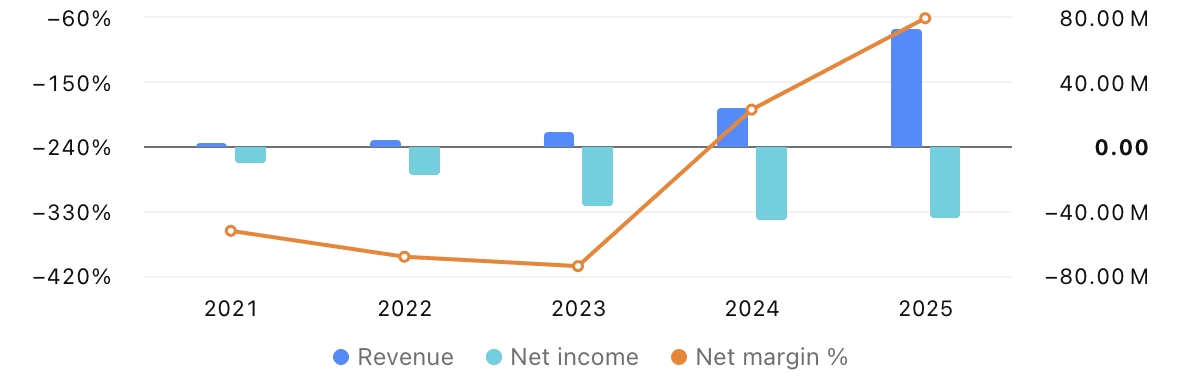

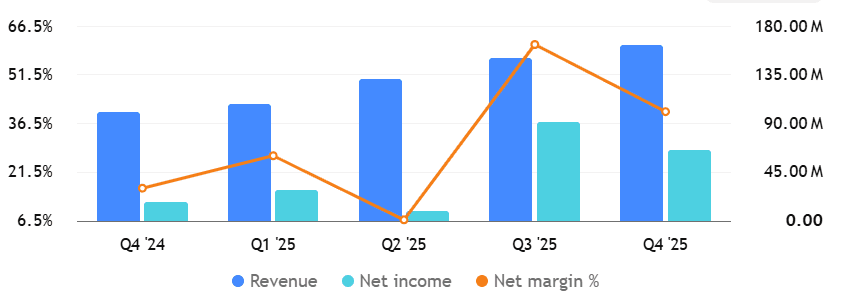

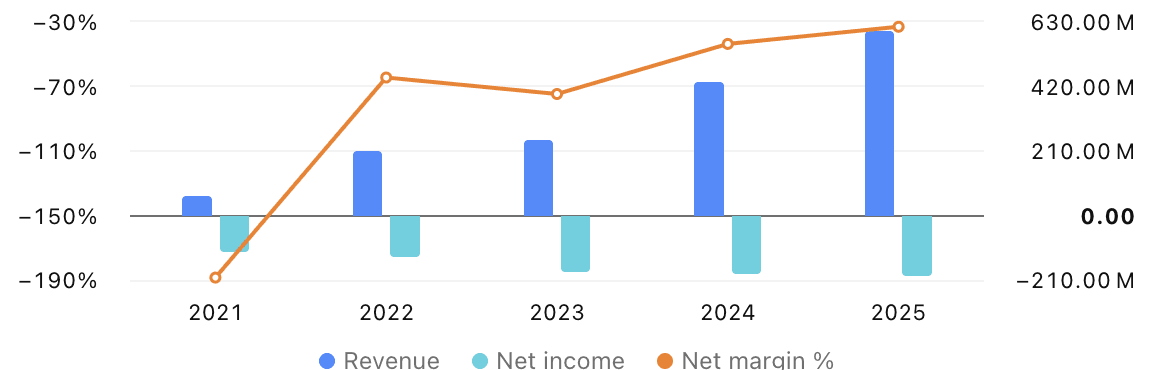

PACS Group $PACS

PACS Group $PACS

PACS Group is one of the fastest-growing public care platforms in the U.S. They operate skilled nursing facilities and assisted living facilities. Its facilities care for patients after they leave the hospital but still need nursing support, rehab, therapy, wound care, medication management, or longer clinical monitoring.

The key to its growth is a better operating model for a very difficult asset class.. PACS buys or leases skilled nursing facilities, improves how they are run, raises occupancy, improves care quality, manages staffing better, and tries to earn more profit from the same building. High occupancy is critical. A facility that is 95% full can be much more profitable than a facility that is 80% full because the extra patients use the same building and much of the same infrastructure. PACS reported 90.8% overall occupancy, compared with an industry average of around 79%.

Skilled nursing is hard to run. Many facilities are owned by smaller operators that may struggle with staffing, compliance, purchasing, reimbursement, training, technology, and quality reporting. PACS can bring stronger systems, better reimbursement knowledge, local operating discipline, and scale benefits.

They now operate 323 healthcare facilities across 17 U.S. states, with 32,757 skilled nursing beds and 2,759 assisted living beds.

PACS makes money mainly from Medicare, Medicaid, managed care insurers, and private-pay patients. These payers have different margin profiles. Medicare and higher-acuity short-stay patients are usually more attractive than long-stay Medicaid patients, while managed care depends heavily on contract terms, authorization rules, denial behavior, and length of stay.

The company has been growing quickly. In FY 2025, PACS reported $5.29B of revenue, up 29.3% year over year, with $191.5M of net income and $505M of adjusted EBITDA. In Q1 2026, revenue was $1.42B, net income was $80.7M, adjusted EBITDA was $170.4M.

After a huge move in November, it spent 7 months building a base. And is starting breakout to new all-time highs as the market continues to rotate into new sectors.

Lin

AAPL

Vishay Precision Group $VPG

Vishay Precision Group $VPG

Vishay Precision Group is a precision measurement company. It builds sensors and measurement systems that help machines understand the physical world through force, weight, pressure, stress, torque, and movement.

Thus becomes extremely important as machines become more advanced. A robot needs to know how hard it is gripping an object. A factory machine needs to know whether a part is under too much stress. A medical device needs to measure force with extreme accuracy. These are all areas where physical measurement becomes critical.

VPG operates through 3 main segments: Sensors, Weighing Solutions, and Measurement Systems. Across these segments, the company makes products such as strain gages, force sensors, load cells, precision resistors, weighing modules, and measurement systems. These components turn physical changes into electrical signals. That signal becomes data, and that data allows a machine to understand what is happening in the real world.

This is especially important in robotics. Vision can show a robot what an object looks like, but force sensing tells the robot what happens when it touches that object. Both are absolutely critical. A simple robot arm can follow a fixed path, but a more advanced robot arm needs to feel contact, measure pressure, detect slipping, and recognize when force is too high before it damages the object, the machine, or the person nearby.

The business has been stagnant for a few years. But they are finally starting to reaccelerate again. In Q1 2026, VPG reported revenue of $84.4 million, up 17.6% year over year. Orders reached $102.1 million, creating a book-to-bill ratio of 1.21, which means new orders were coming in faster than the company was converting them into revenue.

The Sensors segment was especially strong. Revenue in that segment grew 23.1% year over year in Q1 2026, helped by better demand in precision resistors, robotics, aerospace, military, and space.

Humanoid robotics is still a very early opportunity for VPG. The company reported about $1 million of humanoid orders in Q1 2026. That is still small compared with total revenue. There is still a long way to go. But if robotics takes off, VPG’s business will definitely benefit.

Lin

AAPL

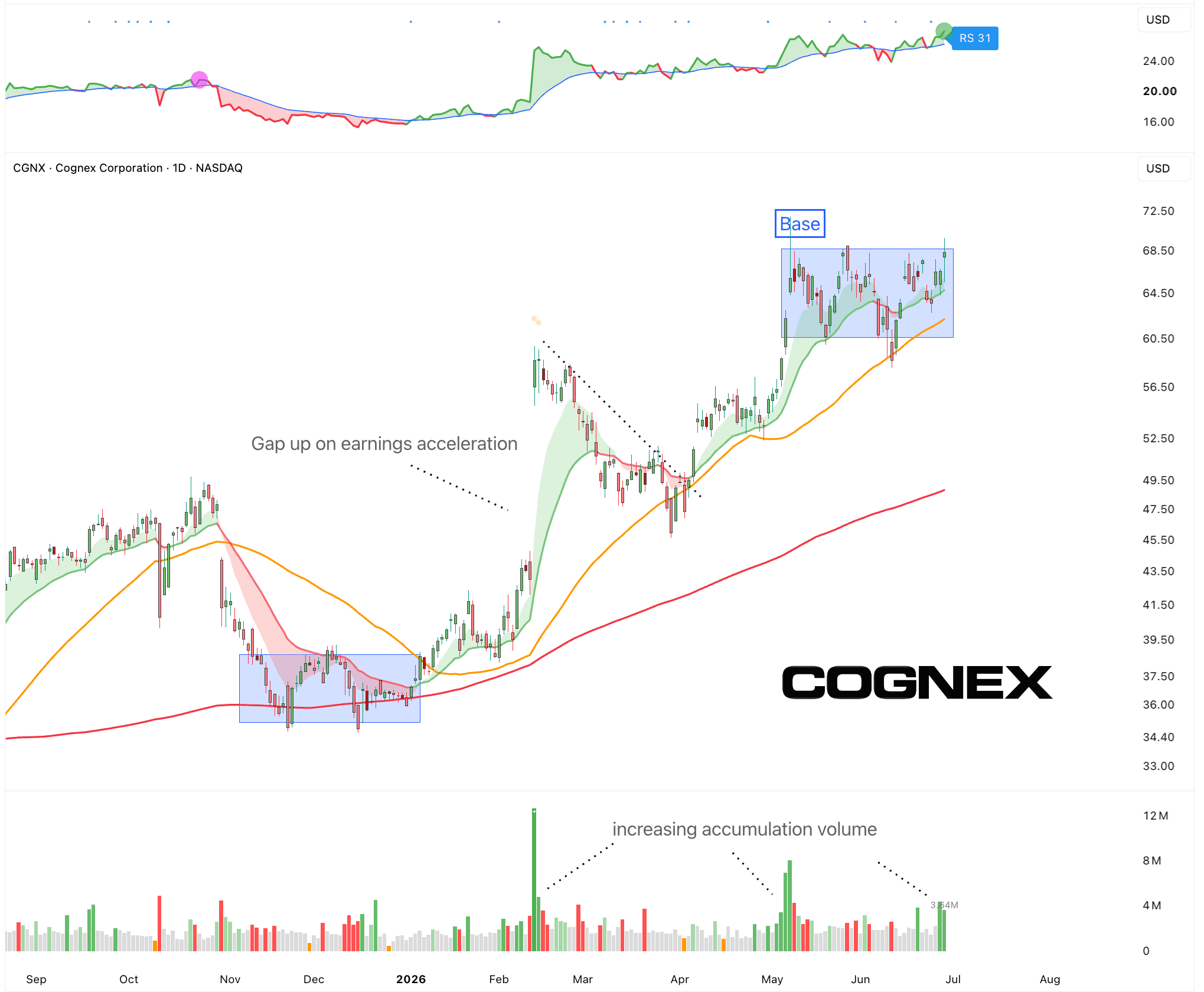

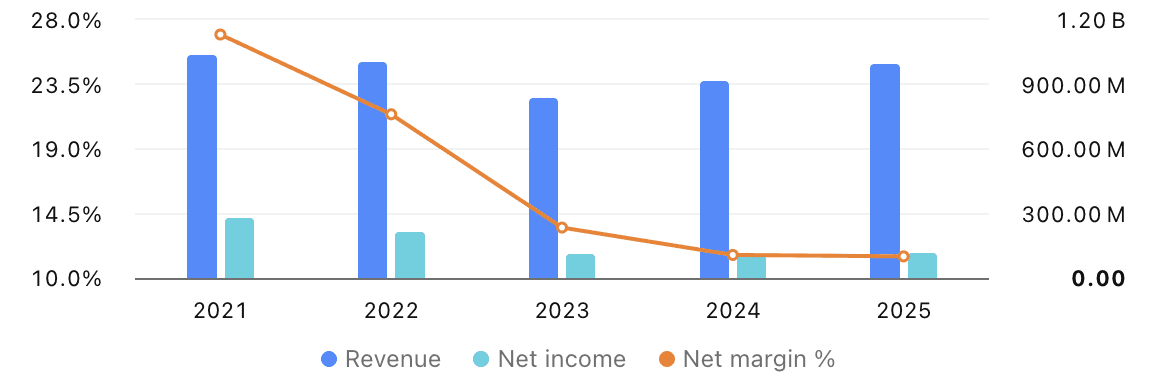

Cognex $CGNX

Cognex $CGNX

Cognex builds machine vision systems, sensors, and software that allow factories, warehouses, robots, and production lines to operate in the physical world.

Its products are used across factory automation, logistics, consumer electronics, packaging, automotive, semiconductors, medical lab automation, and other industrial end markets. It already serves more than 30,000 customers in over 30 countries.

Now, AI is the catalyst for robotics and machines. AI is changing what machine vision can do. Traditional vision systems were powerful, but often hard to deploy. They needed controlled lighting, expert setup, and a lot of tuning. AI-powered vision systems can handle more complex, messy, real-world environments. That makes the technology easier to use and opens more use cases.

Cognex wants to become the top provider of AI-powered machine vision. New products like OneVision, DataMan 290, and SLX are designed to make vision systems easier to deploy and more scalable.

After a few years of declining revenues, 2025 was a turning point. Revenue returned to growth, adjusted EPS grew 38%, and management began cutting low-growth, low-margin revenue from the portfolio. Q1 2026 showed a clear inflection. Revenue grew 24% year over year to $268M, gross margin improved to 71.1%, operating margin reached 22.3%, and adjusted EPS more than doubled to $0.34. The company also guided Q2 2026 revenue to $280M to $300M.

It’s been building consolidating for two months now. And the recent market pullback barely left a dent. There’s also increasing investor interest in robotics with since the humanoid maker Agility Robotics is going public via a SPAC merger $CCXI under the ticker $AGLT from which companies the entire sector should benefit. Companies like AEVA and Ouster, which were highlighted recently, are back in focus.

My believe is that Physical AI and robotics will be one of the biggest beneficiaries of this tech boom.

Lin

AAPL

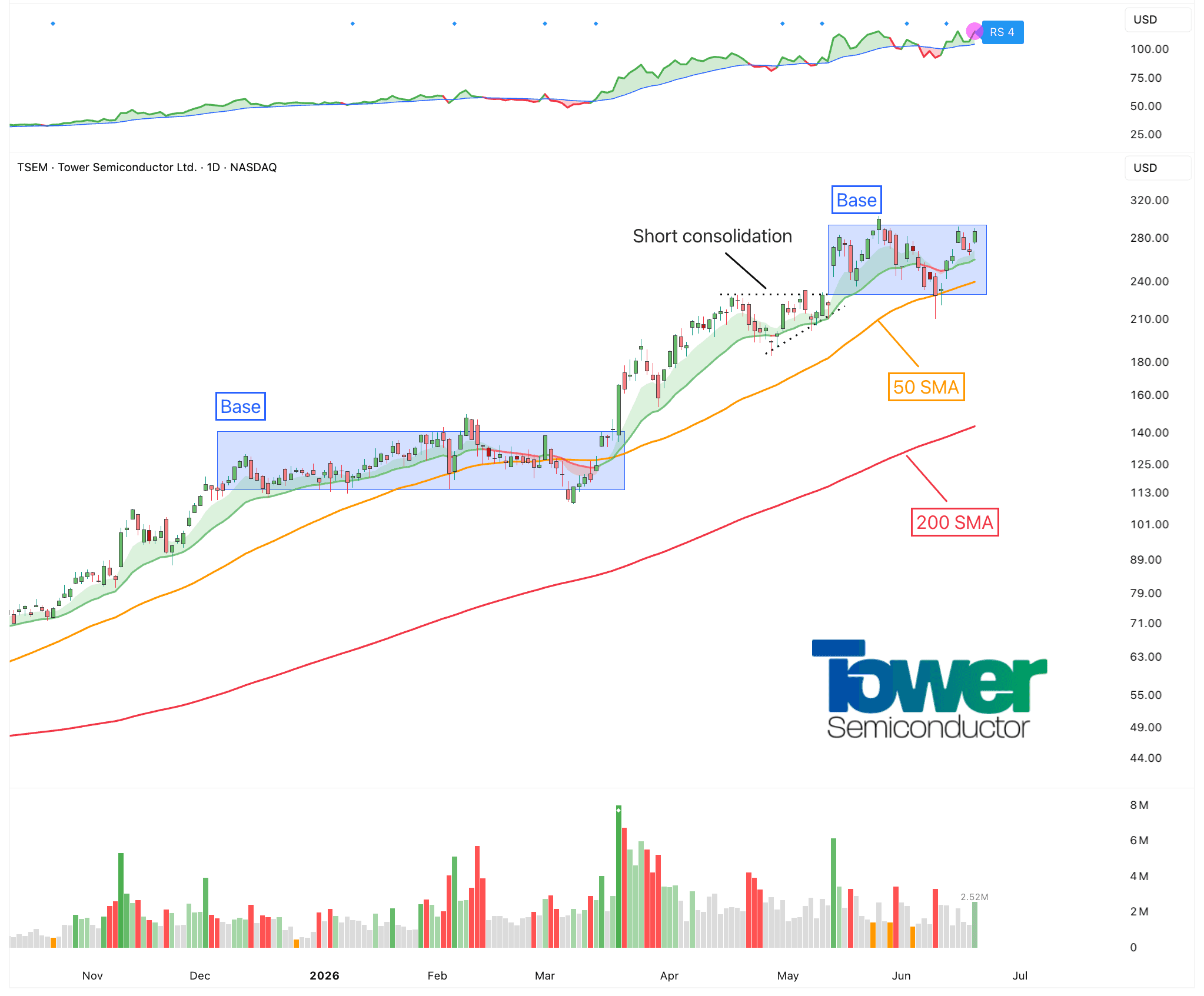

Tower Semiconductor $TSEM

Tower Semiconductor $TSEM

Tower Semiconductor is a specialty foundry.

It manufactures chips for other companies, but it does not compete directly with TSMC at the most advanced logic nodes. Tower focuses on high-value specialty processes like silicon photonics, silicon germanium, RF, analog, power management, image sensors, and mixed-signal chips.

The most important part is silicon photonics.

AI data centers need to move huge amounts of data between GPUs, switches, racks, and data centers. Every training run needs constant communication between GPUs, memory, switches, racks, and storage. The bigger the AI model gets, the more important the network becomes.

Inside a normal data center, data often moves through copper wires and electrical signals. Copper works well over short distances, but it becomes less efficient as speeds rise. At very high bandwidth, copper creates more signal loss, more heat, more power consumption, and more complexity. That’s why current copper cables struggle as bandwidth and power demands rise (read more on optical AI infrastructure chain in the Photonics theme). Optical connections solve part of that problem by moving data with light and Tower Semiconductors manufactures the photonic chips that make this possible.

Its Q1 2026 earnings result was decent.

Revenue was $414 million, up 15% year over year. Gross profit was $111 million, up 52%. Operating profit was $65 million, up 96%. Net profit was $65 million, up from $40 million last year. The company guided Q2 revenue to a record $455 million, up 22% year over year and 10% sequentially.

The numbers weren’t mind-blowing. There are definitely faster growing companies. But the most important number was not revenue.

It was the silicon photonics contract book.

TSEM signed customer contracts for $1.3 billion of silicon photonics revenue for 2027. Customers also paid $290 million in prepayments to reserve capacity. That is an incredibly strong signal. Customers do not pay upfront unless they really really need the capacity.

That’s why it is expanding aggressively. It is investing heavily in silicon photonics and silicon germanium capacity, with total planned investment around $920 million.

Right now, it’s building another base and setting up a potential breakout to new all-time highs.

Lin

AAPL

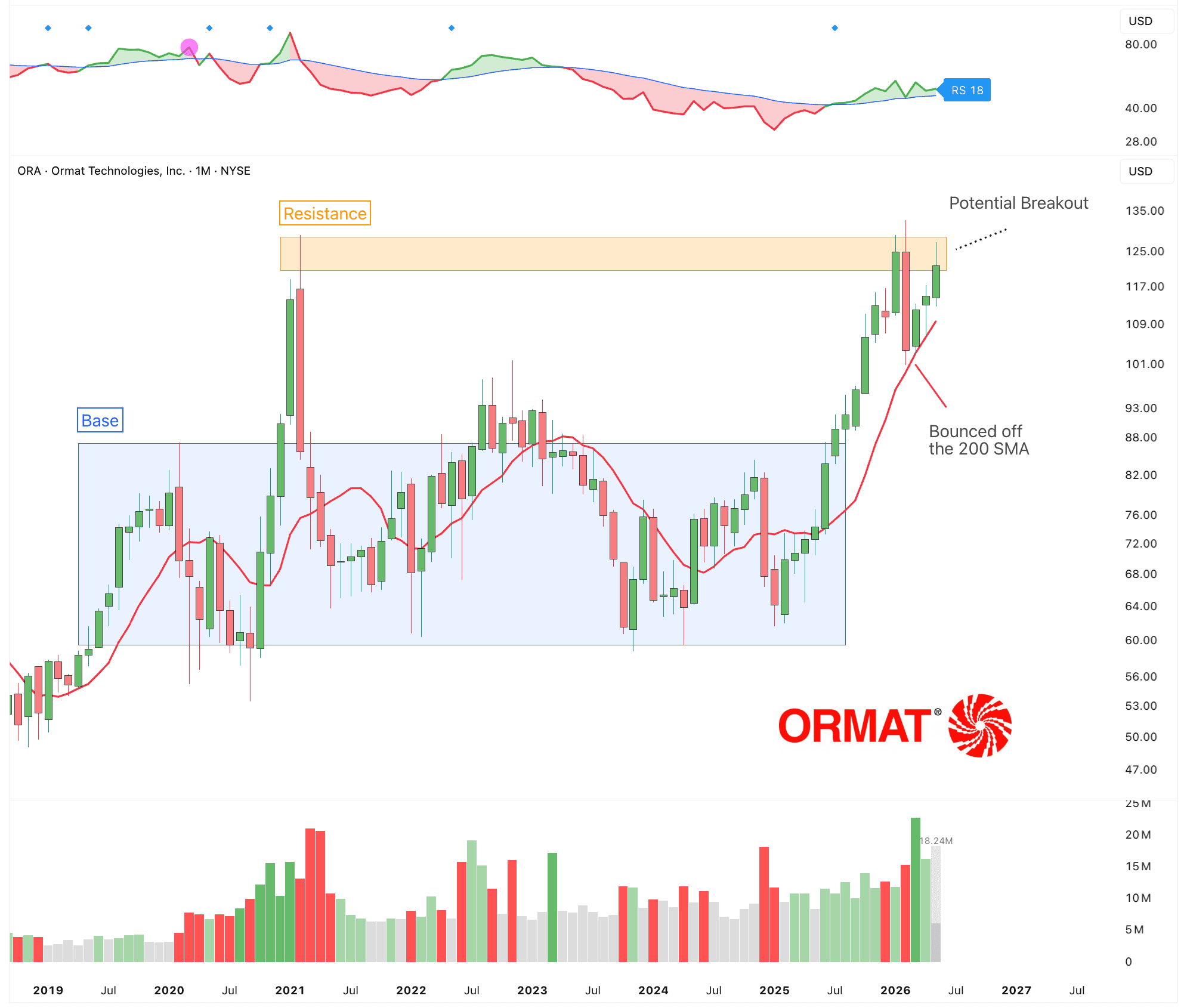

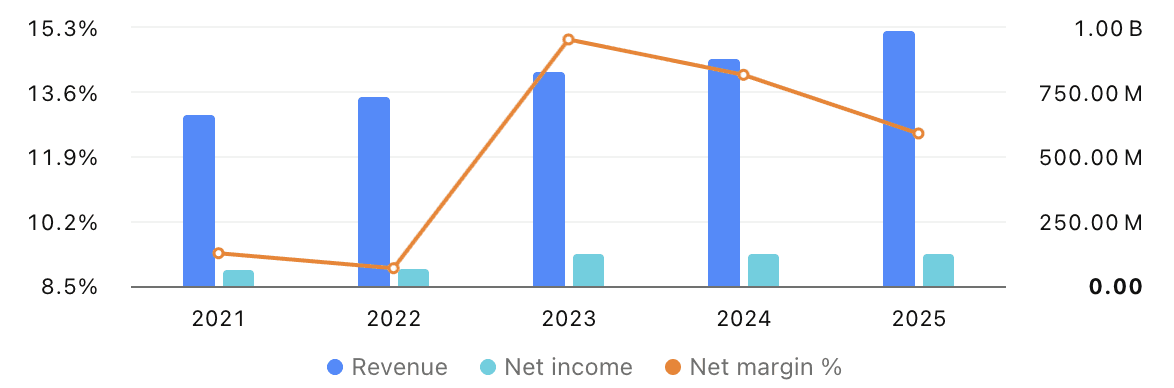

Sterling Infrastructure $STRL

Sterling Infrastructure $STRL

Tower Semiconductor is a specialty foundry.

It manufactures chips for other companies, but it does not compete directly with TSMC at the most advanced logic nodes. Tower focuses on high-value specialty processes like silicon photonics, silicon germanium, RF, analog, power management, image sensors, and mixed-signal chips.

The most important part is silicon photonics.

AI data centers need to move huge amounts of data between GPUs, switches, racks, and data centers. Every training run needs constant communication between GPUs, memory, switches, racks, and storage. The bigger the AI model gets, the more important the network becomes.

Inside a normal data center, data often moves through copper wires and electrical signals. Copper works well over short distances, but it becomes less efficient as speeds rise. At very high bandwidth, copper creates more signal loss, more heat, more power consumption, and more complexity. That’s why current copper cables struggle as bandwidth and power demands rise (read more on optical AI infrastructure chain in the Photonics theme). Optical connections solve part of that problem by moving data with light and Tower Semiconductors manufactures the photonic chips that make this possible.

Its Q1 2026 earnings result was decent.

Revenue was $414 million, up 15% year over year. Gross profit was $111 million, up 52%. Operating profit was $65 million, up 96%. Net profit was $65 million, up from $40 million last year. The company guided Q2 revenue to a record $455 million, up 22% year over year and 10% sequentially.

The numbers weren’t mind-blowing. There are definitely faster growing companies. But the most important number was not revenue.

It was the silicon photonics contract book.

TSEM signed customer contracts for $1.3 billion of silicon photonics revenue for 2027. Customers also paid $290 million in prepayments to reserve capacity. That is an incredibly strong signal. Customers do not pay upfront unless they really really need the capacity.

That’s why it is expanding aggressively. It is investing heavily in silicon photonics and silicon germanium capacity, with total planned investment around $920 million.

Right now, it’s building another base and setting up a potential breakout to new all-time highs.

Lin

AAPL

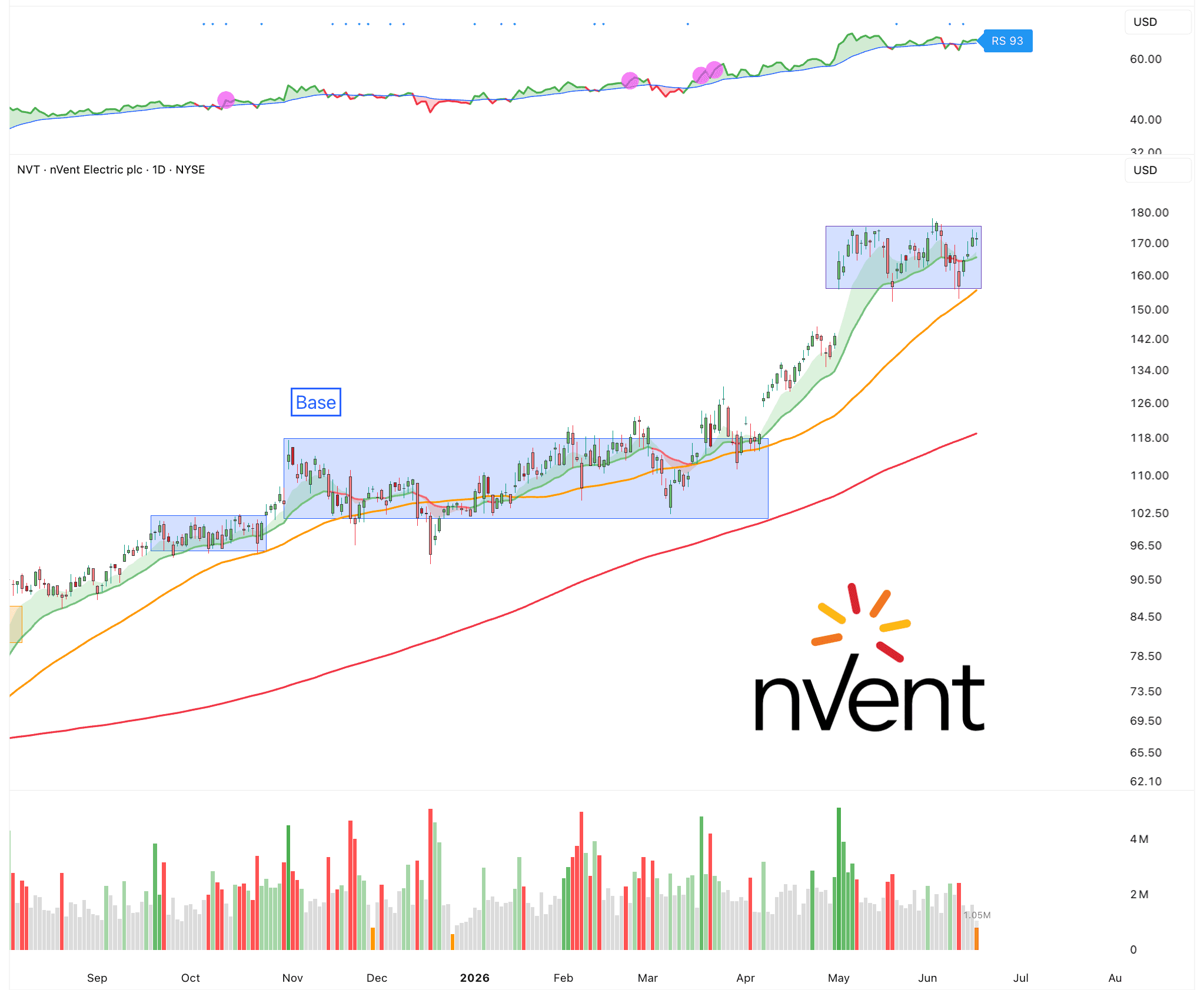

nVent Electric $NVT

nVent Electric $NVT

AI needs physical infrastructure. Chips are critical, but chips alone are not enough. AI computer requires power, racks, cooling, enclosures, and protection.

nVent makes electrical connection and protection products that sit inside mission-critical infrastructure. That includes enclosures, racks, power connections, fastening systems, liquid cooling infrastructure, modular electrical buildings, and protection solutions for data centers, utilities, industrial facilities, and commercial buildings.

AI workloads require dense compute clusters. Dense compute creates more heat, more electrical load, and more complexity inside the data center. That creates demand for liquid cooling, racks, enclosures, power distribution, and protection systems. nVent sells into all of that. It help customers connect, protect, cool, and manage electrical systems safely.

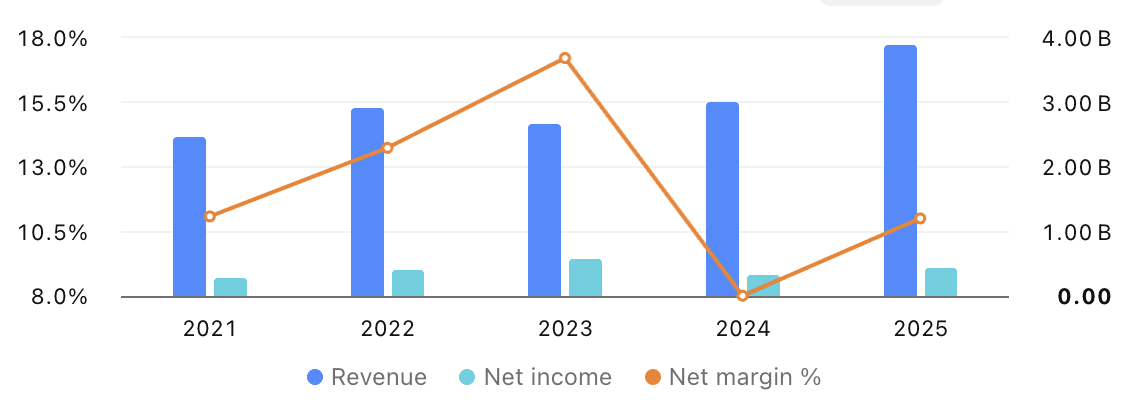

It’s Q1 2026 earnings result was very strong.

Revenue was $1.2 billion, up 53% year over year. Organic growth was 34%. Adjusted EPS was $1.09, up 63%. Adjusted operating margin stayed at 20%. The standout segment was Systems Protection. Sales grew 76%, with 50% organic growth. Segment income grew 95%, and margin expanded to 22.7%.

But The most important number was backlog: $2.6 billion. Data center demand is clearly propelling demand for the company to new heights.

And right now it’s been building a textbook base and setting up for a breakout.

Lin

AAPL

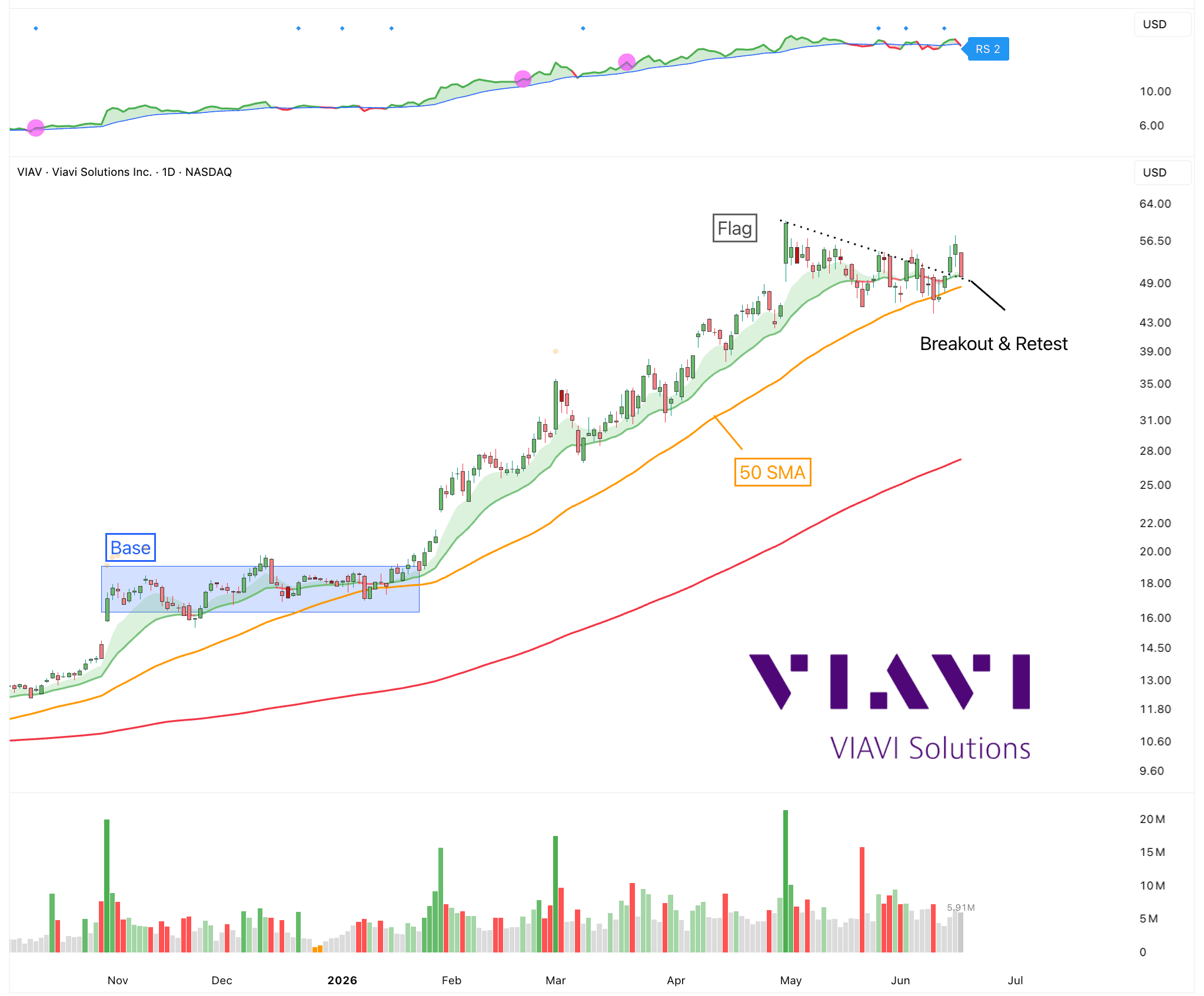

Viavi Solutions $VIAV

Viavi Solutions $VIAV

AI needs physical infrastructure. Chips are critical, but chips alone are not enough. AI computer requires power, racks, cooling, enclosures, and protection.

nVent makes electrical connection and protection products that sit inside mission-critical infrastructure. That includes enclosures, racks, power connections, fastening systems, liquid cooling infrastructure, modular electrical buildings, and protection solutions for data centers, utilities, industrial facilities, and commercial buildings.

AI workloads require dense compute clusters. Dense compute creates more heat, more electrical load, and more complexity inside the data center. That creates demand for liquid cooling, racks, enclosures, power distribution, and protection systems. nVent sells into all of that. It help customers connect, protect, cool, and manage electrical systems safely.

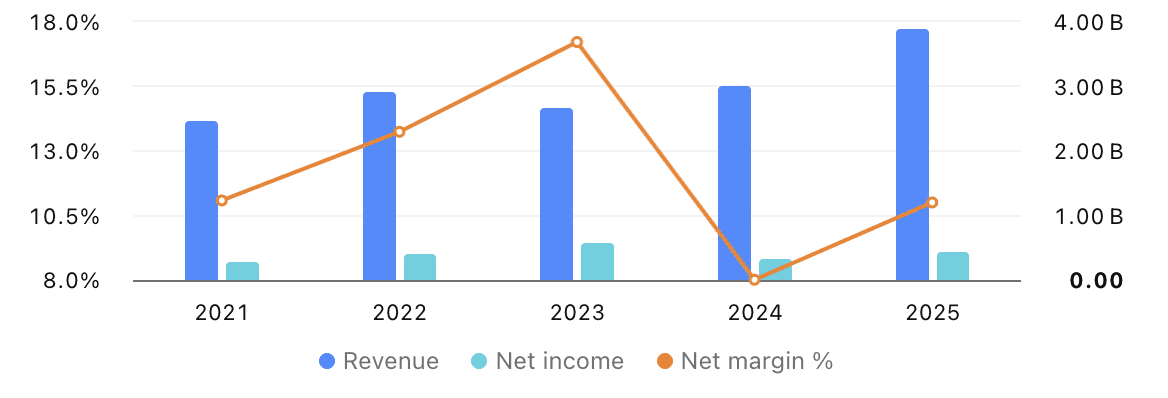

It’s Q1 2026 earnings result was very strong.

Revenue was $1.2 billion, up 53% year over year. Organic growth was 34%. Adjusted EPS was $1.09, up 63%. Adjusted operating margin stayed at 20%. The standout segment was Systems Protection. Sales grew 76%, with 50% organic growth. Segment income grew 95%, and margin expanded to 22.7%.

But The most important number was backlog: $2.6 billion. Data center demand is clearly propelling demand for the company to new heights.

And right now it’s been building a textbook base and setting up for a breakout.

Lin

AAPL

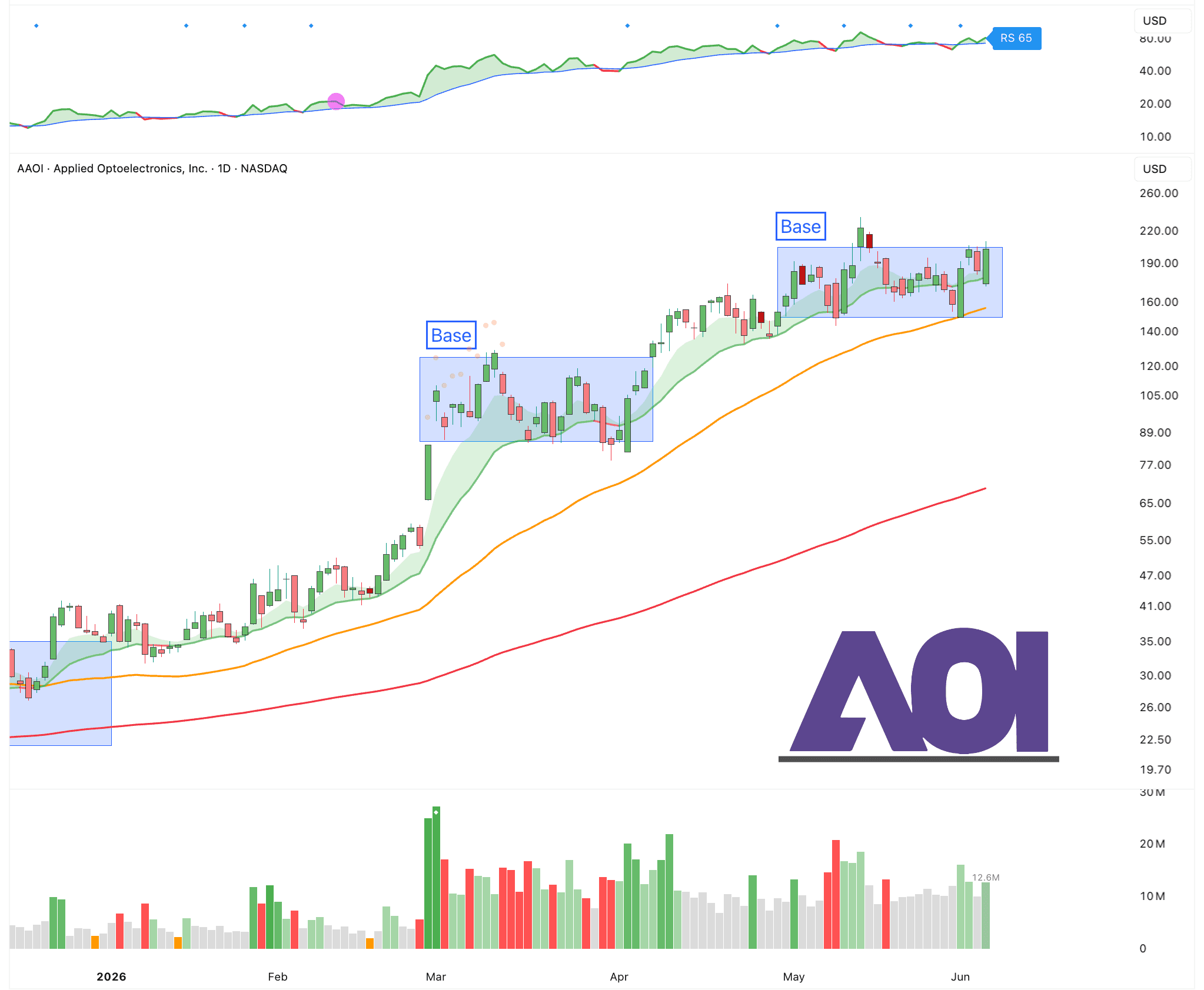

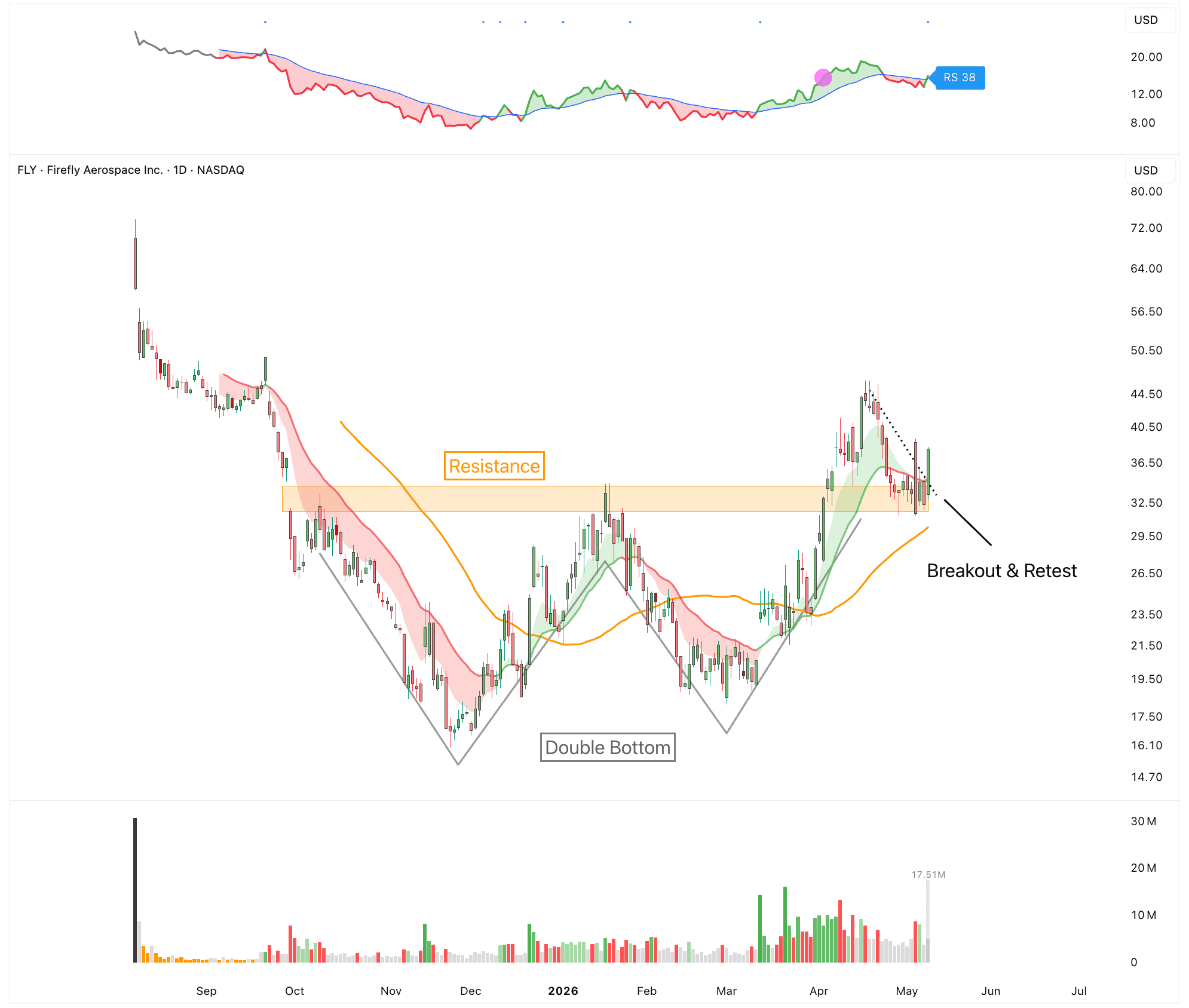

Applied Optoelectronics $AAOI

Applied Optoelectronics $AAOI

Applied Optoelectronics $AAOI is one of the more interesting picks-and-shovels names in the AI infrastructure trade.

Every new AI data center needs more GPUs, more power, more cooling, and much faster connections between servers. The larger the clusters get, the more important optical networking becomes. As AI models get bigger and training clusters scale, the amount of data moving through the network explodes. That makes optical networking less of a boring hardware category and more of a core AI infrastructure layer.

Applied Optoelectronics makes optical transceivers, laser components, and networking products used in AI data centers, cable networks, telecom, and fiber access. AI workloads are forcing hyperscalers to upgrade their networks faster, and AAOI is becoming one of the suppliers tied directly to that upgrade cycle. The key product cycle is 800G, with 1.6T coming after that. These are high-speed optical transceivers that help move massive amounts of data inside and between data centers.

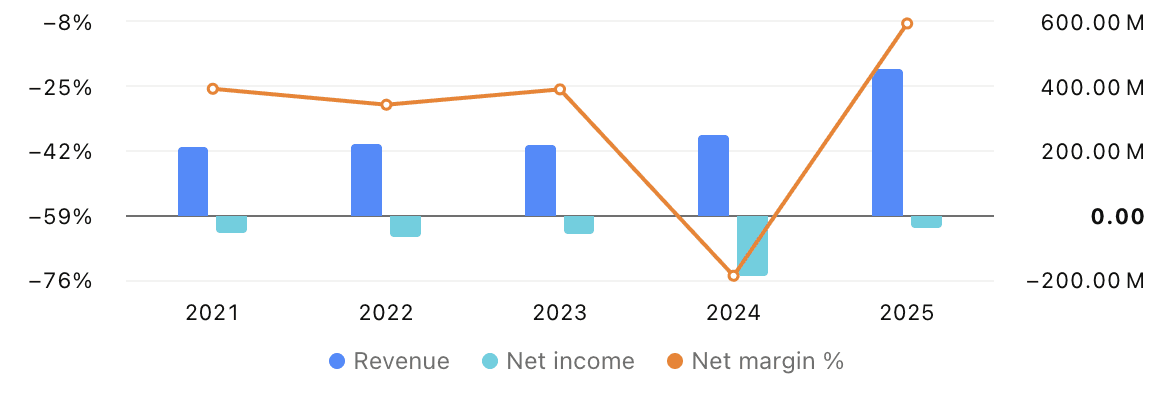

The numbers are starting to show that shift. In Q1 2026, AAOI reported record revenue of about $151 million, up from about $100 million in the prior year period. Data center revenue was about $81 million, making it the largest segment in the quarter.

The most important part of the earnings story was the ramp. Management said it completed the first volume shipment of 800G products to a large hyperscale customer in Q1 and expects a stronger volume ramp starting in Q2. They also guided for Q2 revenue of $180 million to $198 million, which implies another step up from Q1. Even more important, management expects sequential growth through the year, with bigger growth starting in Q3 as more capacity comes online.

This is not a small company selling into weak end markets. It is selling into the biggest AI infrastructure buyers in the world. The company has received new 800G orders from major hyperscale customers, including a $71 million order announced in April 2026. These customers demand quality, volume, reliability, and price. So, this is a meaningful validation point.

It is not the safest way to play AI, but it may be one of the most direct ways to play the optical networking bottleneck. So far, the stock has also been holding up incredibly well and now looks like it is setting up for a potential breakout for its next leg higher.

Lin

AAPL

Digital Ocean $DOCN

Digital Ocean $DOCN

AI infrastructure demand is outrunning the physical world.

Hyperscalers and AI cloud companies need massive amounts of compute capacity. Today, the constraint has moved beyond GPUs. It is power, speed, and location. Applied Digital is building large-scale AI data center campuses in places where power is available and land is easier to develop.

The winners in this cycle will not only be the companies with the best chips or models. They will also be the companies that can supply the most compute. And for that they need to secure land, power, cooling, permitting, construction capacity, and long-term customers.

Old data center model was built around internet traffic, cloud storage, SaaS workloads, and proximity to population centers. That is no longer true for AI.

Training and inference workloads do not always need to sit next to major cities. What they need most is cheap power, available grid capacity, cooling efficiency, and the ability to deploy thousands of GPUs at scale.

In June 2025, the company announced 2 roughly 15-year lease agreements with CoreWeave for 250 MW at its Ellendale, North Dakota campus. Reuters reported that the leases were worth about $7 billion over the term.

And in its fiscal Q3 2026 update, Applied Digital said Polaris Forge 2 is a 200 MW investment-grade hyperscaler campus, while Delta Forge 1 is a 300 MW AI factory campus backed by a high investment-grade hyperscaler, with initial operations expected in mid-calendar 2027.

What’s important is that Applied Digital has moved past 1 GW of contracted capacity.

In fiscal Q3 2026, revenue was $126.6 million, up 139% year over year from $52.9 million. Revenue is starting to scale as more nad more facilities come online. Adjusted revenue, which excludes the Cloud Services business, was $108.6 million. Adjusted EBITDA was $44.1 million, compared with $6.3 million in the prior-year quarter.

Now the setup looks even more interesting. Applied Digital just broke out of a 10-month base and then came back to retest the breakout area almost perfectly.

And it’s not just Applied Digital. The whole sector is starting to lead, and that is exactly what you want to see. The best moves usually happen when the stock is not moving in isolation, but together with the entire sector - as mentioned here.

Lin

AAPL

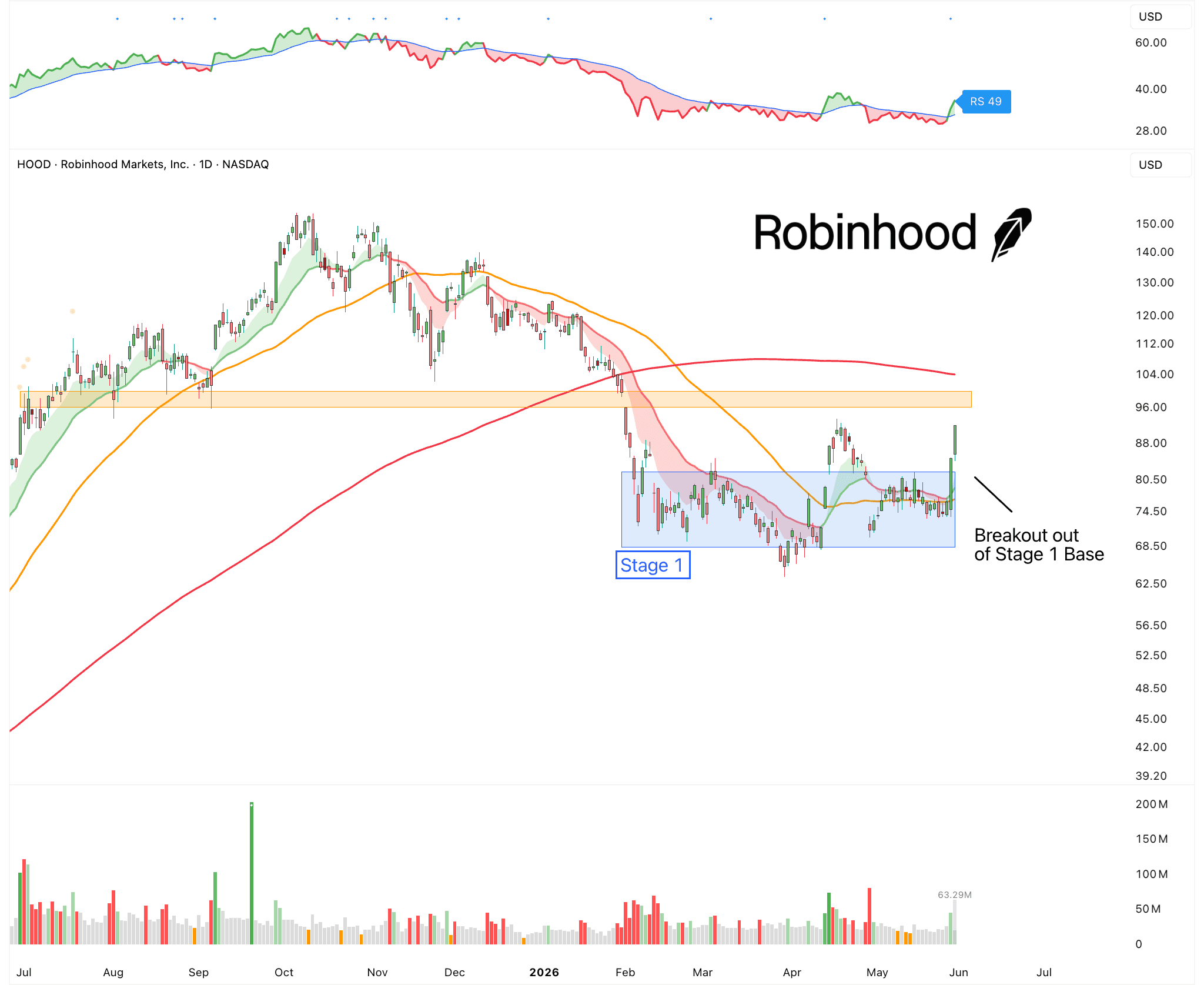

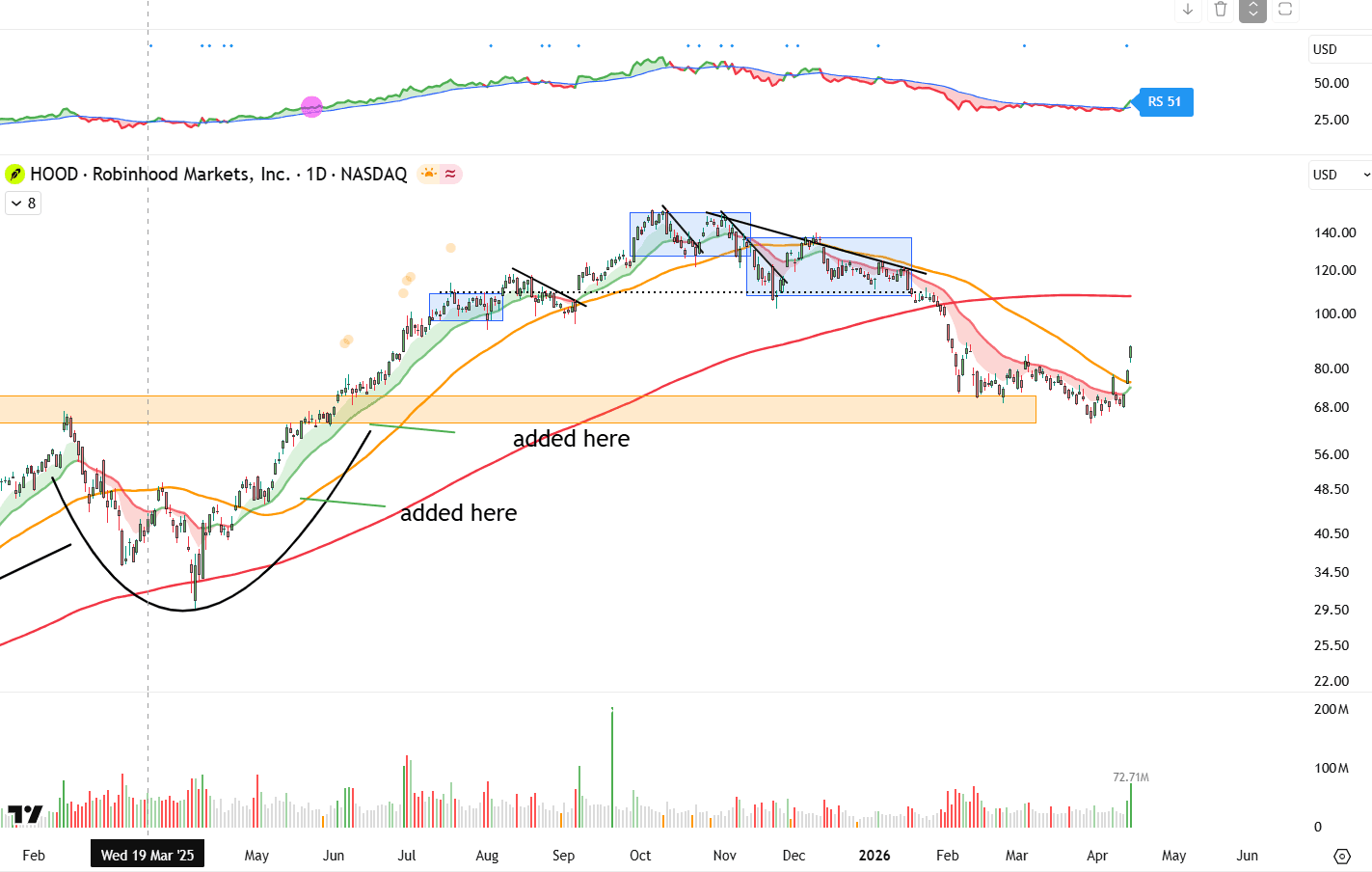

Robinhood $HOOD

Robinhood $HOOD

Robinhood is one of my key long-term holdings.

It’s the closest thing to a financial super app, with a huge market, an expanding moat, a visionary founder, a growing ecosystem, and a relentless speed of innovation.

But one of the key things I try to convey here is that timing is critical. Even great companies can get way ahead of themselves simply because of sentiment. Sometimes, fundamentals need time to catch up.

Robinhood has been in a correction since October last year. From peak to trough, it was down over 50%. That is a good lesson that even great companies routinely correct, and exactly why risk management is so critical, even for long-term positions. That means reducing your position when the technicals deteriorate and increasing it when they improve.

Right now, it’s finally starting to reemerge from an early-stage base, and the catalyst are the new Trump Accounts.

On launch day, the app hit #1 in finance and #4 overall in the App Store. The fastest-growing app outside of AI.

Trump Accounts are investment accounts for children, with eligible newborns from 2025 to 2028 receiving a $1,000 government contribution. The app was built with Robinhood and BNY, and funding starts on July 4, 2026. That gives Robinhood a direct role in a large government-backed savings program.

It is becoming financial infrastructure for the next generation.

Lin

AAPL

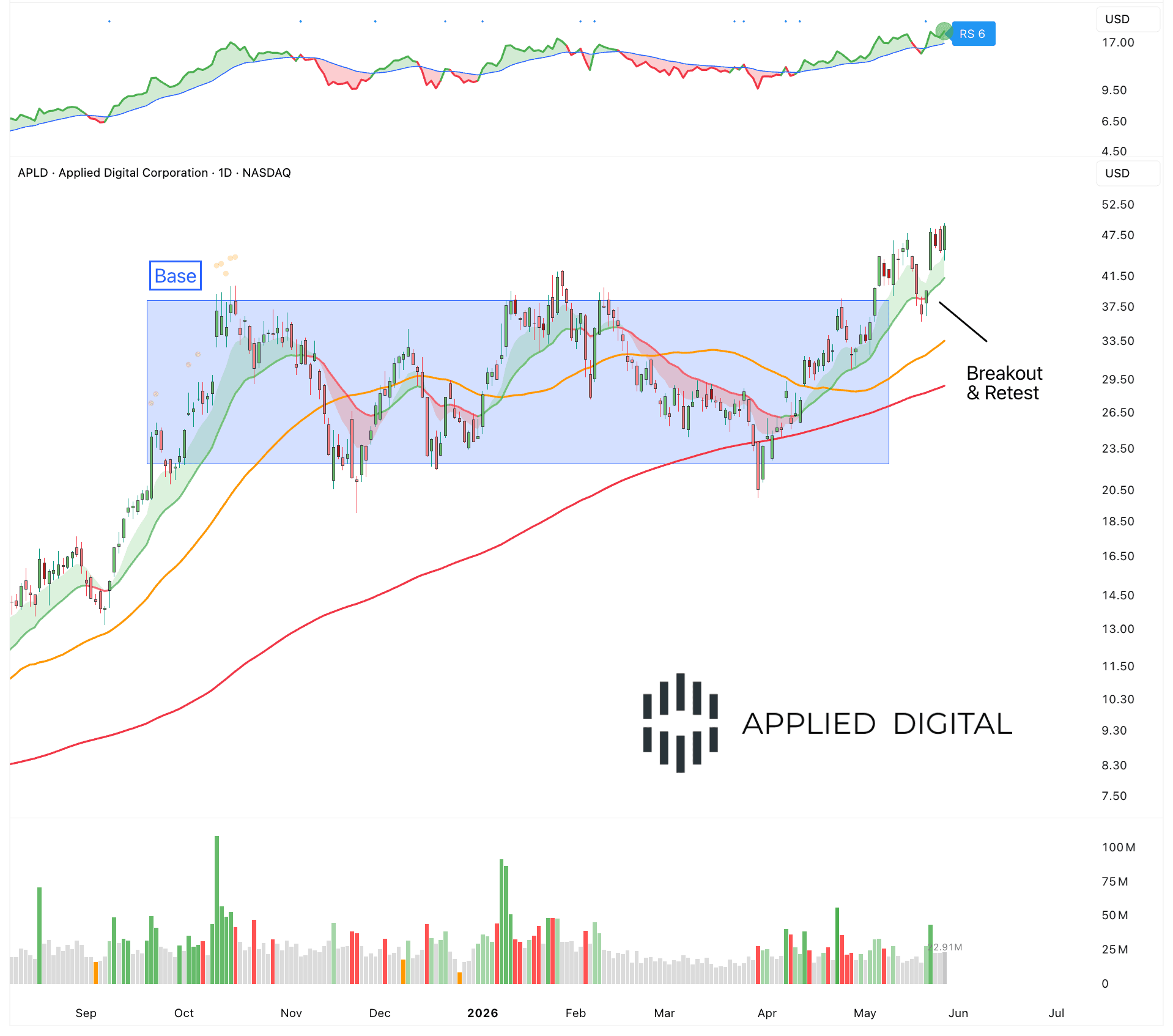

Applied Digital $APLD

Applied Digital $APLD

AI infrastructure demand is outrunning the physical world.

Hyperscalers and AI cloud companies need massive amounts of compute capacity. Today, the constraint has moved beyond GPUs. It is power, speed, and location. Applied Digital is building large-scale AI data center campuses in places where power is available and land is easier to develop.

The winners in this cycle will not only be the companies with the best chips or models. They will also be the companies that can supply the most compute. And for that they need to secure land, power, cooling, permitting, construction capacity, and long-term customers.

Old data center model was built around internet traffic, cloud storage, SaaS workloads, and proximity to population centers. That is no longer true for AI.

Training and inference workloads do not always need to sit next to major cities. What they need most is cheap power, available grid capacity, cooling efficiency, and the ability to deploy thousands of GPUs at scale.

In June 2025, the company announced 2 roughly 15-year lease agreements with CoreWeave for 250 MW at its Ellendale, North Dakota campus. Reuters reported that the leases were worth about $7 billion over the term.

And in its fiscal Q3 2026 update, Applied Digital said Polaris Forge 2 is a 200 MW investment-grade hyperscaler campus, while Delta Forge 1 is a 300 MW AI factory campus backed by a high investment-grade hyperscaler, with initial operations expected in mid-calendar 2027.

What’s important is that Applied Digital has moved past 1 GW of contracted capacity.

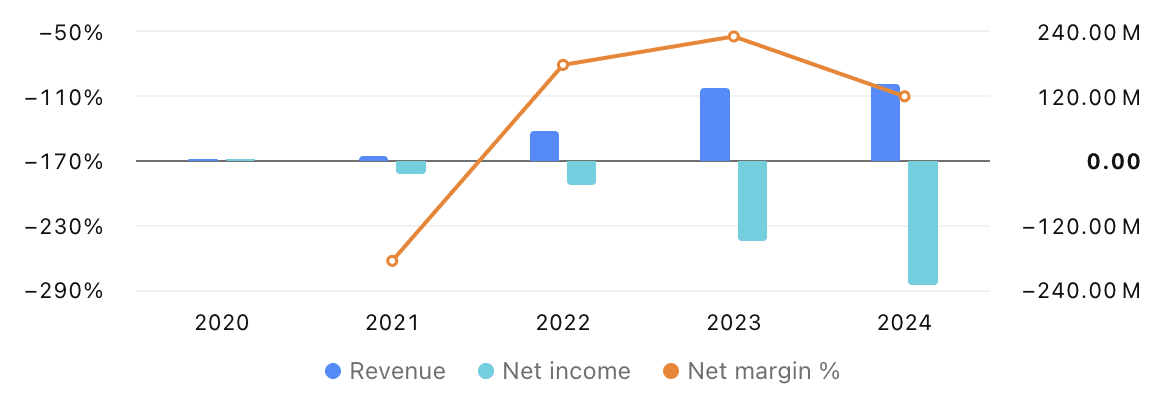

In fiscal Q3 2026, revenue was $126.6 million, up 139% year over year from $52.9 million. Revenue is starting to scale as more nad more facilities come online. Adjusted revenue, which excludes the Cloud Services business, was $108.6 million. Adjusted EBITDA was $44.1 million, compared with $6.3 million in the prior-year quarter.

Now the setup looks even more interesting. Applied Digital just broke out of a 10-month base and then came back to retest the breakout area almost perfectly.

And it’s not just Applied Digital. The whole sector is starting to lead, and that is exactly what you want to see. The best moves usually happen when the stock is not moving in isolation, but together with the entire sector - as mentioned here.

Lin

AAPL

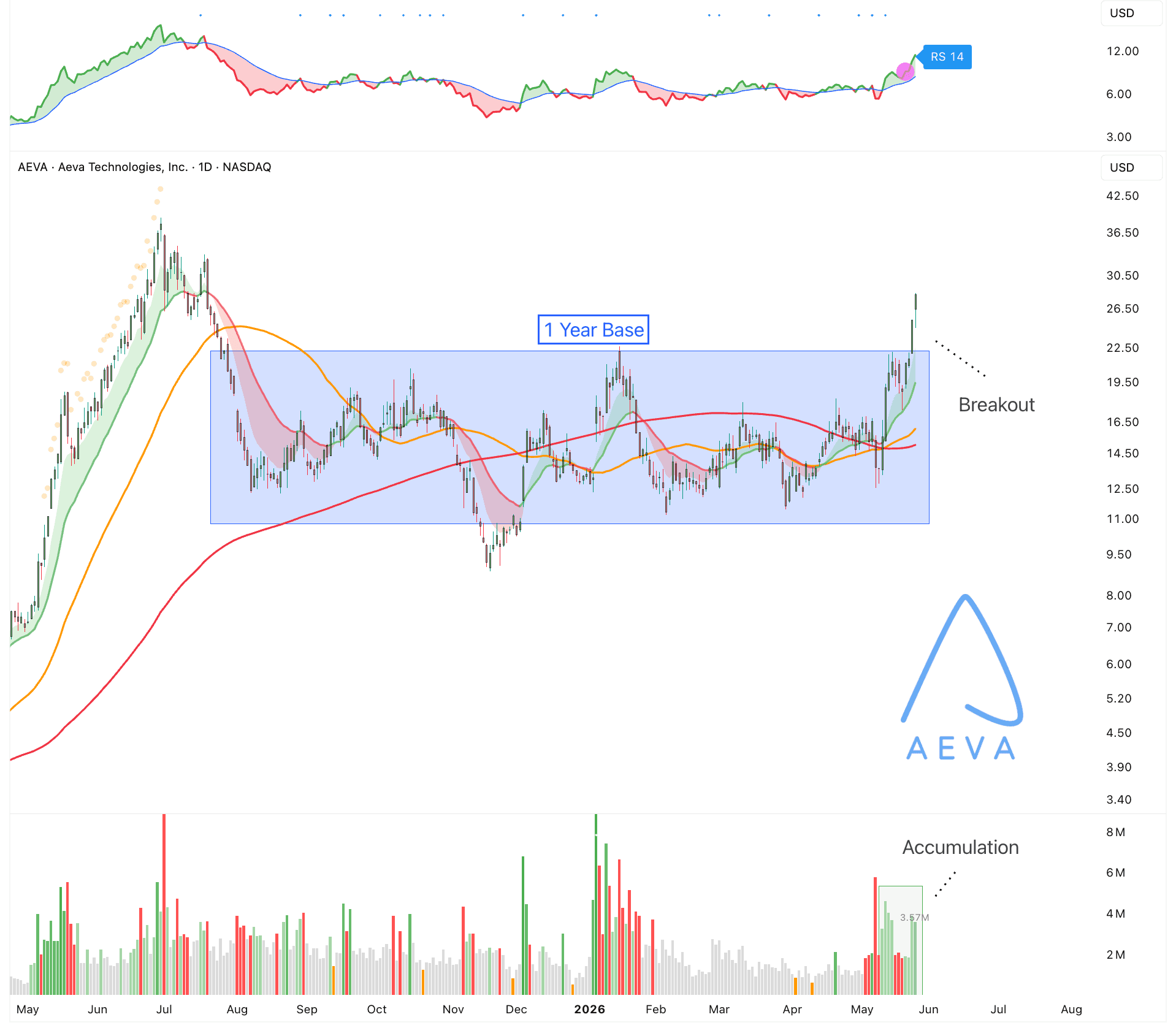

AEVA $AEVA

AEVA $AEVA

Aeva is one of the more interesting small-cap names in the lidar space. It has a lot of similarities to Ouster.

Ouster is building digital lidar sensors that help machines create a precise 3D map of the physical world, while Aeva is building 4D lidar sensors that add instant velocity data, helping machines understand not just where objects are, but how fast they are moving and where they may go next.

It’s basically motion intelligence.

As AI moves from software into the physical world, machines will need a much deeper understanding of their environment. A robot, autonomous truck, drone, or industrial machine does not just need to know what is around it. It needs to know how far away objects are, how fast they are moving, and how that movement is changing in real time.

Aeva’s technology is built around 4D lidar. Traditional lidar gives machines a 3D map of the environment. Aeva’s FMCW lidar adds direct velocity measurement. That means its sensors can measure both distance and speed at the same time.

And motion is one of the hardest problems in autonomy.

A camera can identify objects. Radar can detect speed, but with less precision. Traditional lidar can map depth. Aeva is trying to combine high-resolution depth and instant velocity into one sensing layer.

That makes the company a potential beneficiary of several major trends at once: autonomous trucking, advanced driver assistance, robotics, industrial automation, defense, smart infrastructure, aerospace, and factory inspection.

The company already has early validation from important partners. Aeva is working with Daimler Truck and Torc Robotics in autonomous trucking. It has been selected for Nvidia DRIVE Hyperion. It is also used in Nikon’s APDIS industrial inspection platform, which gives the company exposure beyond just automotive.

Many lidar companies have been too dependent on the slow adoption curve of autonomous vehicles. Aeva’s opportunity is broader. If its sensors can become useful in industrial automation, infrastructure monitoring, defense systems, and factory inspection, the company has more ways to grow while the automotive market develops.

Atlas Ultra is Aeva’s newest long-range 4D lidar sensor for Level 3 and Level 4 automated driving. It is designed to sit behind the windshield and help vehicles detect objects at highway speeds. That could make adoption easier for OEMs because the sensor is more integrated and less intrusive.

In Q1 2026, revenue was $6.3 million, up about 90% year over year. Management is guiding for 70% to 100% revenue growth in 2026. That is strong growth, but from a small base.

It’s the definitely on the more speculative end. But it’s breaking out of a year long base that could be a good opportunity to initiate a position if you manage the risk accordingly.

Lin

AAPL

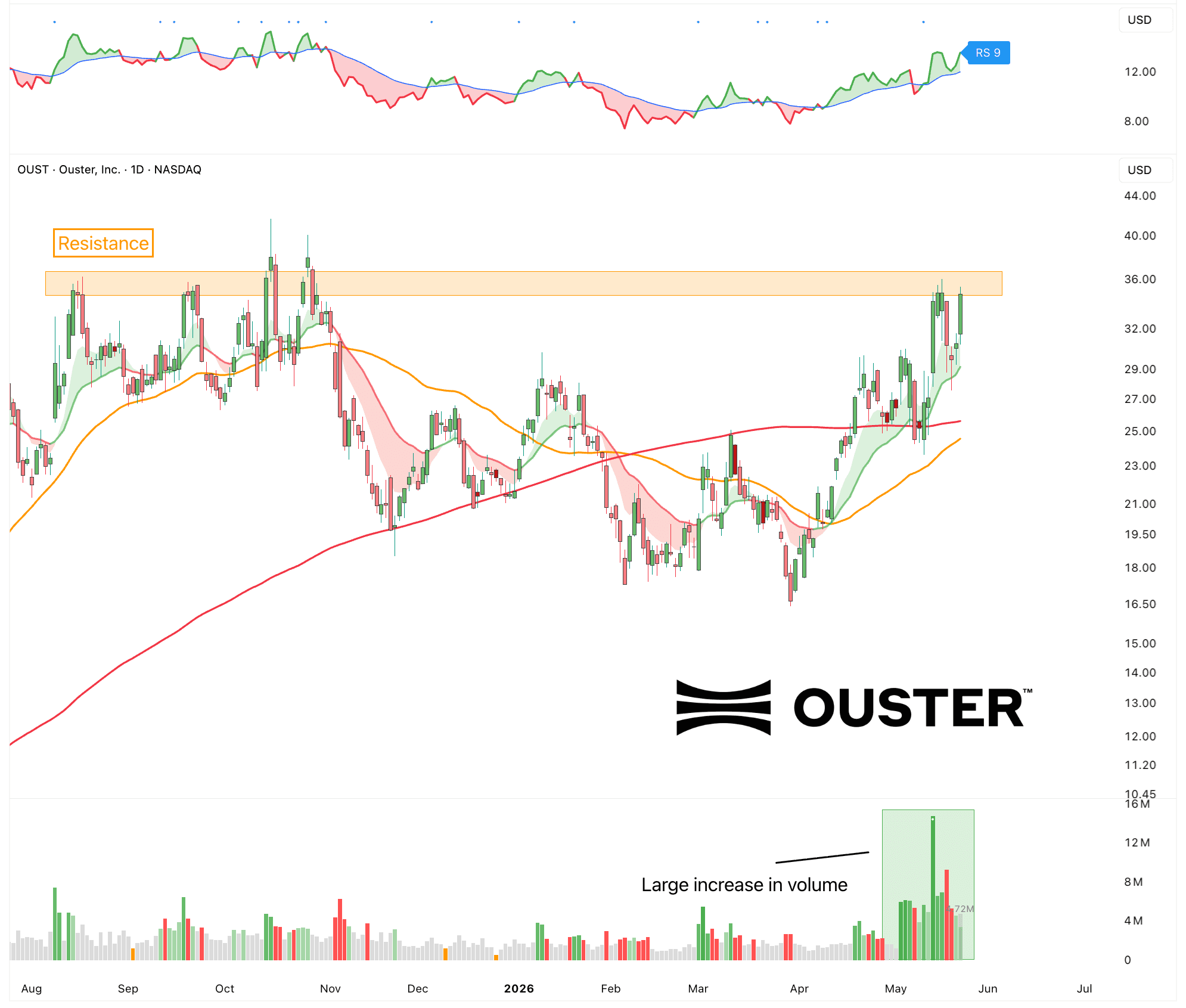

Ouster $OUST

Ouster $OUST

Ouster is a lidar company. It makes sensors that help machines see the real world in 3D.

The next big AI wave is not just chatbots or ai agents. It is robots, autonomous vehicles, drones, industrial machines, smart cities, warehouses, ports, security systems, and infrastructure that can understand what is happening around them.

Its core product is digital lidar. Lidar sends out light pulses and measures how long they take to return. That creates a 3D map of the environment. A camera sees color and texture. Radar sees rough distance and speed. Lidar gives machines precise depth. And is critical for autonomy.

Ouster sells into 4 main markets: industrial, robotics, automotive, and smart infrastructure. It’s goal is to create a platform for Physical AI combining lidar, cameras, AI compute, sensor fusion, perception software, and AI models.

Its sensors can be used in warehouses, factories, mining, ports, traffic intersections, security, delivery robots, mapping, agriculture, construction, and autonomous machines.

And just recently it launched Rev8. Rev8 is the world’s first mass-produced native color lidar sensor. So, instead of needing separate camera and lidar systems, Rev8 can capture 3D depth and color together in one sensor. That can reduce hardware complexity and make sensor fusion easier for robots and autonomous systems

In Q1 2026, revenue was $49 million, up 49% year over year. Product revenue was $48 million, up 55% year over year and 18% sequentially. The company also shipped more than 12,600 lidar and camera sensors, with lidar making up around 65% of the total.

That’s why it’s become a pretty popular name among retail and institutional investors recently. And that is clearly showing in the massive increase in accumulation volume. It’s one the verge of a breakout. But keep in mind that it can be very volatile.

Lin

AAPL

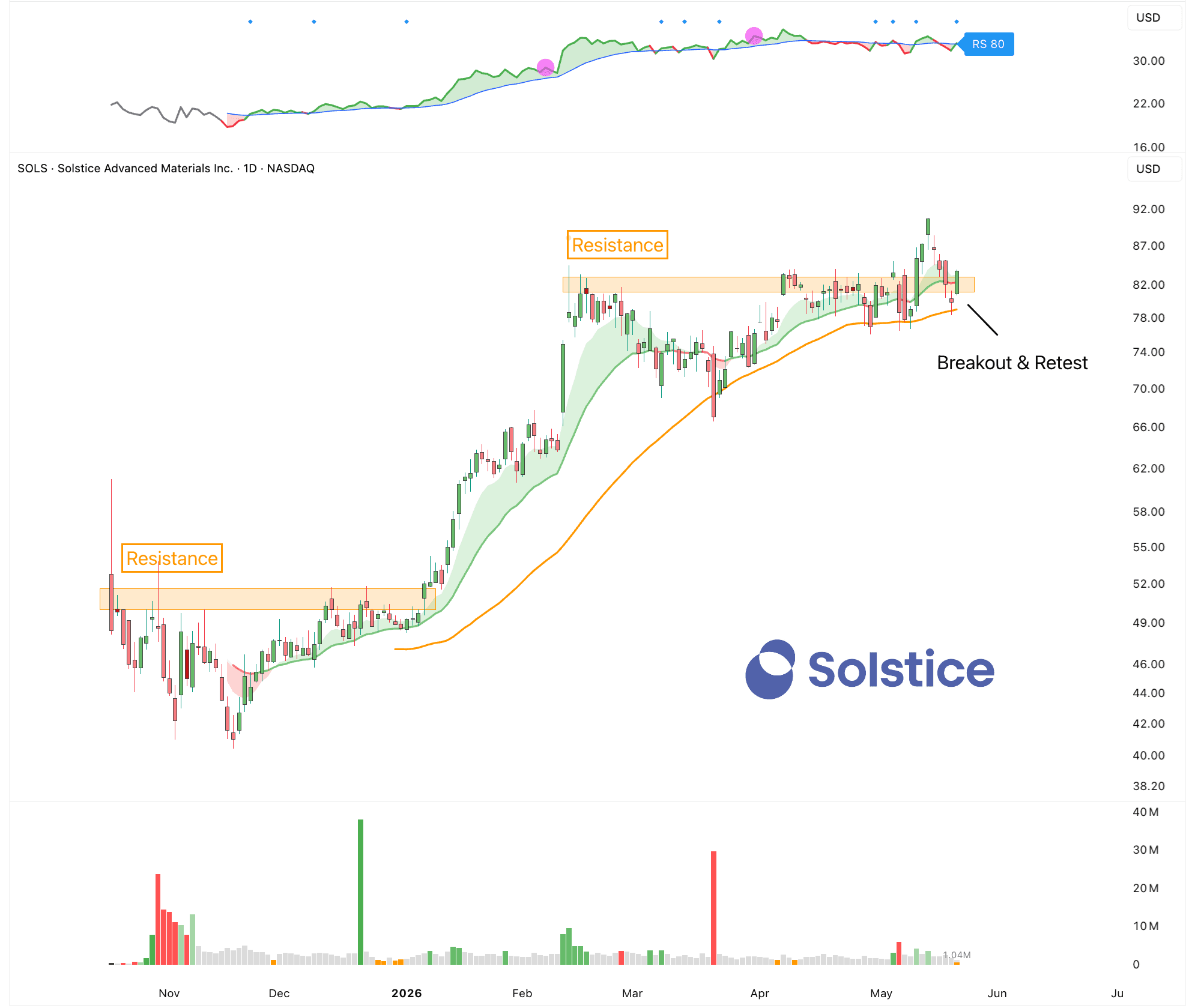

Solstice $SOLS

Solstice $SOLS

At first glance, Solstice looks like a specialty materials and chemicals company. It was spun out of Honeywell and has businesses across refrigerants, advanced materials, electronic materials, healthcare packaging, and industrial chemistry. But I think that simple view misses one of the most interesting parts of the company.

The key part is Metropolis Works in Illinois. This is the only uranium conversion facility in the United States. It converts uranium oxide into uranium hexafluoride, which is a required step between uranium mining and enrichment. As nuclear energy becomes more important again, especially because AI data centers need reliable power, this asset could become much more important than the market currently reflects.

Right now, Solstice is still mostly being valued like a chemicals company. That may be fair on the surface, but I think it may understate the value of the nuclear conversion business. If investors start looking at Solstice as a mix of specialty materials, nuclear infrastructure, refrigerants, electronic materials, and AI related thermal management, the valuation framework could change over time.

The recent Q1 2026 results were solid. Sales grew, guidance was reaffirmed, and the strongest growth came from the areas that matter most to my thesis: Nuclear, Electronic Materials, and Refrigerants. Nuclear revenue grew 27% year over year, helped by both pricing and volume.

The nuclear business is the main reason I’m interested, but the rest of the portfolio also adds value. Refrigerants could benefit from the transition to next generation products and the growing cooling needs of AI data centers. Electronic materials give $SOLS exposure to advanced semiconductor manufacturing. Thermal management could become more important as AI moves into robots, autonomous systems, drones, and other physical machines.

This could be a very compelling long-term opportunity. And right it's setting up for a perfect low risk entry after a breakout and retest of its previous highs.

Lin

AAPL

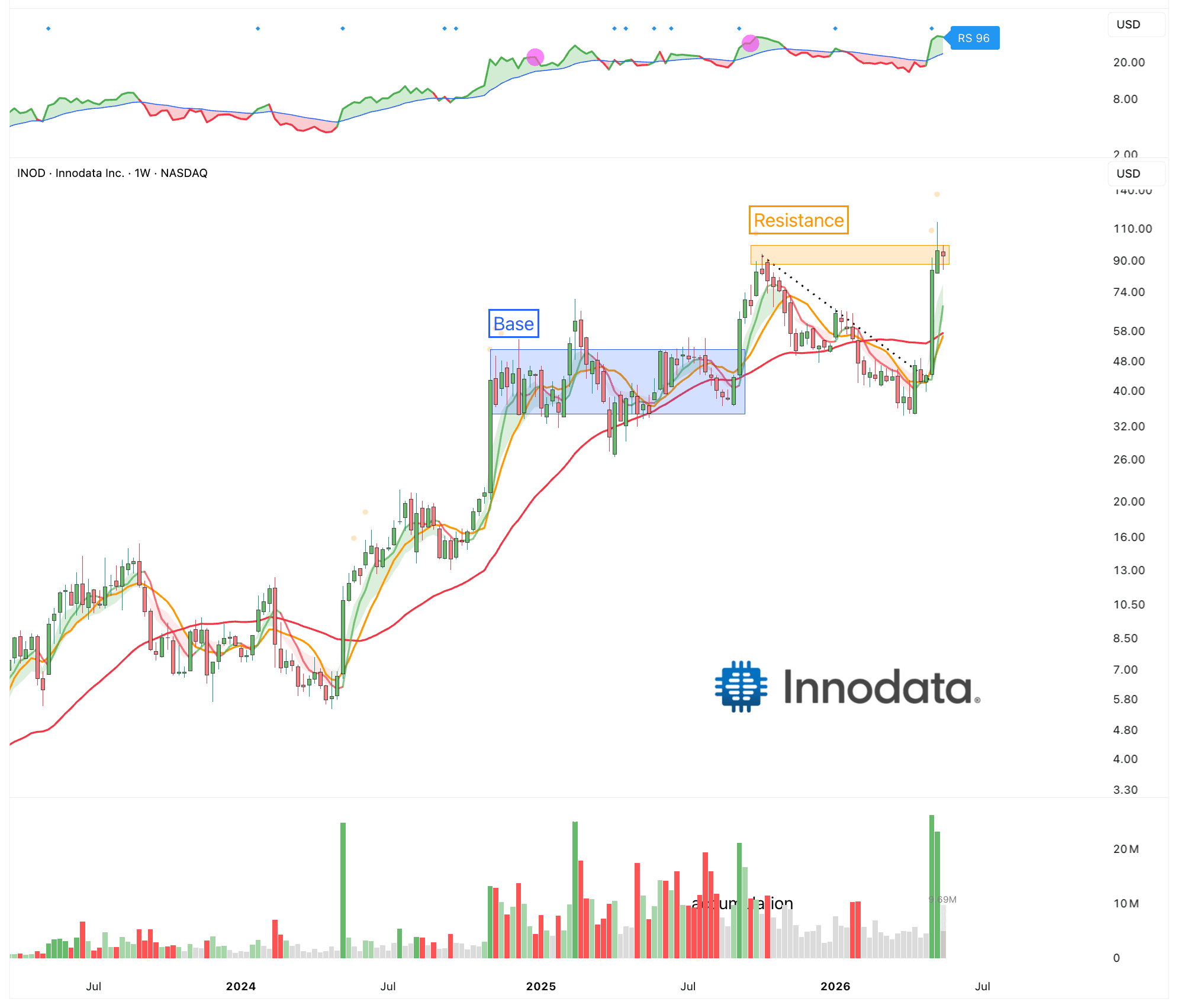

Innodata $INOD

Innodata $INOD

Innodata is one of the fastest growing software companies.

Innodata provides services and platforms for AI builders and AI adopters. Its work includes data annotation, data engineering, model training support, model safety testing, red teaming, human preference optimization, and evaluation workflows. Basically, Innodata helps AI companies and enterprises turn messy data into useful AI systems.

The most attractive part of Innodata is that it is exposed to one of the most important bottlenecks in AI: trusted data and model evaluation. AI models can be powerful, but they still make mistakes, hallucinate, fail edge cases, and behave unpredictably. For companies using AI in real products, this creates a huge need for testing, improvement, and monitoring.

It has already won over high-quality customers like Palantir. Palantir selected Innodata to provide training data and annotation for AI projects, including multimodal data involving video, imagery, and sensor analysis.

In Q1 2025, Innodata reported revenue of $58.3M, up 120% year over year. In Q1 2026, revenue reached $90.1M, up 54% year over year, and the company raised its full-year 2026 revenue growth guidance from more than 35% to 40% or more.

But it’s important to keep in mind that it can be a very volatile stock.

Lin

AAPL

Navitas $NVTS

Navitas $NVTS

Navitas Semiconductor is a next-generation power semiconductor company focused on gallium nitride and silicon carbide chips. These are not normal chips like Nvidia GPUs. They are power chips. Their job is to move electricity more efficiently, with less wasted energy, less heat, and higher power density.

AI data centers do not just need more chips. They need more electricity, better power conversion, better cooling, less copper, and more efficient power delivery. Because data centers are becoming extremely power hungry. As AI racks move from kilowatts to hundreds of kilowatts and eventually megawatt-scale systems, the power architecture inside the data center needs to change.

Navitas originally became known for GaN fast chargers, especially in mobile and consumer electronics. But it has pivoted move into bigger, higher-value markets like AI data centers, grid and energy infrastructure, performance computing, and industrial electrification. As part of it’s Navitas 2.0 strategy it has developed GaN and SiC products aimed at Nvidia’s next-generation 800V DC AI factory architecture.

The company’s revenue base is small. In Q1 2026, Navitas reported $10 of revenue,

Lin

AAPL

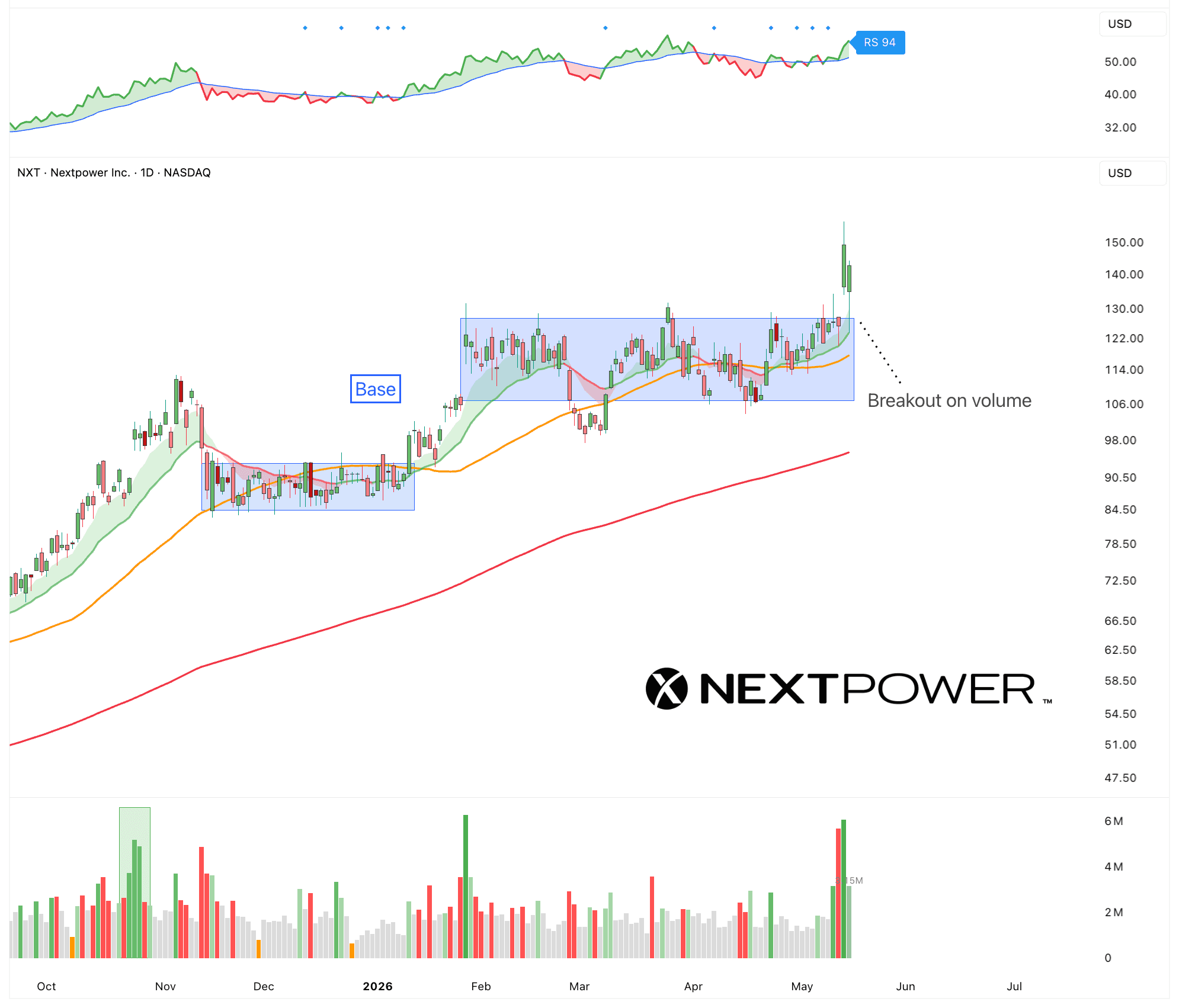

Nextpower $NXT

Nextpower $NXT

I've talked about Nextpower $NXT a while ago but it's worth highlighting again.

Traditional solar panels are fixed, which limits the amount of sunlight they can capture.

That’s where Nextpower comes in.

They build solar tracking systems with intelligent motors and software that make panels follow the sun throughout the day. Each tracker uses sensors, algorithms, and cloud software to adjust in real time for wind, terrain, and sunlight.

The result is up to 25% more energy output from the same panels.

Until now they’ve deployed systems on more than 90 gigawatts of solar projects across over 30 countries. And Nextracker works with many of the world’s largest renewable energy developers and utilities

They are profitable, growing steadily 25% year after year, and trade at a PE of 32.

All of this comes at a time when valuations across the solar industry have pulled back after four challenging years. The sector’s fundamentals are now starting to stabilize. As global electricity demand accelerates, driven mostly by data centers to power AI.

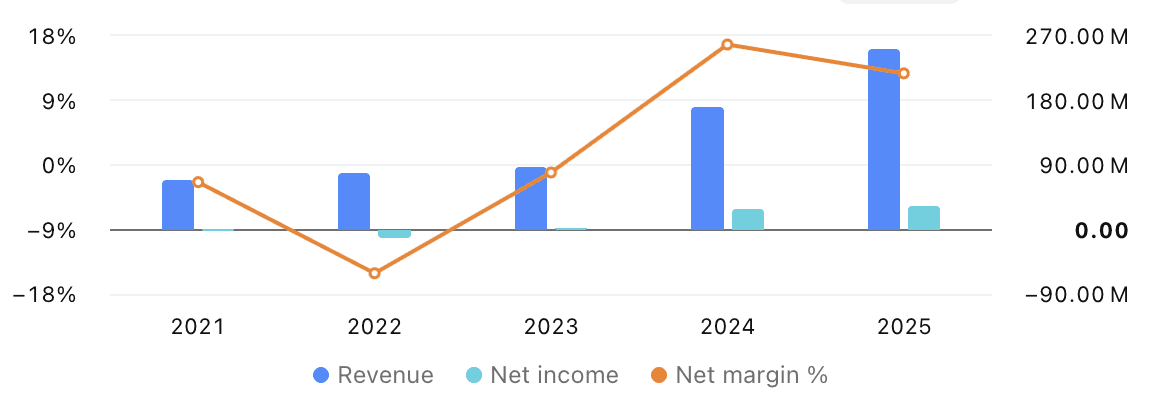

NXT’s earnings were pretty strong overall. They beat expectations on both revenue and earnings, with Q4 revenue around $881M and adjusted EPS of $1.05. More importantly, FY26 revenue reached a record $3.56B, up 20% year over year, and backlog hit a record $5.25B+ and management reaised FY27 revenue guidance to $3.8B to $4.1B.

The Setup:

- Energy is a huge bottleneck

- Solar demand is growing

- NXT expanding beyond basic tracker

- Breakout to new highs after basing for 5 months

Lin

AAPL

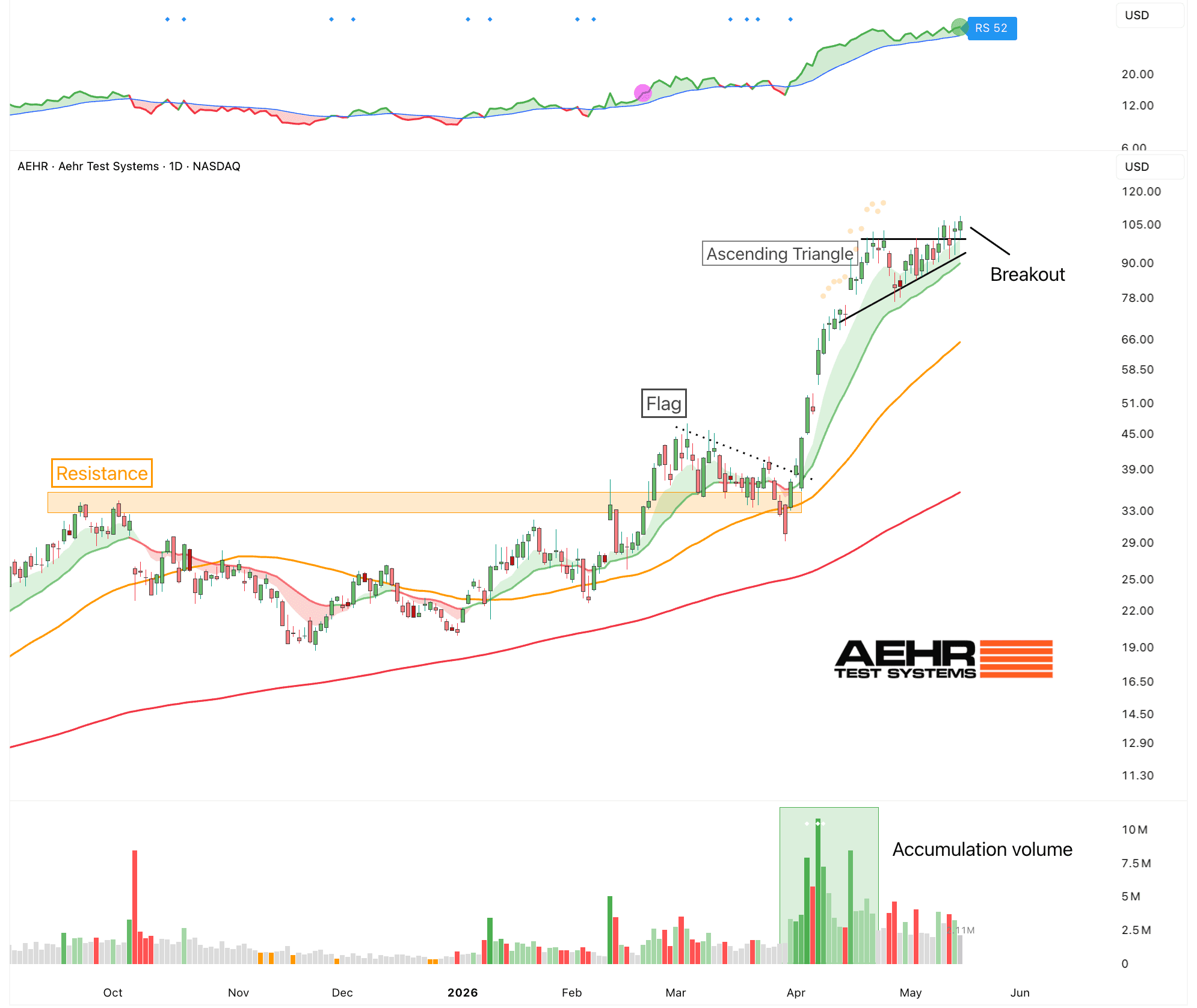

Aehr Test Systems $AEHR

Aehr Test Systems $AEHR

Every chip can look great in the lab. But the lab is controlled, clean, and predictable. The real world is not. The real world is hot, unstable, messy, and unforgiving.

That is where Aehr Test Systems comes in.

Aehr builds advanced testing systems that stress-test chips before they are used in real products. These chips end up inside electric vehicles, fast chargers, solar inverters, industrial machines, data centers, and other high-voltage power systems where reliability matters. In these markets, a failed chip is not just a small technical issue. It can lead to costly repairs, downtime, safety risks, and damaged customer trust.

The company’s core focus is burn-in testing. Burn-in testing means forcing chips to operate under difficult conditions before they are shipped to customers. Aehr’s systems expose chips to heat, voltage, long operating times, and other stress factors. The goal is simple: find the weak chips before they fail in the real world.

This is especially important for silicon carbide chips, also called SiC chips. Silicon carbide is becoming one of the most important materials in modern power electronics because it can handle high voltage, high temperature, and high power more efficiently than traditional silicon chips. That makes SiC critical for electric vehicles, charging infrastructure, solar energy, industrial power systems, and other applications where efficiency and reliability are essential.

Aehr reported more than $37M in quarterly bookings in fiscal Q3 2026, driven by AI, data center infrastructure, and silicon photonics demand. Revenue was still unimpressive, but the backlog shows that demand is high. So, it might not be the strongest on the fundamentals but the technical setup looks good for short-term opportunity.

The Setup:

Winning a major new silicon photonics customer

The demand for AI and its supply chain is growing exponentially

Breaking out of an ascending triangle

Lin

AAPL

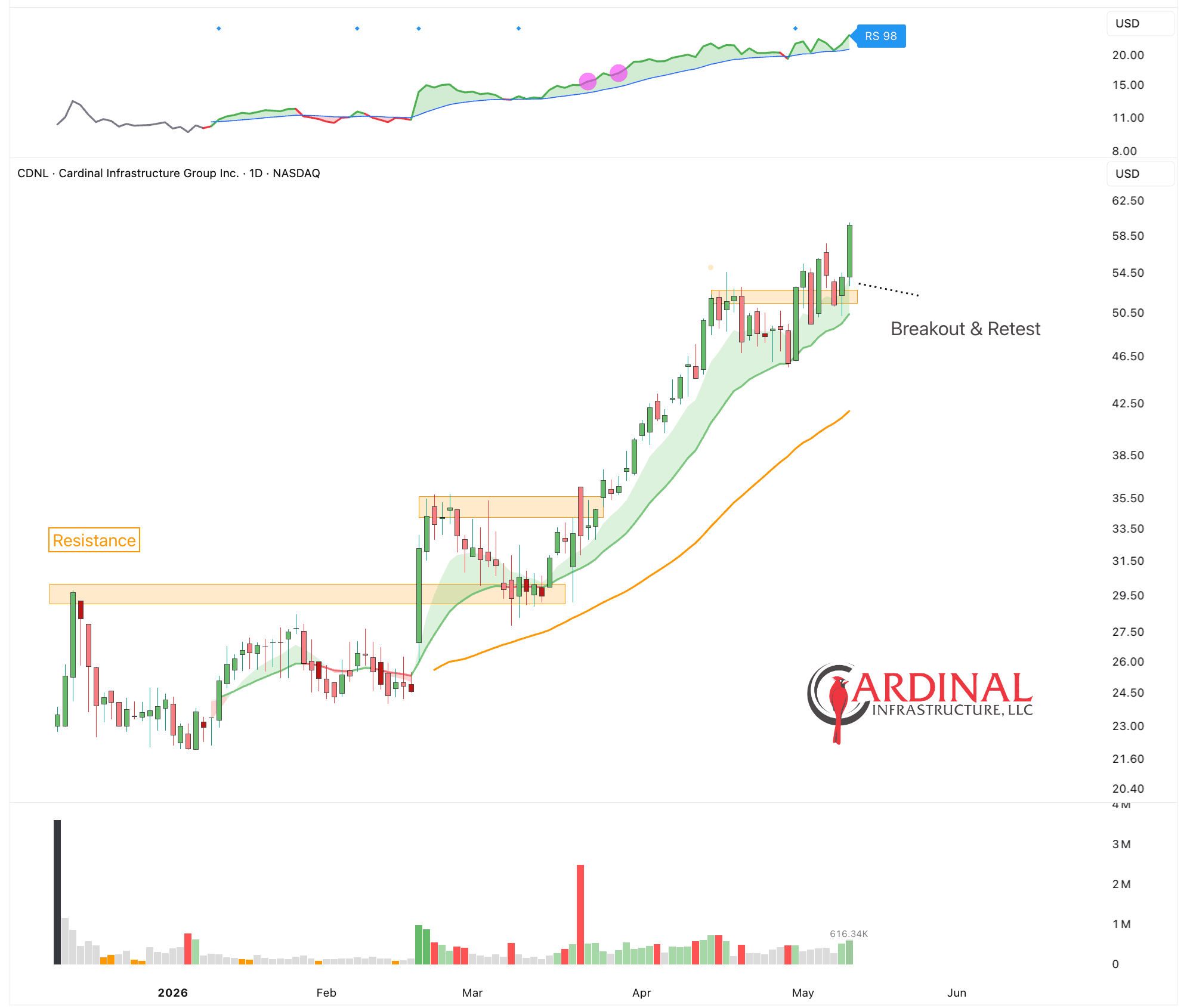

Cardinal Infrastructure $CDNL

Cardinal Infrastructure $CDNL

Cardinal Infrastructure is one of the more interesting recent IPOs in the market.

The company went public in December 2025 and was already added to the Russell 2000 and Russell 3000 in March 2026.

Cardinal focuses on site development and civil infrastructure work. And business is booming right now because of AI.

Before a massive data center can be built, the land has to be cleared, graded, connected to utilities, drained properly, and prepared for construction.

Water systems, sewer systems, underground utilities, roads, and stormwater infrastructure all need to be installed first. None of the high-tech infrastructure works without this physical foundation.

AI data centers alone are consuming enormous amounts of land, electricity, cooling, fiber connectivity, and utility infrastructure. The companies building these facilities need contractors that can move quickly and handle large-scale development projects. Cardinal is positioning itself directly inside that trend.

In April 2026, the company announced a $24 million contract for the first phase of a large multi-phase data center campus. This is important because it is Cardinal’s first major mission-critical data center project.

And you can clearly see the demand. Revenues And there is no end in sight.

The financials also show real momentum. Full-year 2025 revenue was $456 million, up 45% year-over-year and it’s continuing to accelerate.

The Setup:

Won its first major multi-phase data center campus contract

Russell index inclusion brings more institutional buying

AI data center construction is exploding

Lin

AAPL

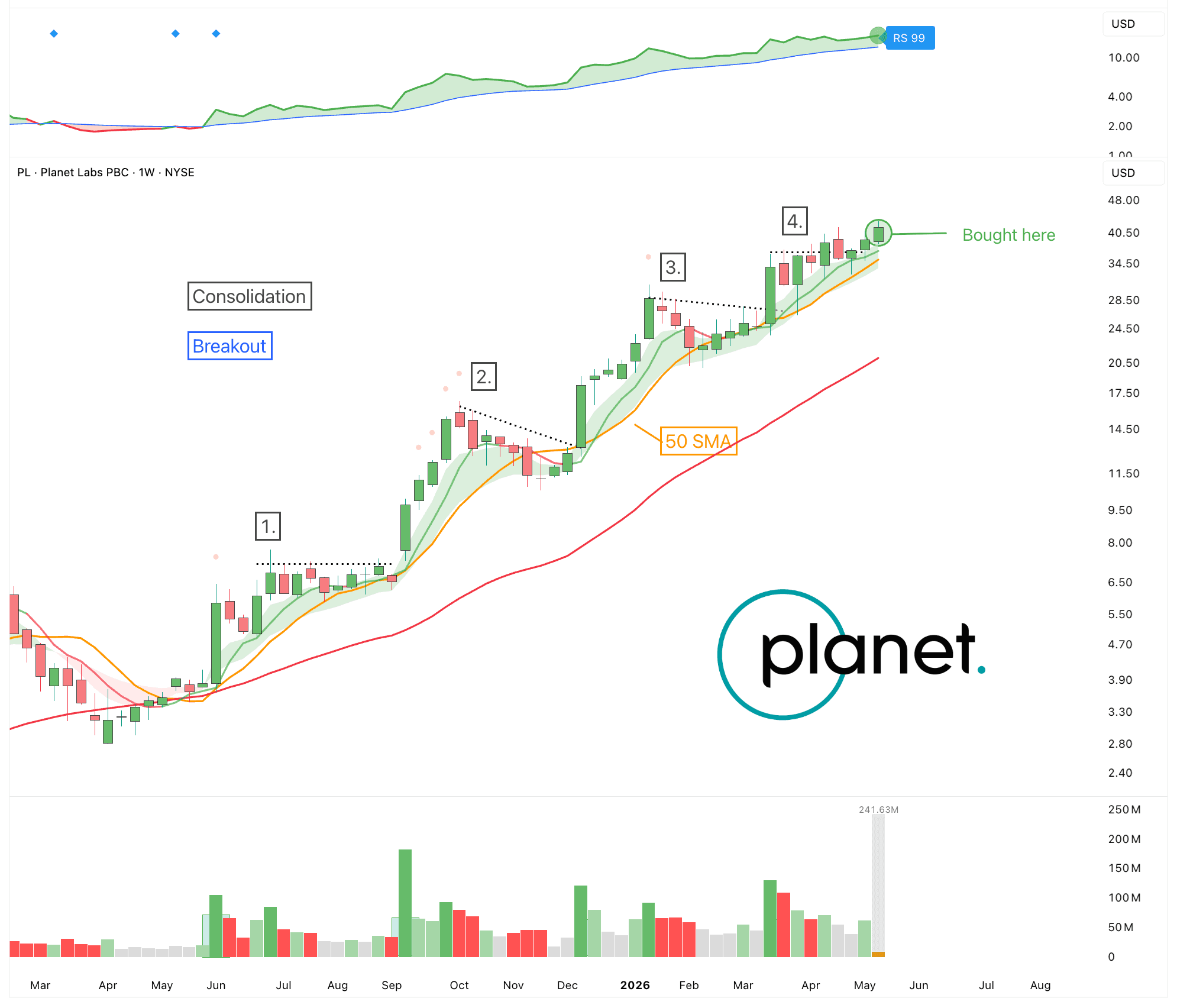

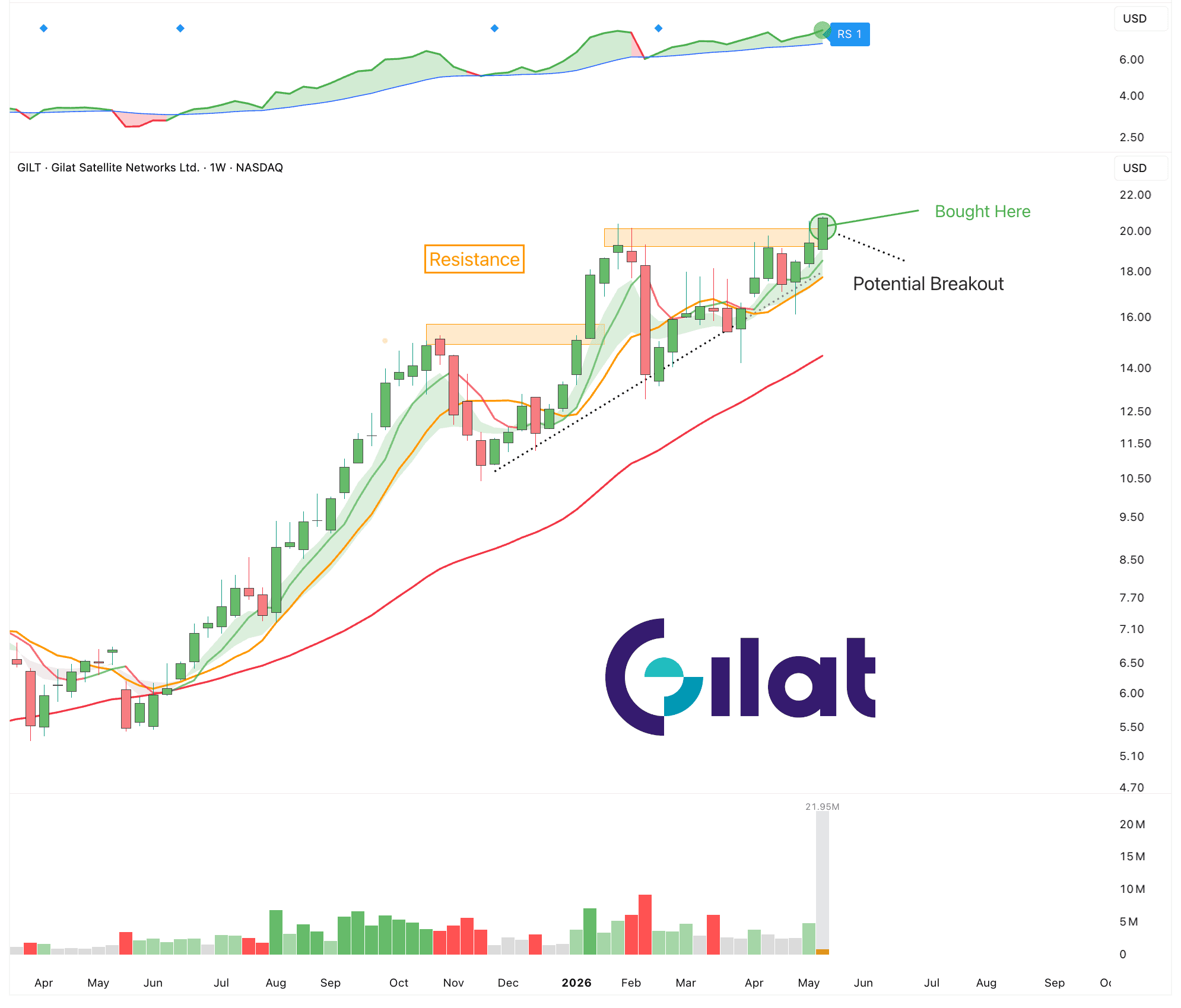

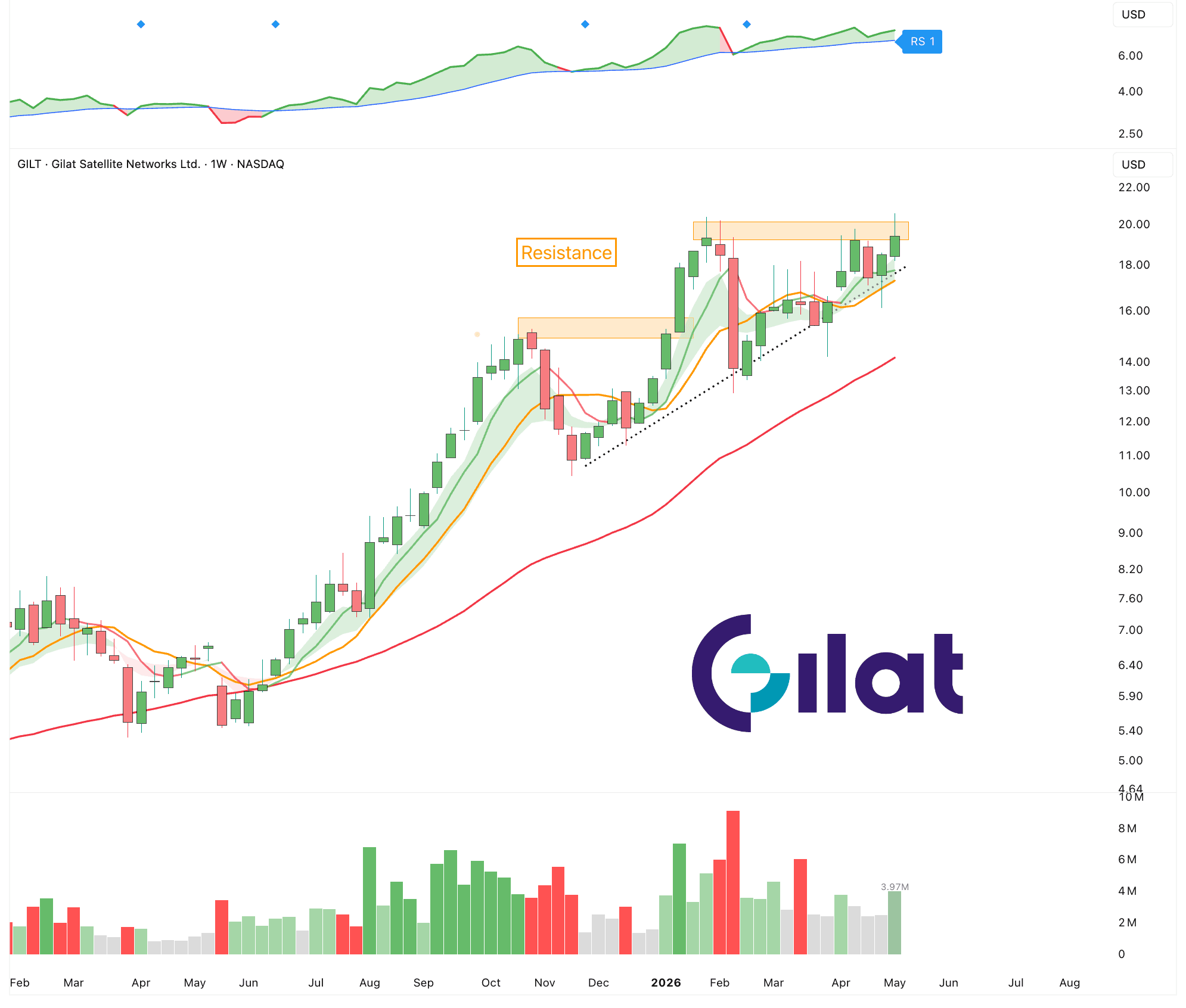

Bought $PL & $GILT

Bought $PL & $GILT

I’ve added two new positions.

Space continues to be one of my main focus areas. And I want more exposure to it. That’s why I’ve added $GILT and $PL.

I’ve written about $GILT yesterday and $PL about two weeks ago.

Both are breaking out together with the entire space sector.

Lin

AAPL

Robinhood $HOOD

Robinhood $HOOD

.Robinhood is starting to form a bottom

Lin

AAPL

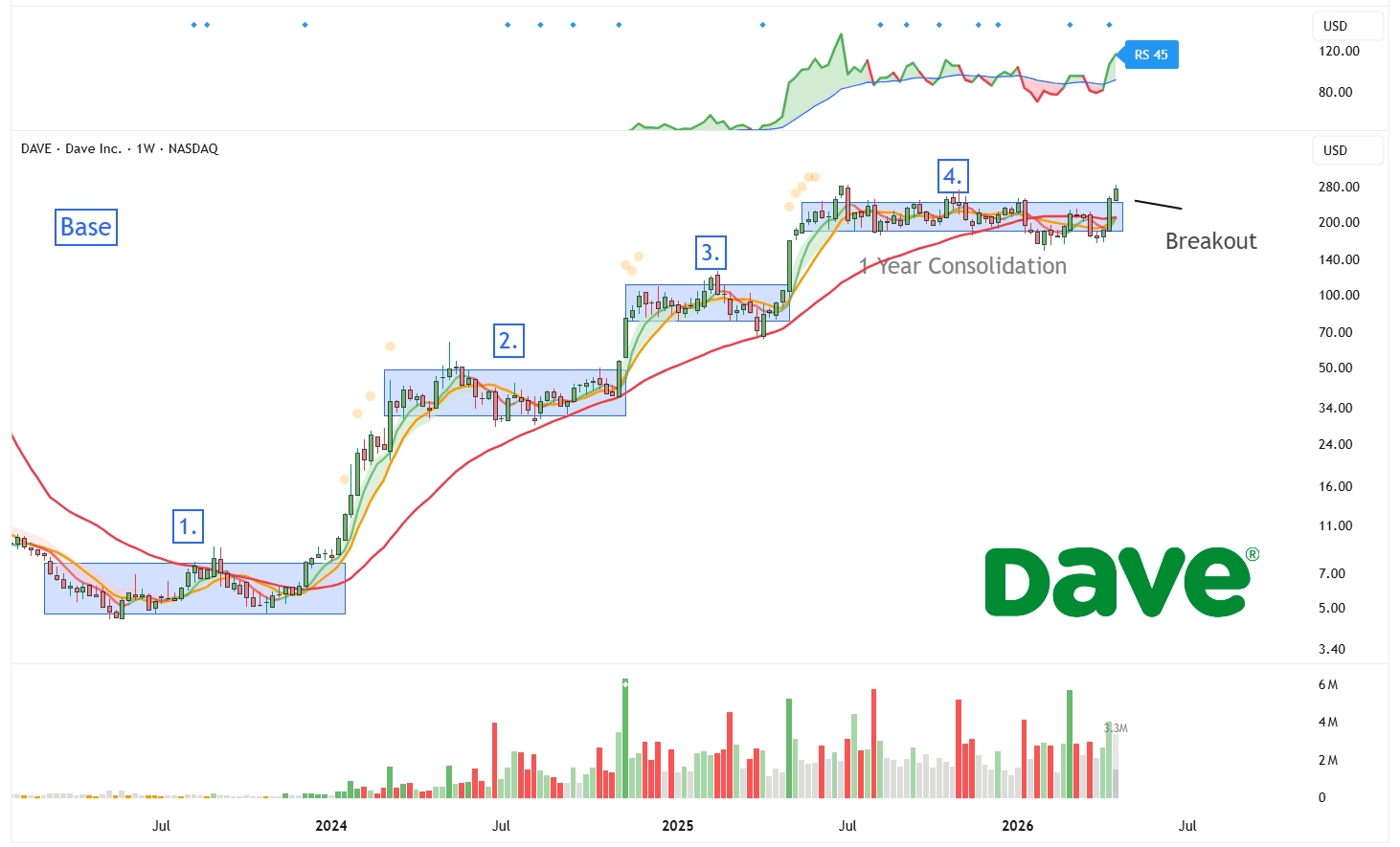

Dave $DAVE

Dave $DAVE

I’ve had a position a while ago because the technical thesis didn’t play out.

But now it’s back on the radar and honestly it looks a lot more interesting this time around. It is finally starting to break out after almost a full year of going sideways. That said, this is still a volatile name, so it’s important to size positions accordingly.

If you go back and look at the price action, there’s a pretty clear pattern that keeps repeating. It tends to spend months consolidating and building a base, then breaks out and moves quickly just to repeat the process again. The key thing to note is that the actual breakout phases are usually short and sharp.

The Setup:

Breakout of a year-long consolidation

Operating leverage is kicking in leading to revenue acceleration

Dave’s business benefits from a harder macro setup and rising inflation

Steady compounder growing every year and every quarter

Lin

AAPL

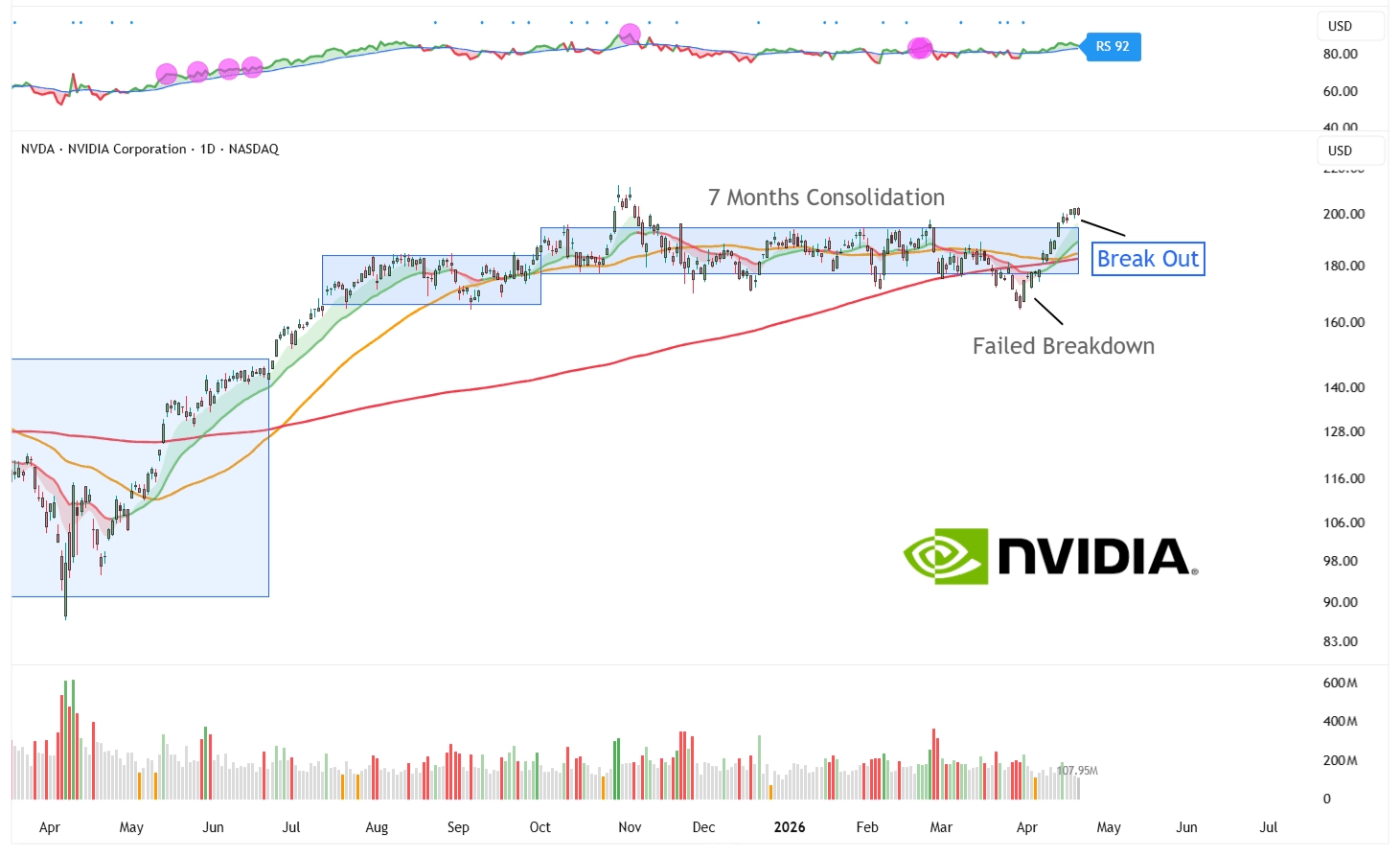

Nvidia $NVDA

Nvidia $NVDA

There is not much more to say about Nvidia.

I’ve been bullish for over 10 years and still am. It remains the most important company in the world and the leader in AI.

The Setup:

Breakout of a 7 months-long consolidation

AI developments continue to accelerate

Unprecedented revenue and earnings growth

Valuation has come down while fundamentals have improved

Semiconductor sector is hitting new all-time highs alongside $AVGO, $AMD, $TSM etc.

Lin

AAPL

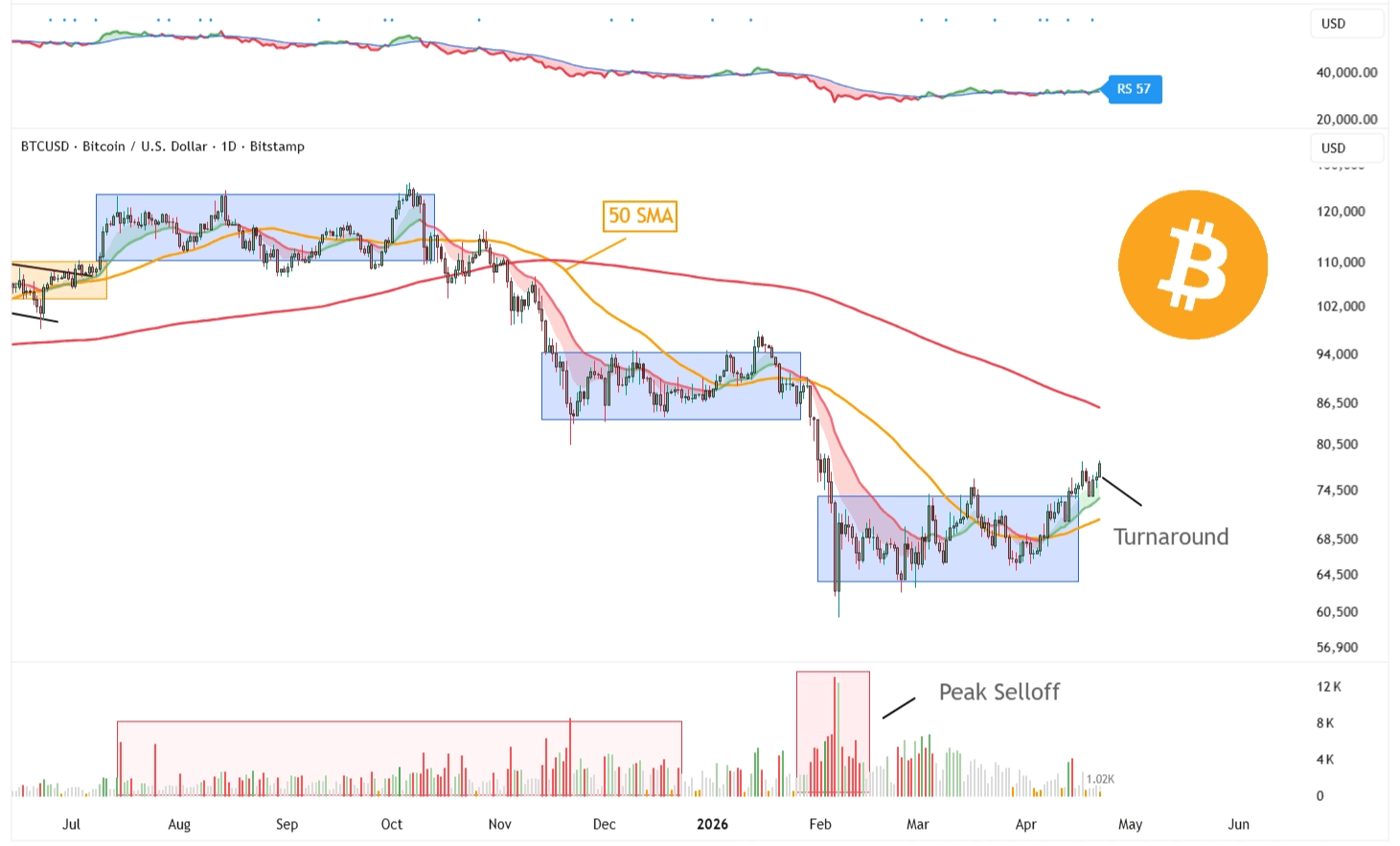

Bitcoin $BTC

Bitcoin $BTC

This is the first time in over a year that Bitcoin is starting to set up.

It’s not the cleanest setup, especially in this market, but it’s worth keeping an eye on and could make sense if you’re looking to start or add to a long-term position or as a short-term trading opportunity. And if this is the turning point, it will also likely start the rally in all the crypto adjacent names. But there will also be plenty of opportunities to add more.

The Setup:

Peak selloff volume in February

Breaking out of a bottom base

Building higher highs

Improving sentiment

Lin

AAPL

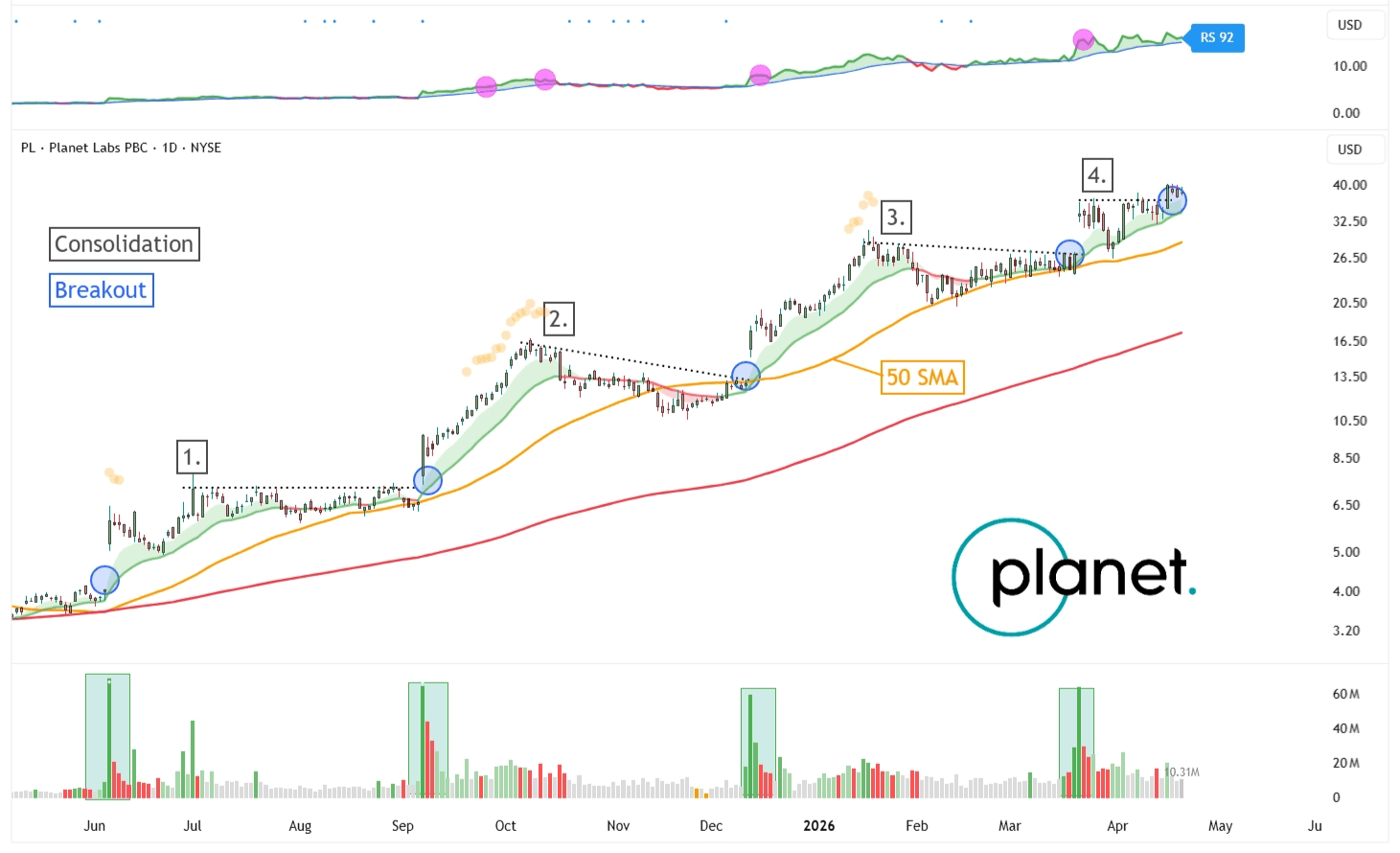

Planet Labs $PL

Planet Labs $PL

The SpaceX IPO is coming closer and closer. That will create a ripple effect through out the entire sector.

And Planet Labs is one of the more interesting names in this space. Planet Labs operates a fleet of small satellites that capture daily images of the Earth and turn them into data used to track changes.

The stock has been on a picture perfect advance. This is one to bookmark. The moves have been pretty linear. Every breakout is followed by a tight consolidation. It rallies, then pauses, then ralliesagain. This is exactly what leading stocks do.

The Setup:

Breakout of tight consolidation

Satellite data demand is exploding with massive backlogs

Lin

AAPL

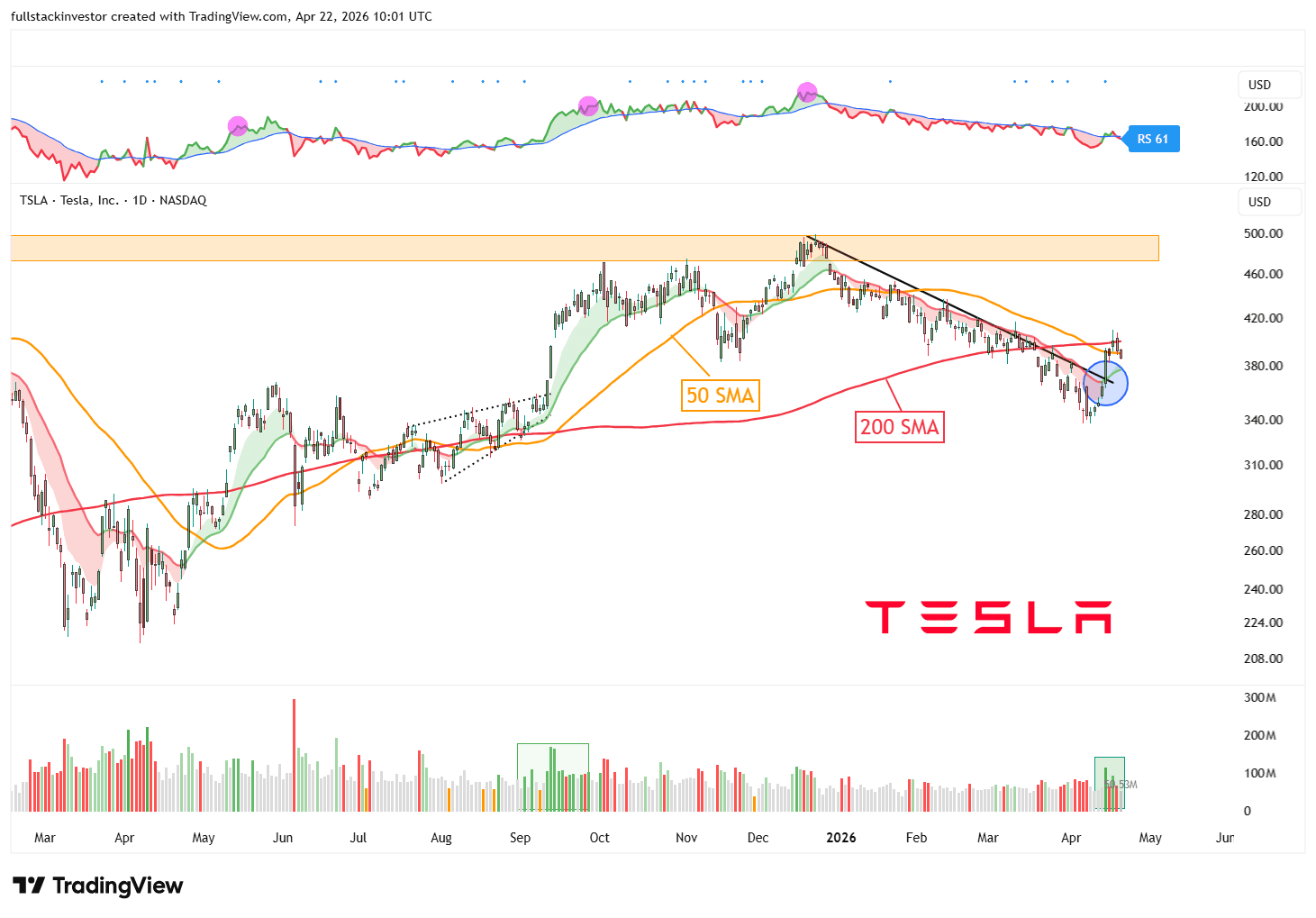

Tesla $TSLA

Tesla $TSLA

Tesla is setting up again after a 4 month long correction.

It’s still the best play on physical AI and the key driver will be FSD and robotaxis expanding globally. That will unlock trillions of value but there is still a long way ahead. It’s a big bet. But few people are capable of achieving that and one of that is Elon.

Tesla is not a car company anymore. It is an AI, robotics, autonomy, and energy infrastructure company wrapped inside an EV company.

And keep in mind that earnings are tonight afterhours.

The Setup:

Breakout of a downtrend and sitting right at key moving averages

Robotaxis starting to expand into new cities

Investing aggressively in the AI buildout and Terrafab

Energy business is growing rapidly

Announced new chip AI5

Lin

AAPL

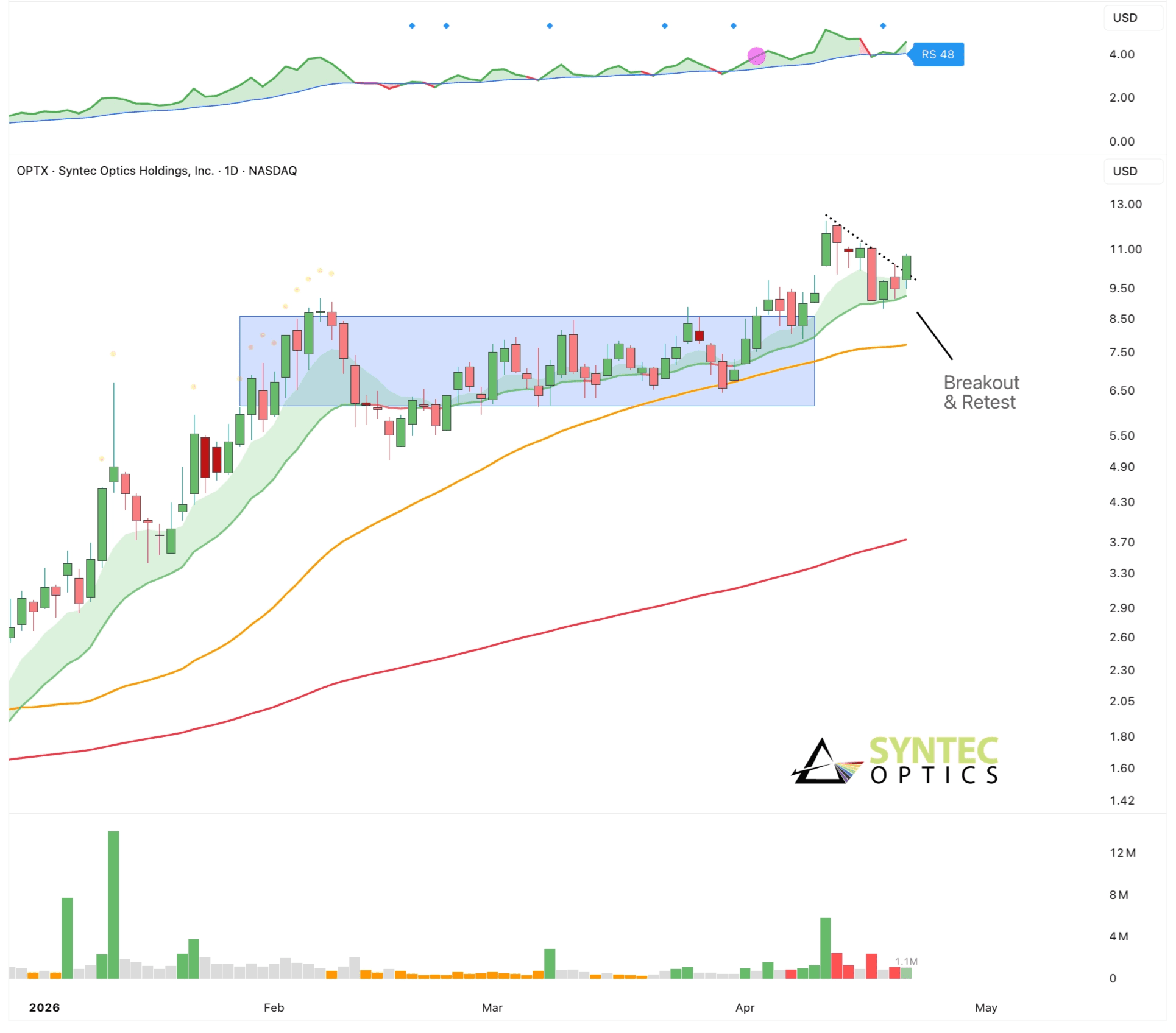

Syntex Optics $OPTX

Syntex Optics $OPTX

Photonics and optics have been one of the hottest sectors lately.

Syntec Optics designs and manufactures very precise optical components. Think lenses, mirrors, and optical assemblies that control and guide light. These parts are used in things like semiconductors, medical devices, defense systems, and laser-based equipment.

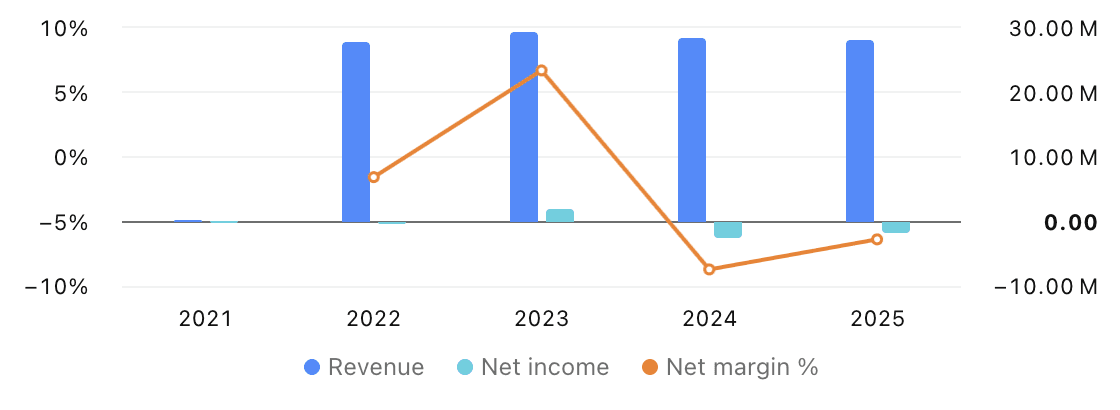

Fundamentally, not much has changed. The business has been fairly stagnant, so this is more of a short-term play taking advantage of the current market sentiment. It’s a small cap stock that is very volatile, so keep that in mind.

The Setup:

Part of the leading theme

Just broke out of a base and retested the breakout area

Capitalizing on short-term trend

Lin

AAPL

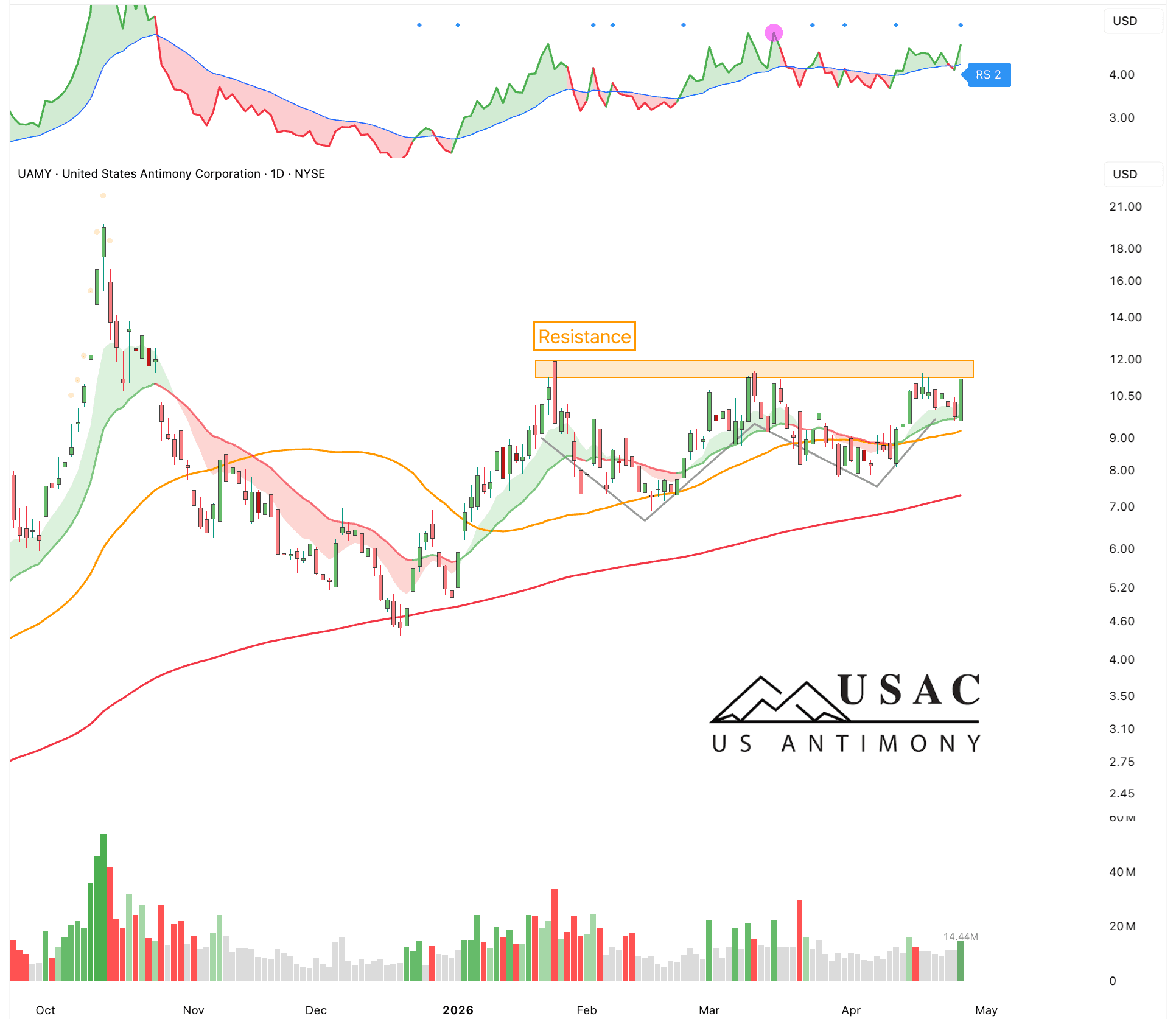

United States Antimony $UAMY

United States Antimony $UAMY

One of the interesting sectors setting up are rare earths.

US rare earths supply is the #1 national security priority right now.

The United States owns almost none of the upstream capacity/refineries for AI, Robotics, to Space, they rely on other countries from Canada to China.

One of the more interesting setups right now is $UAMY, with others like $MP and $USAR looking compelling as well.

Keep in mind that this is a highly speculative sector.

The Setup:

Policy support for critical minerals has accelerated

New long-term strategic agreements as catalyst

Classic VCP (volatility contraction pattern)

Lin

AAPL

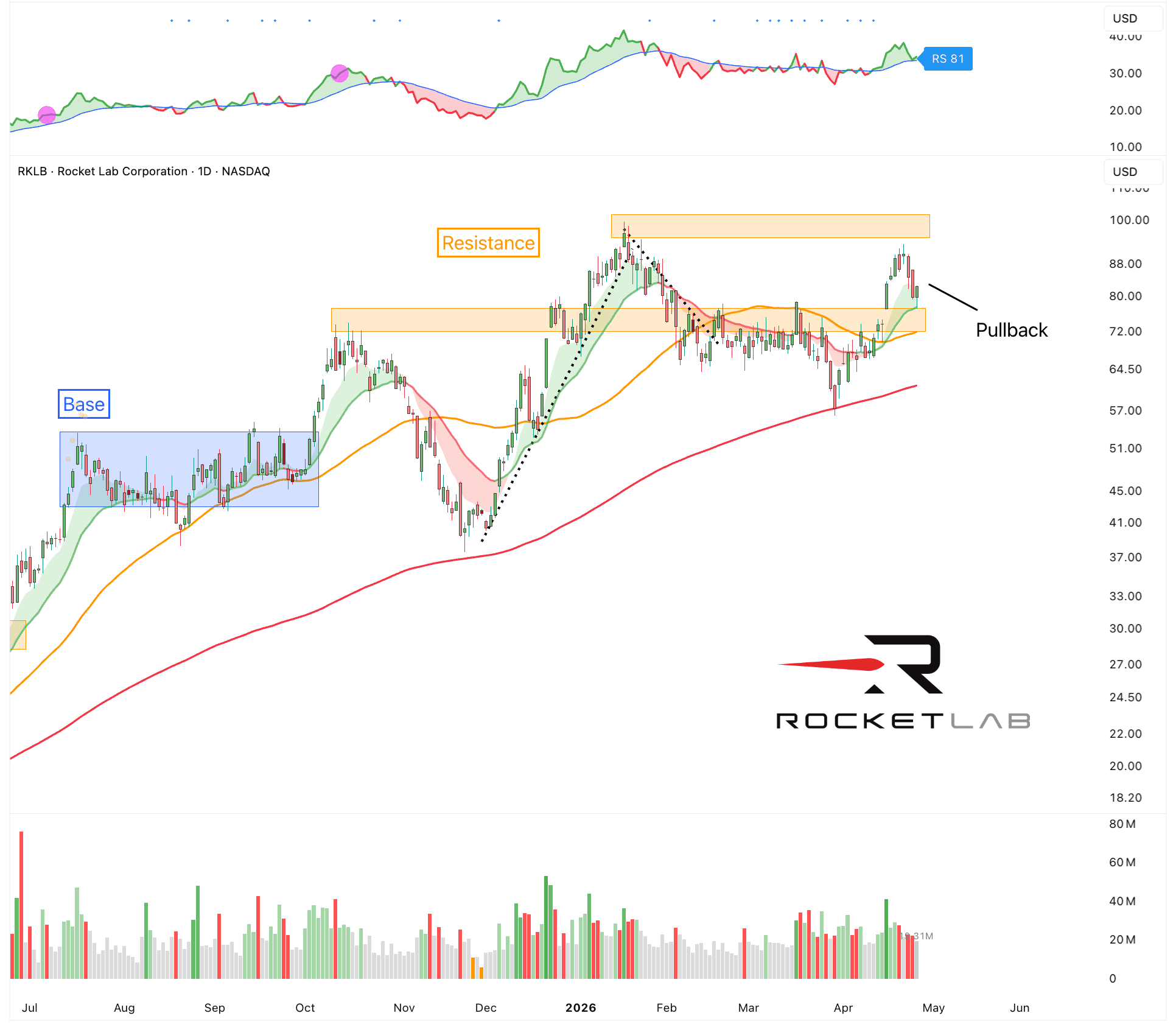

RocketLab $RKLB

RocketLab $RKLB

The space race is on.

There are rumors that SpaceX could IPO at a $1.75T valuation. If true, it would be the largest and most expensive IPO in history. Whether that valuation is justified is a separate debate. But one thing is clear: it would likely be a major positive catalyst for the rest of the space sector. Investors will likely re-rate the whole sector.

And one of the companies that is somewhere close to SpaceX is RocketLab - as I’ve written about at various points. It is one of the few public names with real launch capability.

The Setup:

Re-rating of the whole sector

SpaceX likely in June or July

Potential pullback buy point

Lin

AAPL

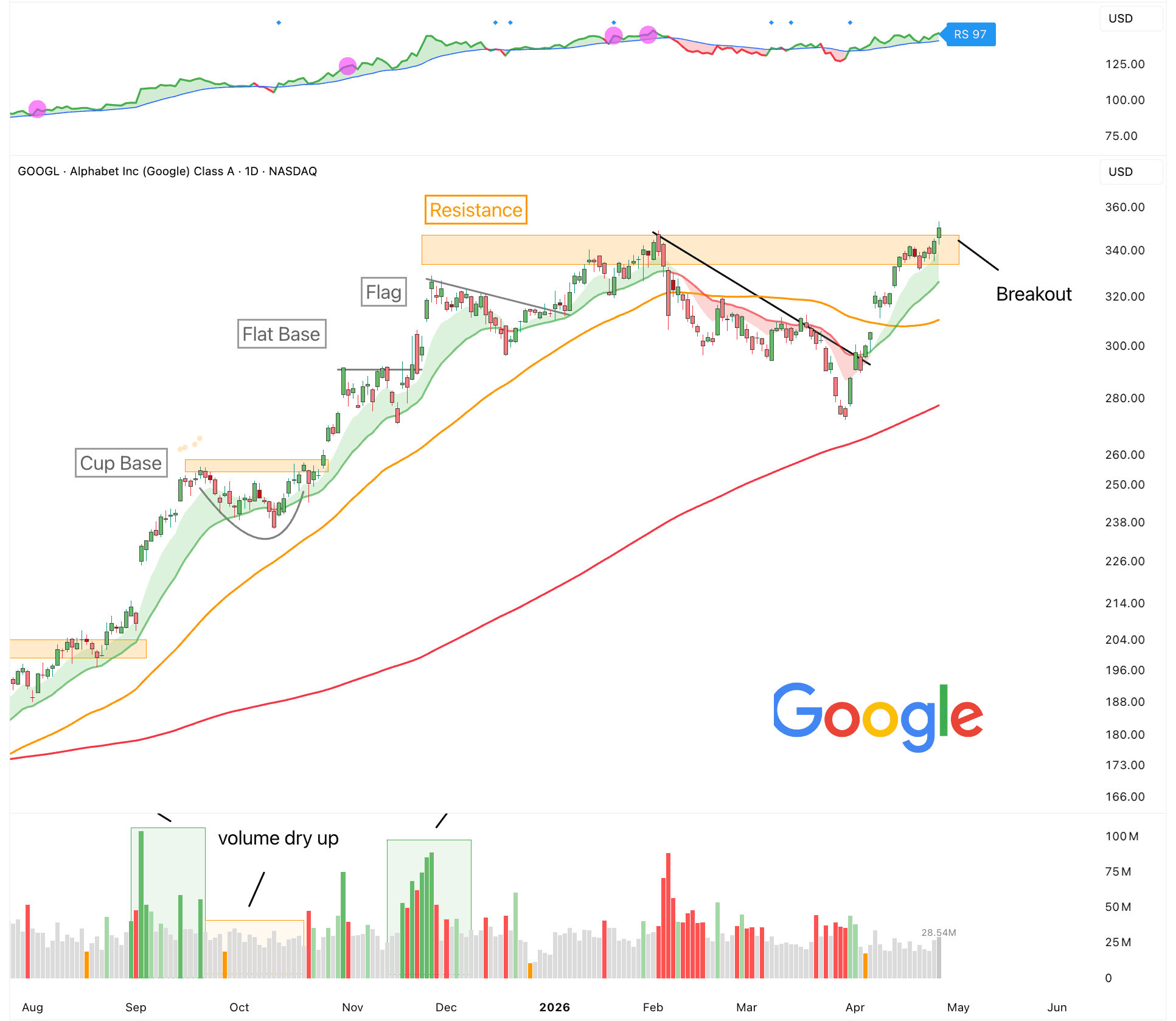

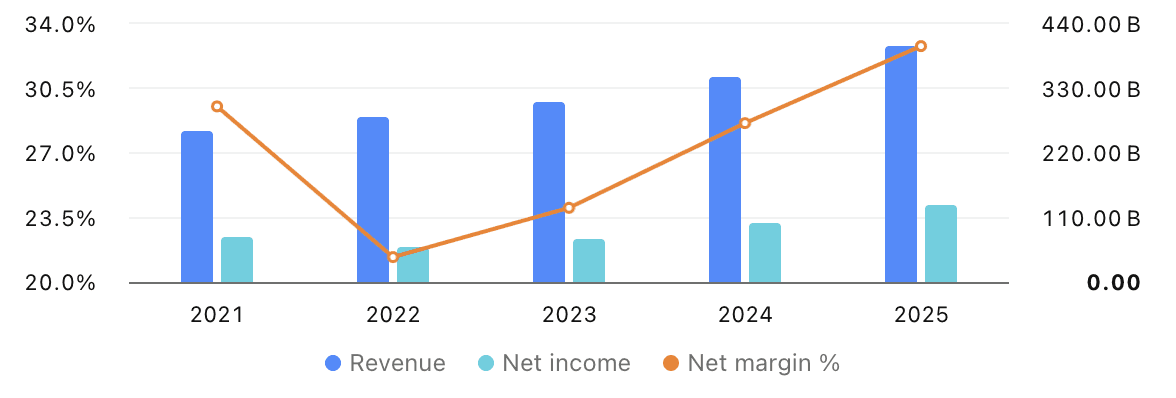

Google $GOOGL

Google $GOOGL

My favorite names of the Mag 7 right now are:

$NVDA, $AMZN, and $GOOGL.

I’ve talked about Nvidia last week and since then it’s up close to 10% and back to new all-time highs.

And like Nvidia, Google continues to be underrated.

It’s the only company in the AI era with a serious AI-chip play + model play + consumer-facing applications.

It has >8 products each serving >1B active users (think Maps, Gmail, Search, YouTube, others).

TPUs are the only at-scale AI-chip deployment besides Nvidia.

Hence, I’m definitely looking to increase my position.

The Setup:

Breakout to new all-time highs

Earnings could the catalyst for the next move higher

Exposure Level

Guidance:

Neutral

0%

100%

Trend Indicator

Long-Term:

Up

Intermediate-Term:

Sideways

Short-Term:

Sideways

Risk Indicators

Volatility:

High

Sentiment:

Neutral

Momentum:

Neutral

Leading Sectors

View All

Energy

Biotech

Fintech

Cybersecurity