Go Back

Lin

Weekly Market Update: The Green Giant

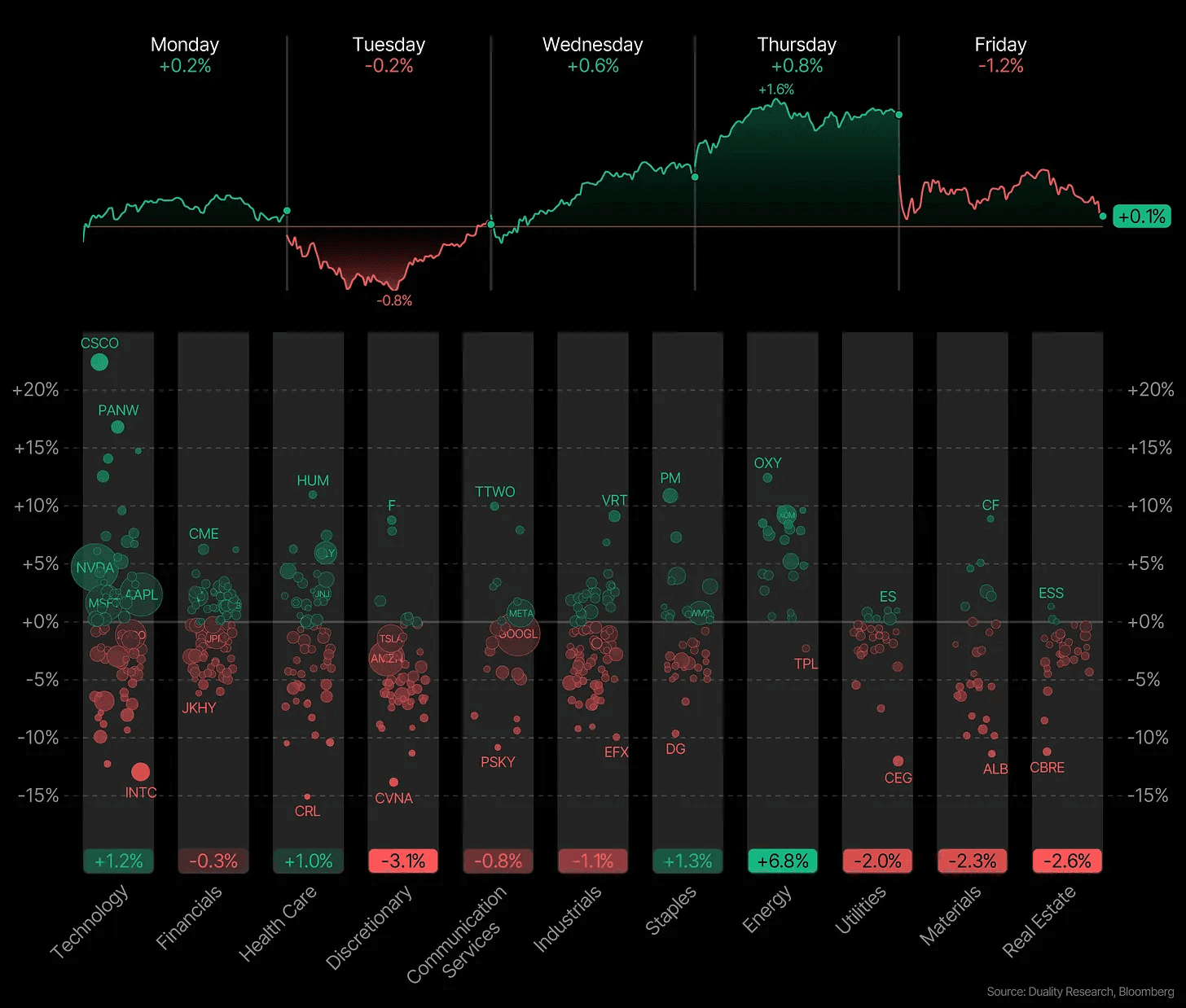

The market hit another all-time high this week.

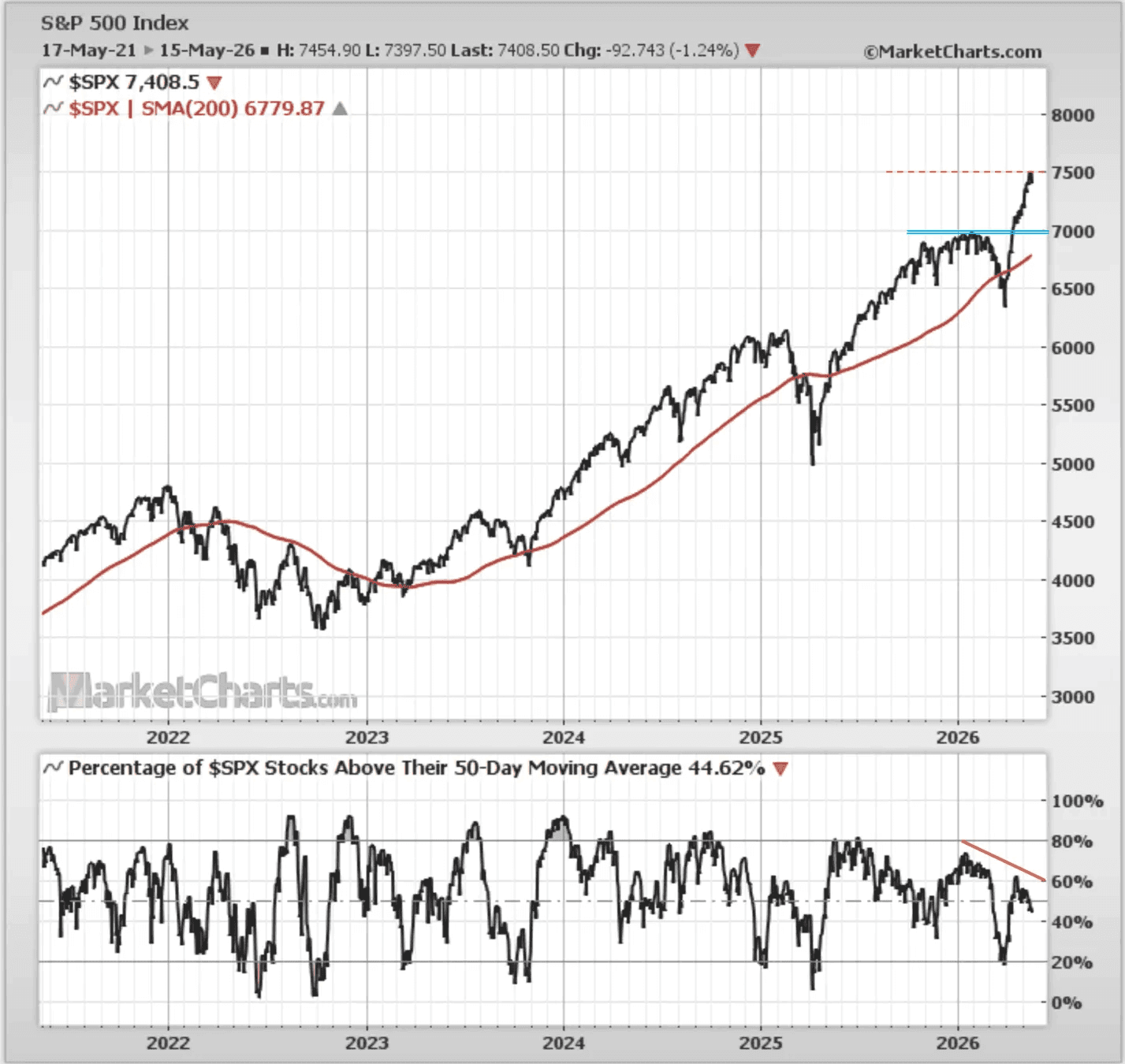

The S&P 500 is now sitting just shy of 7,500, which is a level that would have sounded almost ridiculous not too long ago. But after a huge run, the week ended with a small pause.

And honestly, that is not a bad thing.

A pause after a monster move is normal. Markets do not move in a straight line forever. Even the strongest uptrends need time to cool off. Pullbacks are not signs that the trend is broken. Most of the time, they are what keeps the trend healthy. So a small pause near all-time highs is not something to panic over.

But this week comes down to one name: Nvidia.

Nvidia is no longer just another mega-cap stock. It has become the heartbeat of the AI trade. It sets the tone for semiconductors, data centers, AI infrastructure, power demand, cloud spending, and even the broader market.

If Nvidia delivers like it usually does, and Jensen gives investors what they want to hear, the AI trade can keep pushing higher. But if the reaction disappoints, even slightly, the market will certainly use that as a reason to take a breather.

Either way, a pause here wouldn’t be surprising.

It’s been a near-straight-line trajectory since the lows. And when the market goes straight up, people start to feel like risk has disappeared.

That is where leverage comes in. Leverage rises because confidence rises. Traders start taking bigger positions because the market has been rewarding risk. Hedge funds increase exposure because they do not want to underperform. Retail traders buy more calls and use margin.

The problem is that leverage makes the market more fragile.

When too many everyone is leaning the same way, the market needs everything to keep going right. A lot of the good news is already priced in. It needs earnings to stay strong. It needs guidance to be good. It needs inflation to behave. It needs the Fed to stay friendly. It needs Nvidia and the AI trade to keep delivering. It does not take much to cause a pullback.

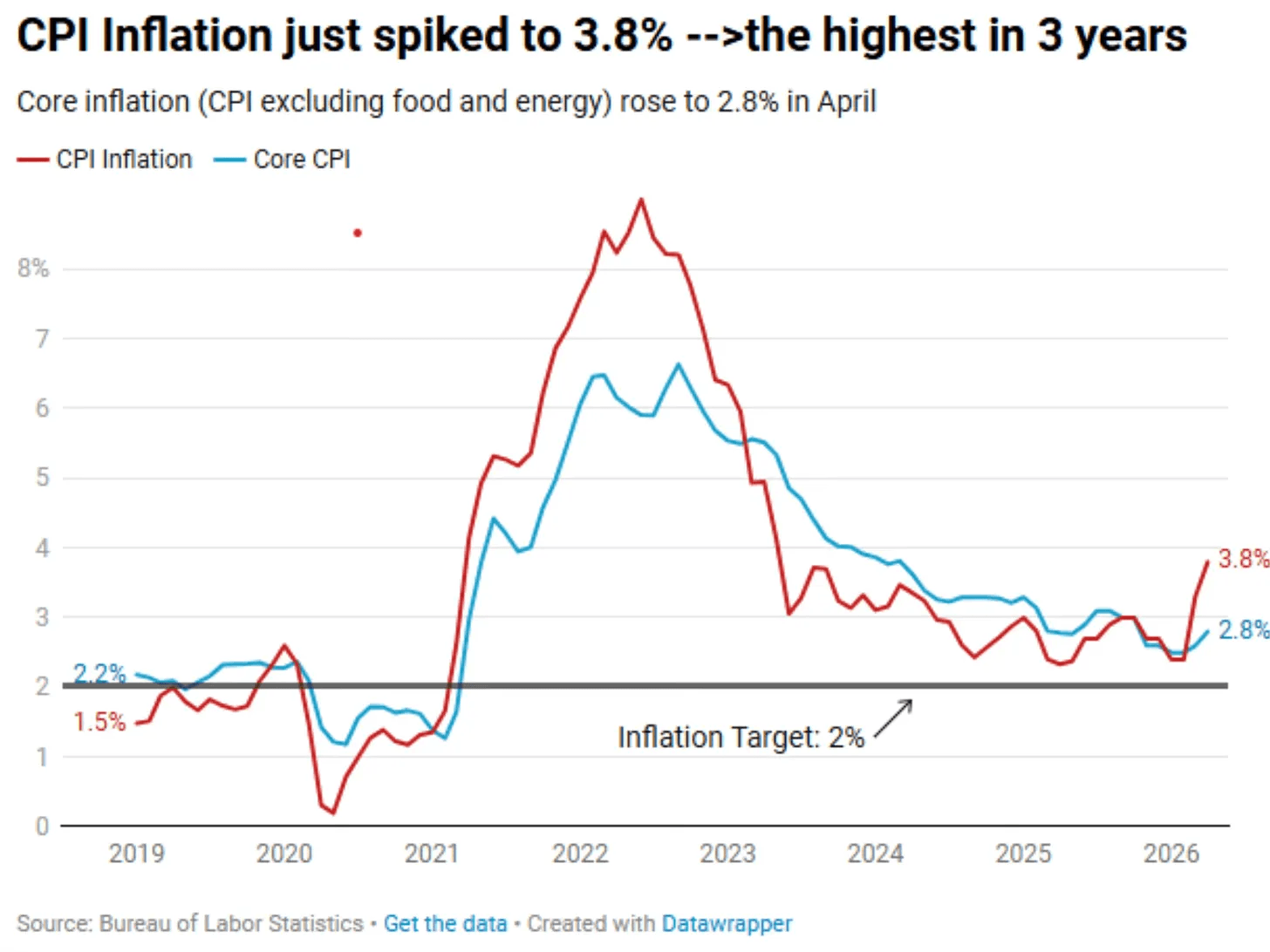

And it this case it was rising inflation and yields.

April CPI came in at 3.8%, the highest reading in 3 years. Core CPI, which strips out food and energy, rose to 2.8%, also coming in above expectations.

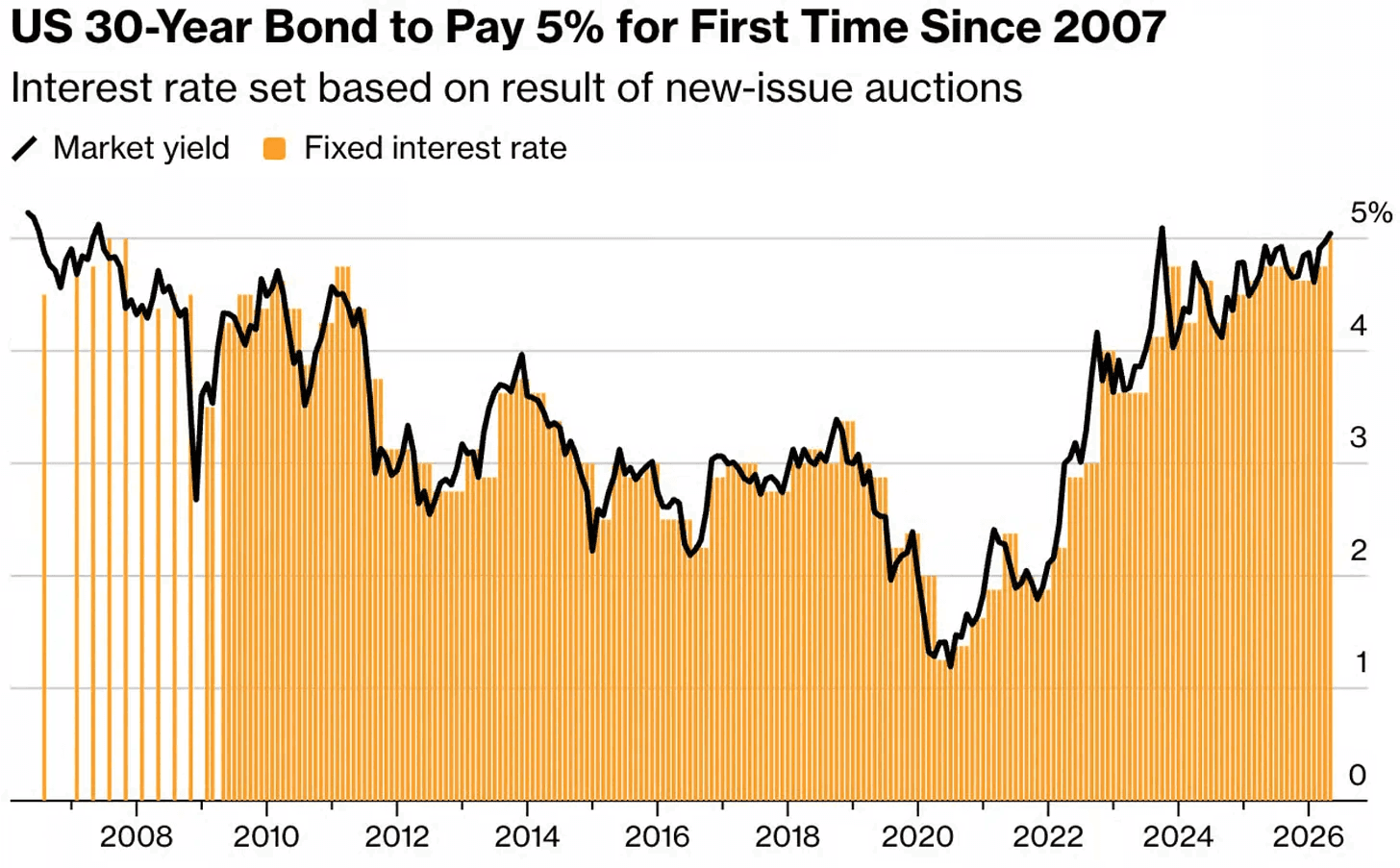

And yields are rising.

The main reason is inflation. April CPI came in hotter than expected, energy prices are up, and core CPI also rose, which tells investors this is not just a short-term gas-price problem. If inflation stays sticky, the Fed has less room to cut rates, and the market has to price in higher rates for longer. That pushes Treasury yields higher.

The second reason is oil and geopolitics. The Iran conflict has pushed energy prices higher and raised fears of supply disruptions, especially around the Strait of Hormuz. Higher oil prices can feed into inflation, transportation costs, company margins, and consumer prices. So the bond market starts pricing in the risk that inflation may not cool as smoothly as investors hoped.

The third reason is supply. The U.S. government has to issue a lot of debt, and when there is more debt supply, investors often demand a higher yield to absorb it. A recent 30-year Treasury auction cleared above 5%, which showed that buyers wanted more return before stepping in.

Higher yields are a problem for markets because they make everything else look more expensive. When Treasuries pay 4.5% to 5%, investors no longer feel forced to chase stocks at any price. They can now earn a solid return in something much safer.

Higher yields also hurt valuations because future profits are worth less today, which is especially painful for growth stocks, AI stocks, software names, and other companies priced on big earnings far into the future.

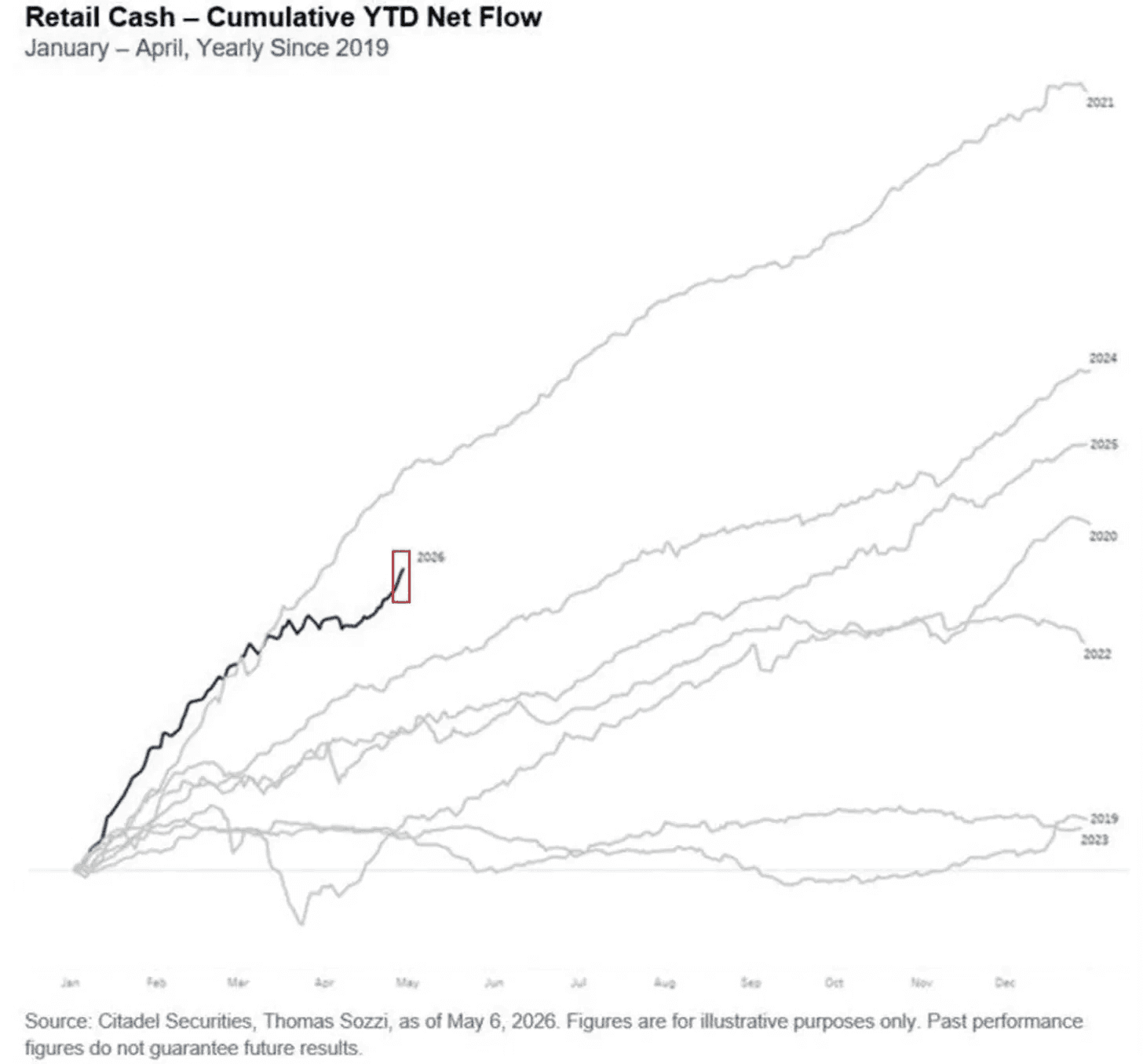

Retail investors have been buying stocks so aggressively this year that the total money flowing into equities is higher than almost every other year over the last 7 years. The only year with stronger retail buying was 2021, when the market was in a huge post-Covid boom with meme stocks, stimulus money, options trading, and massive risk appetite.

Investors are very bullish again, and their buying is what’s pushed the market higher.

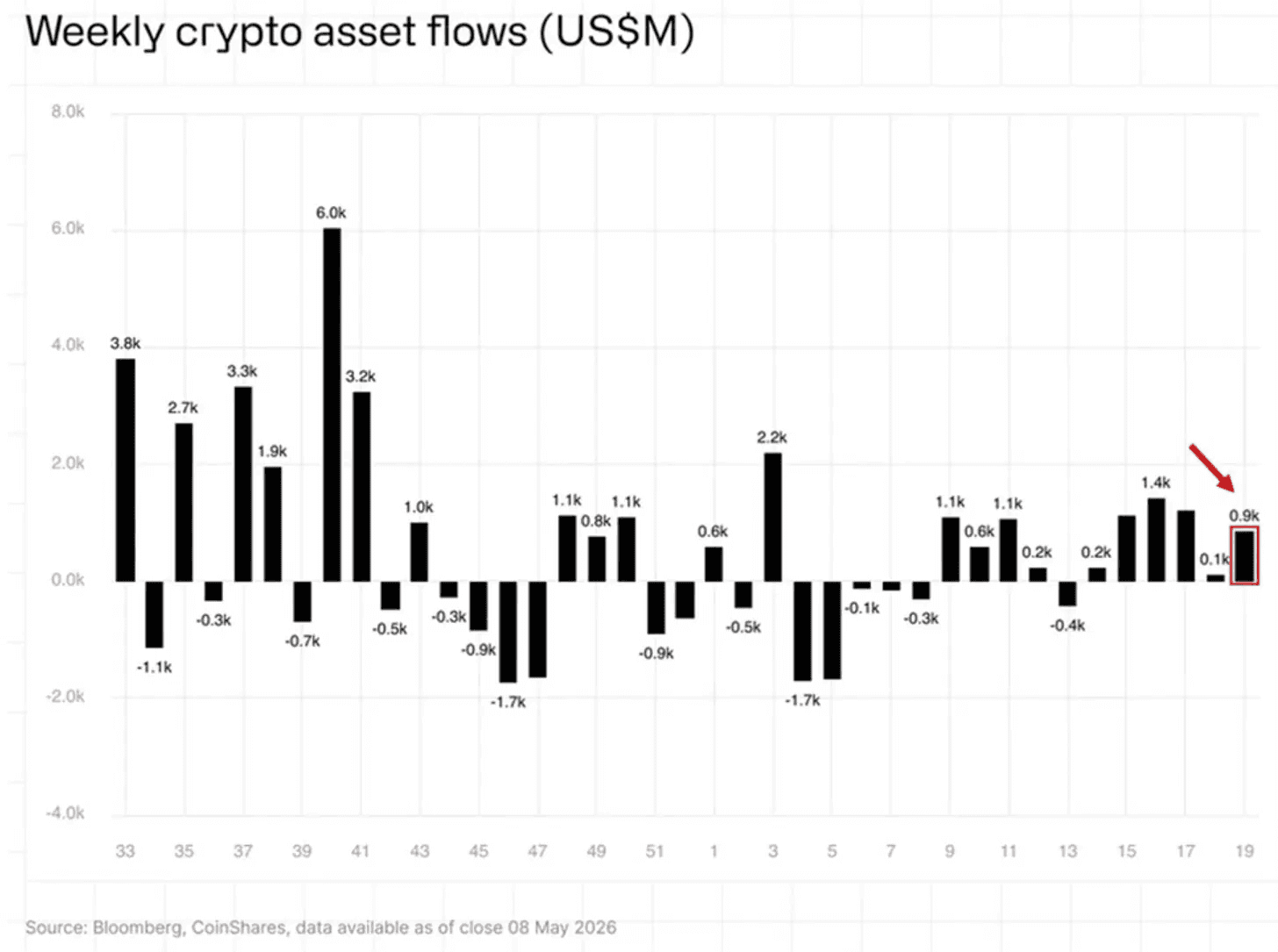

Crypto is telling the same story. Funds posted $858 million in inflows last week, marking the 6th straight week of money coming in. Bitcoin alone has pulled in $4.9 billion year to date. And crypto is one of the best signs of risk appetite. Because when investors are fearful, they would not rush into Bitcoin, crypto funds, or high-beta digital asset names. And this is not just one good week. It’s been 6 straight weeks of inflows.

Speaking of risk.

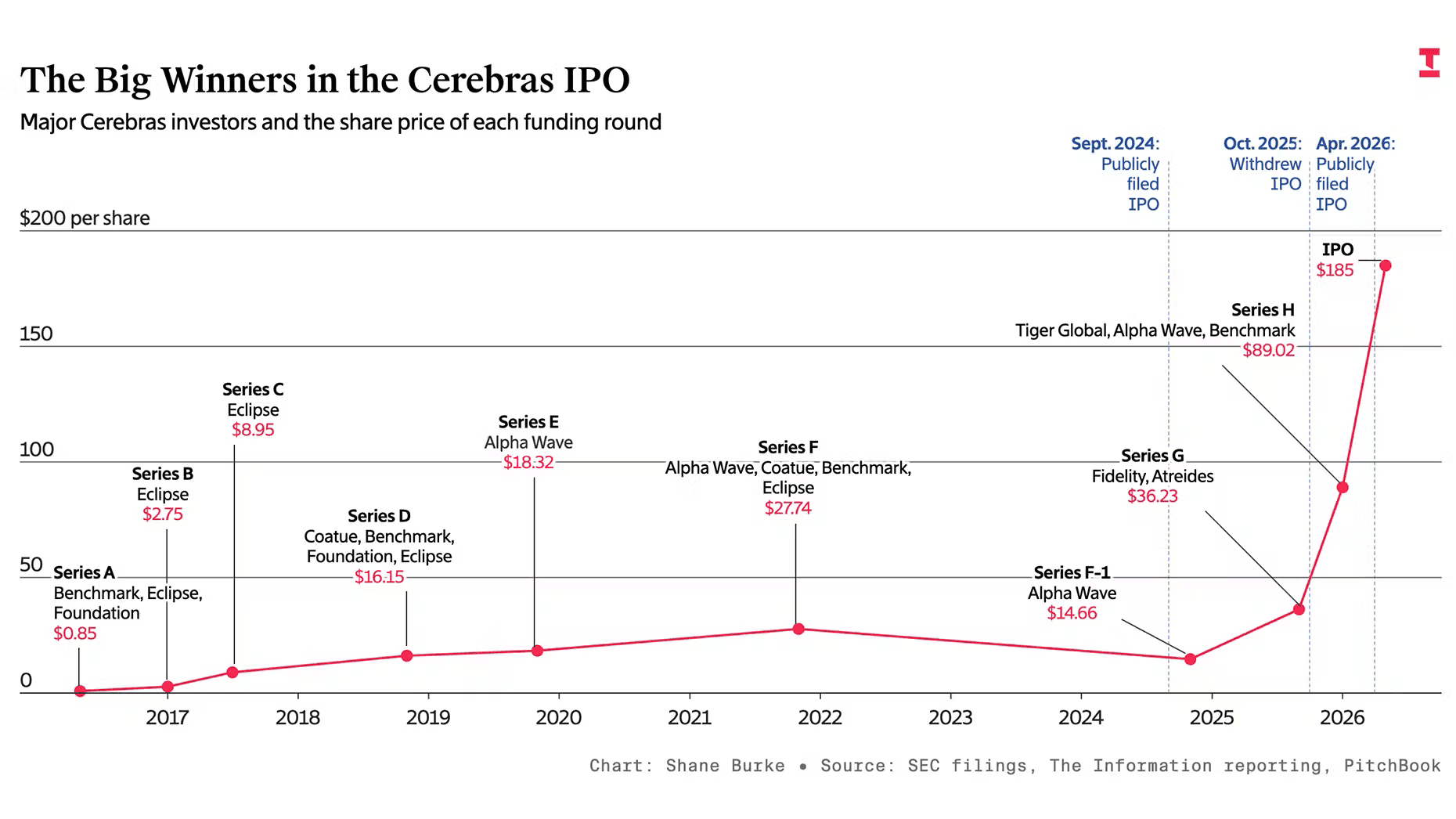

The long-awaited Cerebras $CBRS IPO finally took place last week.

Cerebras builds huge specialized processors for AI training and inference. Instead of making a normal-sized GPU like Nvidia, Cerebras is known for its wafer-scale chip, basically a massive chip built from an entire silicon wafer. The idea is that by making 1 giant AI processor, they can move data faster and run AI models extremely quickly.

The demand for this IPO was staggering.

Initial reports suggested the IPO would price somewhere between $115 and $125. From there, demand pushed the price higher and higher until the stock ultimately opened at $350 and briefly peaked around $385.

But the opening price of $350 per share, a $100B valuation, is anything but cheap. It would have been much more interesting at the initial target valuation of $26.6B, with shares in the $115 to $125 range. The big winners, for now, were the institutions.

Cerebras will remain a major focus for me. New AI IPOs in an AI-driven bull market can be extremely lucrative. Just look at CoreWeave $CRWV last year or Ambiq Micro $AMBQ this year. I’ll be tracking all the new IPOs here.

There usually isn’t a major rush to buy an IPO right away, especially when the valuation is this stretched.

But one thing is clear: the demand for good companies to IPO is off the charts.

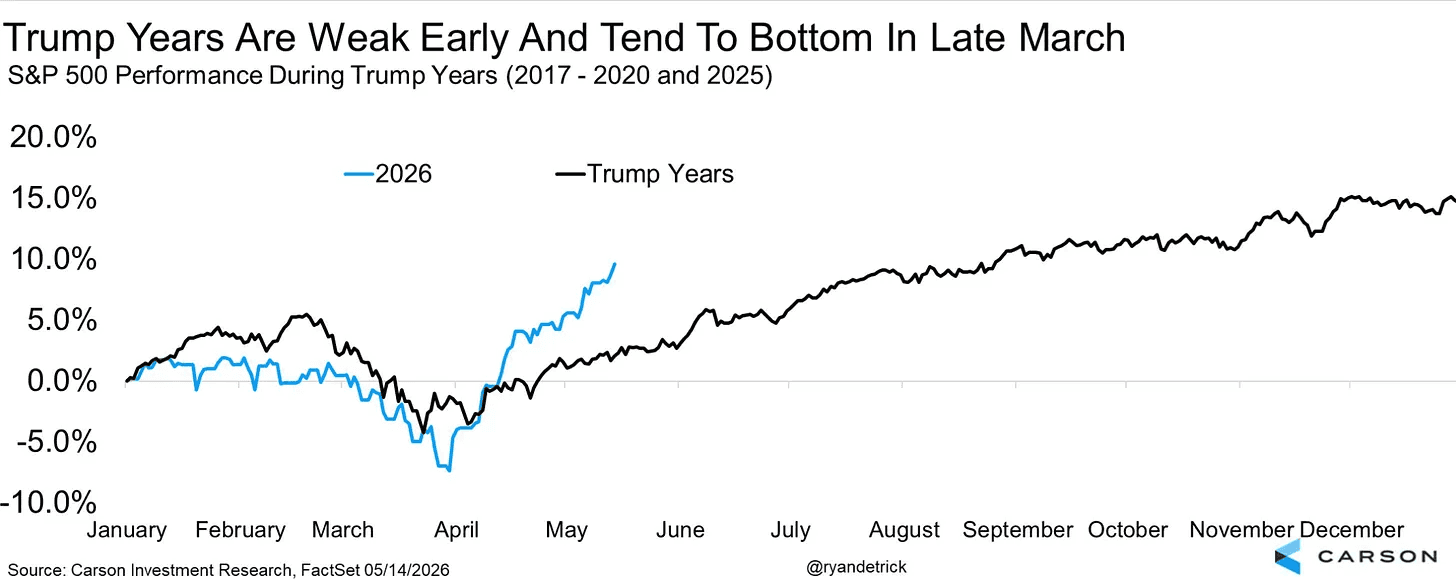

So far this year has followed the typical Trump path.

The market struggled early, bottomed hard around April, and then ripped higher into May. In fact, we have now run ahead of the average Trump-year pattern. It would not be surprising to see the market pause for a while. And if the historical Trump-year pattern continues, the second half of the year should be very positive.

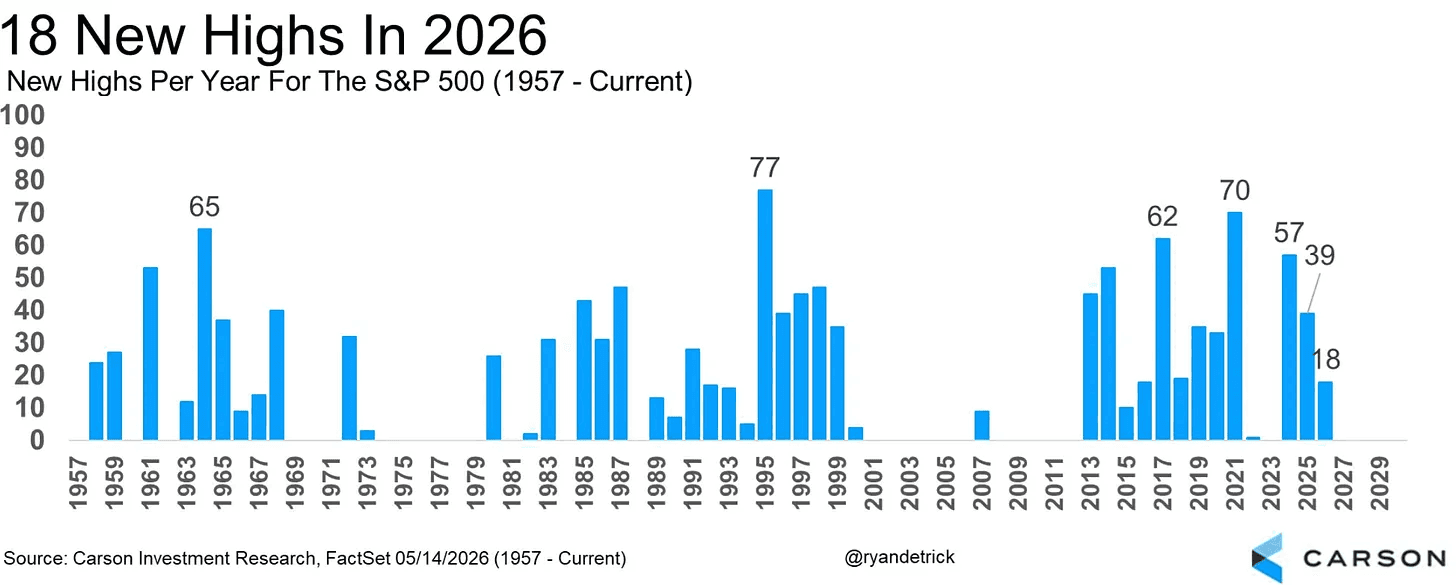

The market has only made 18 new highs this year. That may sound like a lot because every new high gets treated like some major warning sign, but when you look at history, it is actually below the average for a strong uptrend. In real bull markets, new highs are normal. That is what bull markets do.

Usually, in a strong uptrend, you see 30+ new highs in a year. Sometimes much more. So 18 new highs does not look like some extreme euphoric melt-up by itself. It looks pretty average.

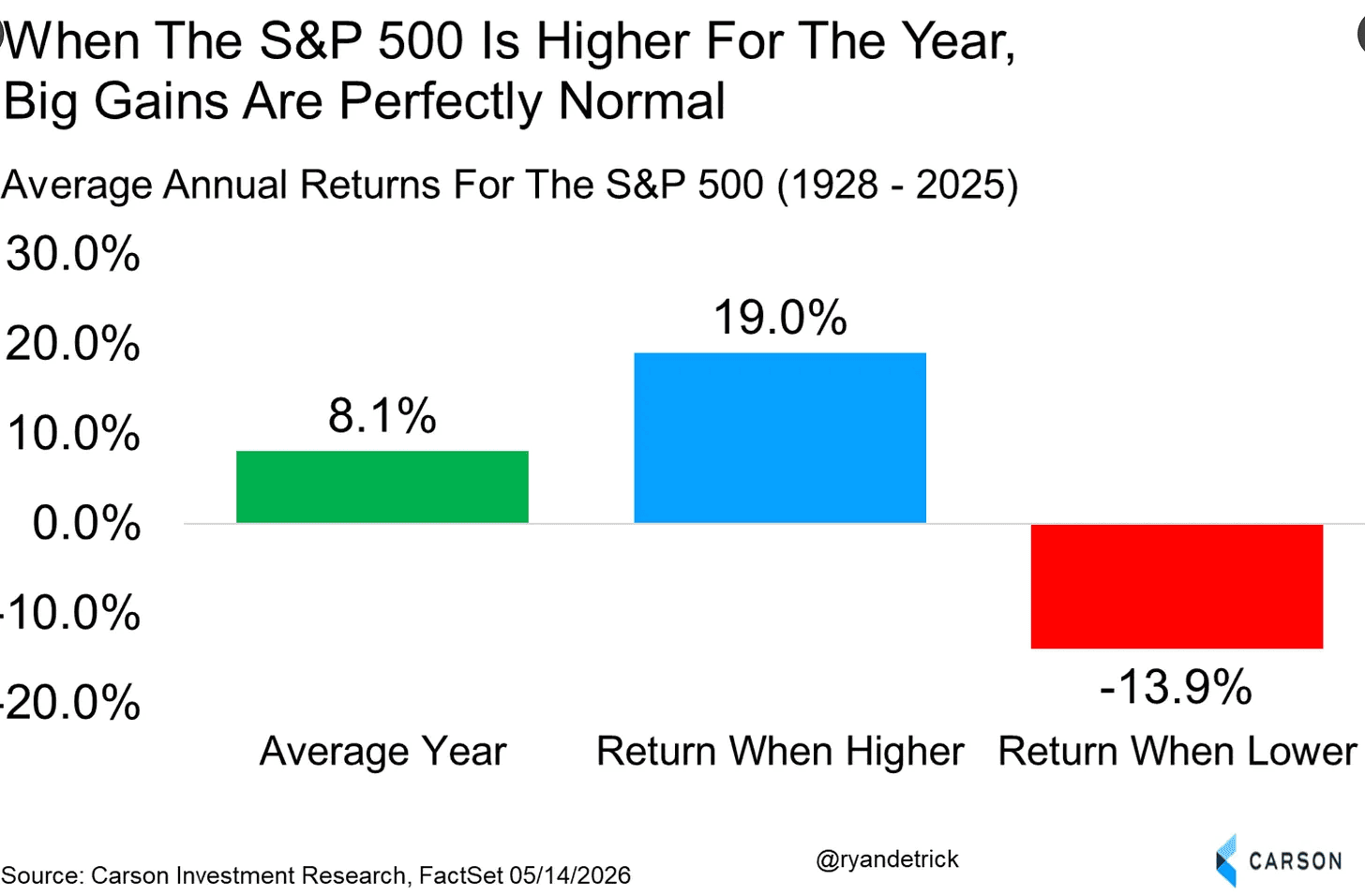

Rallies are usually much stronger than people think.

Everyone loves to quote the market’s average return of 8%. But that number is misleading because it blends everything together. It includes great years, flat years, weak years, bear markets, and crashes. It is the long-term average, not what a normal positive year looks like.

The average up year is closer to +19%. The average down is around -14%.

So even after this impressive run, we are technically still below the average positive year.

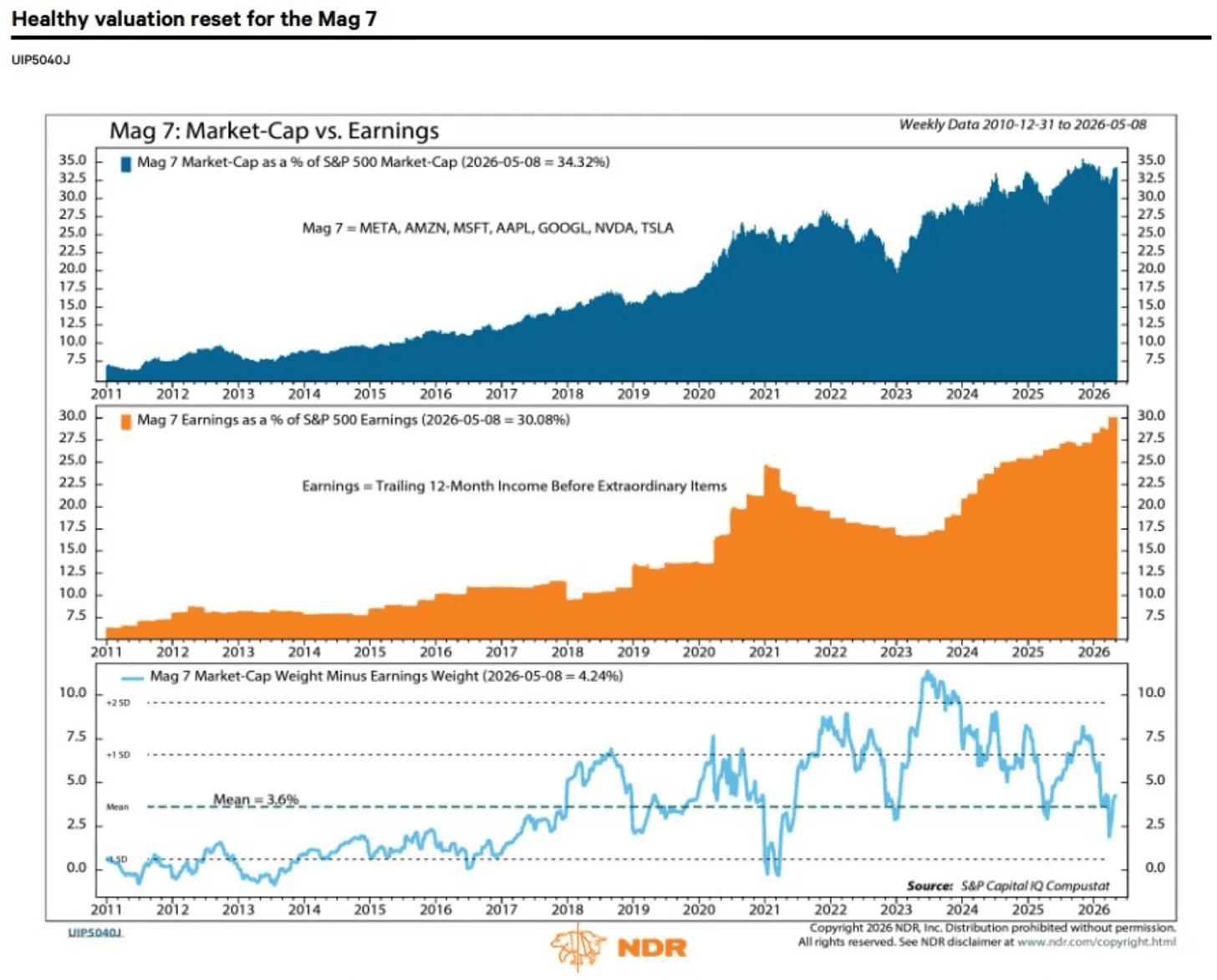

And one big driver of this bull market are the Mag 7.

Since the March 30 low, the Mag 7 is up 27.7%. The cap-weighted S&P 500 is up 17.7%. The equal-weighted S&P 500 is up just 7.9%. And despite the massive run, the Mag 7 is not stretched on valuation in the way many assume.

And there is one Mag 7 earnings report left.

Overall, this is still a bull market until proven otherwise.

Yes, the market is extended. Yes, yields need to be watched closely. And yes, this was the first week where the market started to show a little bit of hesitation after a near-straight-line move higher.

But a pause or small selloff after a run like this is not something to panic over. The bigger picture has not changed. Pullbacks, pauses, and consolidations are part of healthy uptrends. This week comes down to Nvidia and the man in the leather jacket, Jensen Huang.

Previous Updates

View All

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging

- Market Update: A Change of Character

- Market Update: The Next Quantum Leap

- A Few Portfolio Changes

- Weekly Market Update: New Month, New Opportunities

- Market Update: Compute, Compute, Compute

- Weekly Market Update: The Bulls March On