Go Back

Lin

Weekly Market Update: An Unprecedented Rally

The past few weeks have been unprecedented. The speed of this market recovery has been truly remarkable.

At the same time, the Iran war continues to cool off, and the major indices are responding accordingly. Less uncertainty gives markets room to move higher, and that is exactly what we’ve discussed.

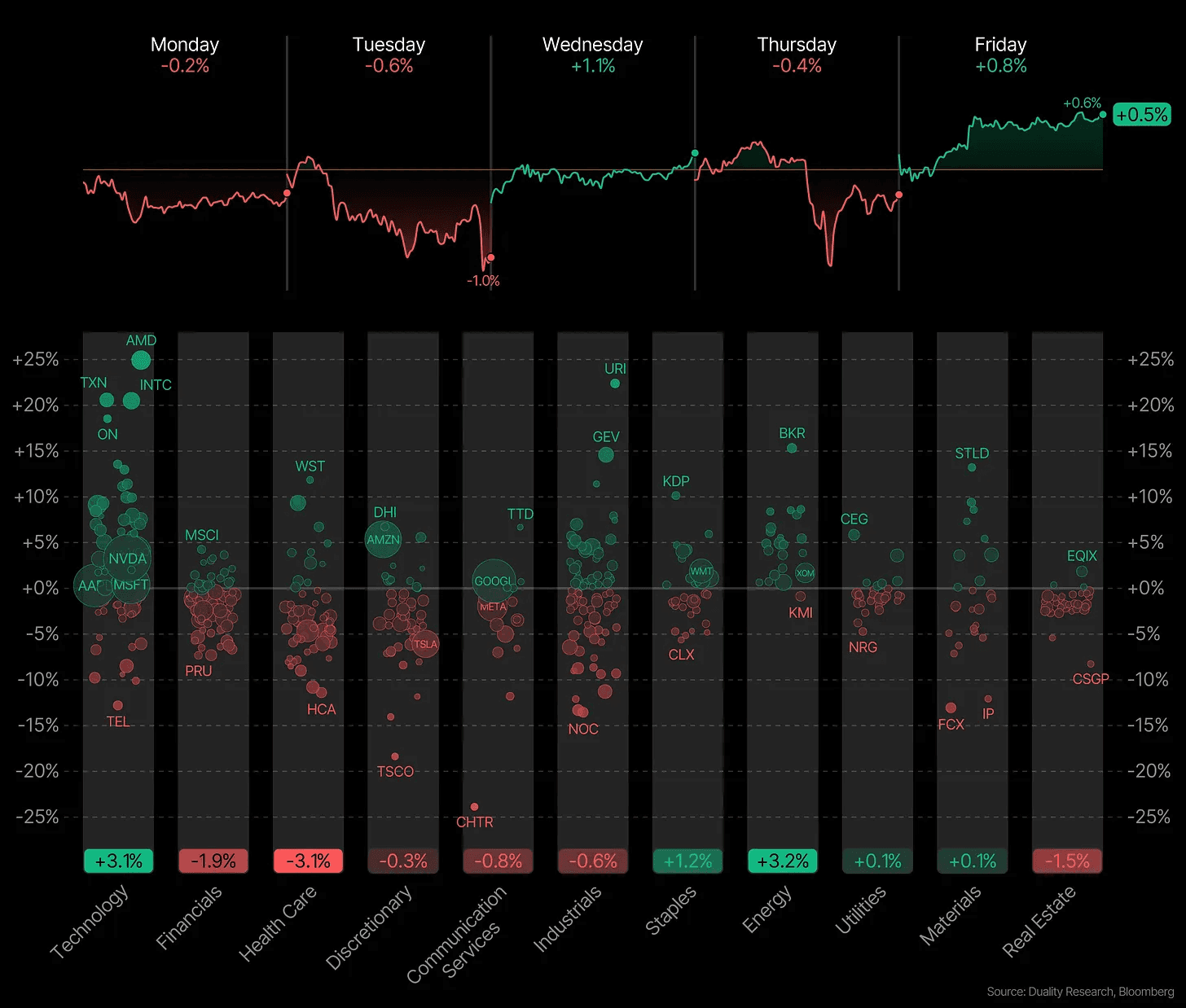

Right now, there are setups everywhere. This is an supportive market with more opportunities than you could take, and that is a good problem to have. But it’s important to remember that you are not going to catch every move. No one does. When dozens of stocks are breaking out and running at the same time, some will move without you. That is part of the game. Chasing everything usually leads to frustration.

Your job is not to catch every stock. Your job is to capitalize on the opportunities that fit your process, your portfolio, and your risk tolerance. There will always be another stock, another breakout, and another chance. What matters is making the most of the opportunities in front of you now.

Stocks are driven mainly by 2 things: earnings and sentiment.

Earnings are what give a business its real value over time. They show whether a company is growing, becoming more profitable, gaining market share, and building something durable. In the long run, stock prices usually follow the direction of earnings because eventually fundamentals matter.

Sentiment, on the other hand, determines how much investors are willing to pay for those earnings today. It reflects confidence, fear, optimism, pessimism, positioning, momentum, and expectations about the future. Sentiment can push prices far above fair value when people get excited, and far below fair value when fear takes over.

That is why markets often seem irrational in the short term. Stocks can rally during negative headlines if investors were already expecting something worse. They can also fall after strong earnings reports if expectations had become too high going in. The reaction is often less about the news itself and more about whether reality was better or worse than what people had already priced in.

In the long run, earnings usually win. In the short run, sentiment often takes over.

The software selloff is a perfect example. Many investors worried AI would destroy traditional software moats, compress pricing, or turn products into commodities. So many software names sold off even before the actual impact was clear. It did not matter how strong or durable the individual businesses were. When fear hits a sector, correlations often move toward 1. Investors stop focusing on differences between winners and losers and start selling the whole group. Sentiment became the main driver.

That is why I emphasize the importance of being in leading sectors and leading stocks, not the opposite.

Great investors understand both forces. They track fundamentals, but they also respect psychology, positioning, fear, greed, and momentum.

Right now, earnings in many areas remain resilient, while sentiment has rebounded from skepticism and fear. That combination is what triggered this strong rally.

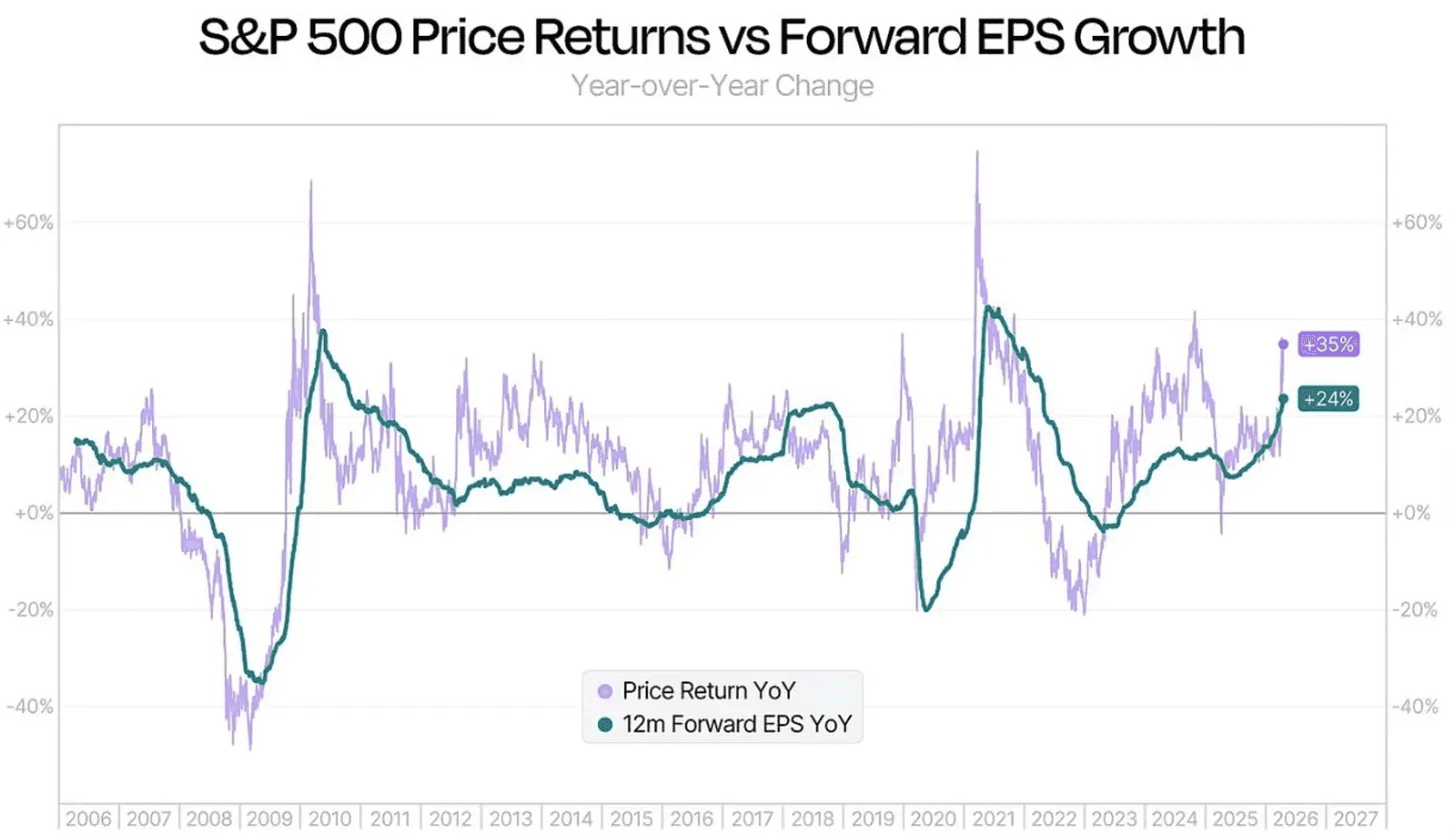

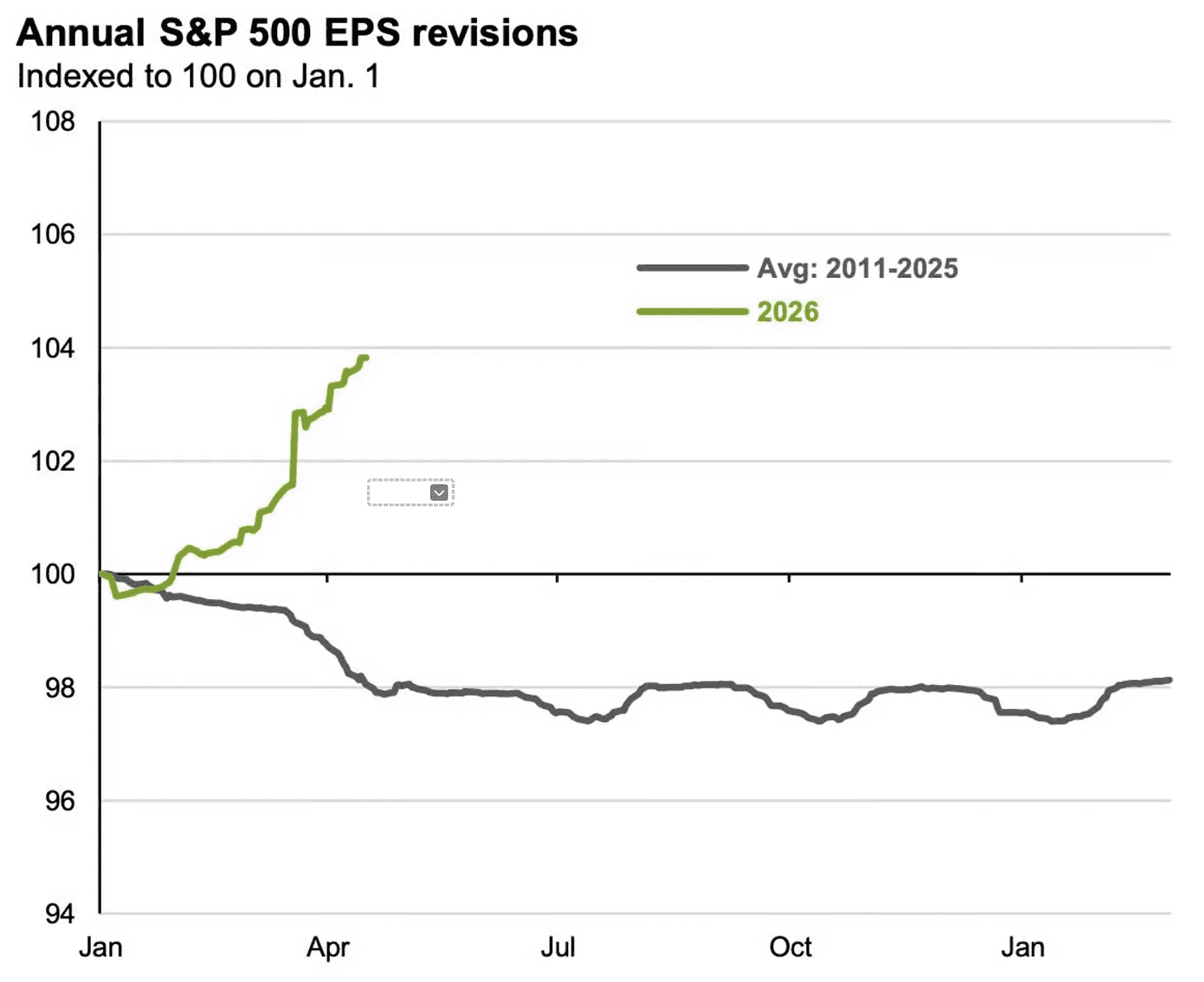

Over the past 15 years, analysts have usually revised EPS estimates lower by around 2% between January and April. That has been the normal pattern. Expectations often begin the year too high, then get trimmed as reality sets in.

But this year has looked completely different.

Instead of cutting numbers, analysts have been raising forecasts for every single quarter of 2026.

That is a major reason stocks are back at record highs.

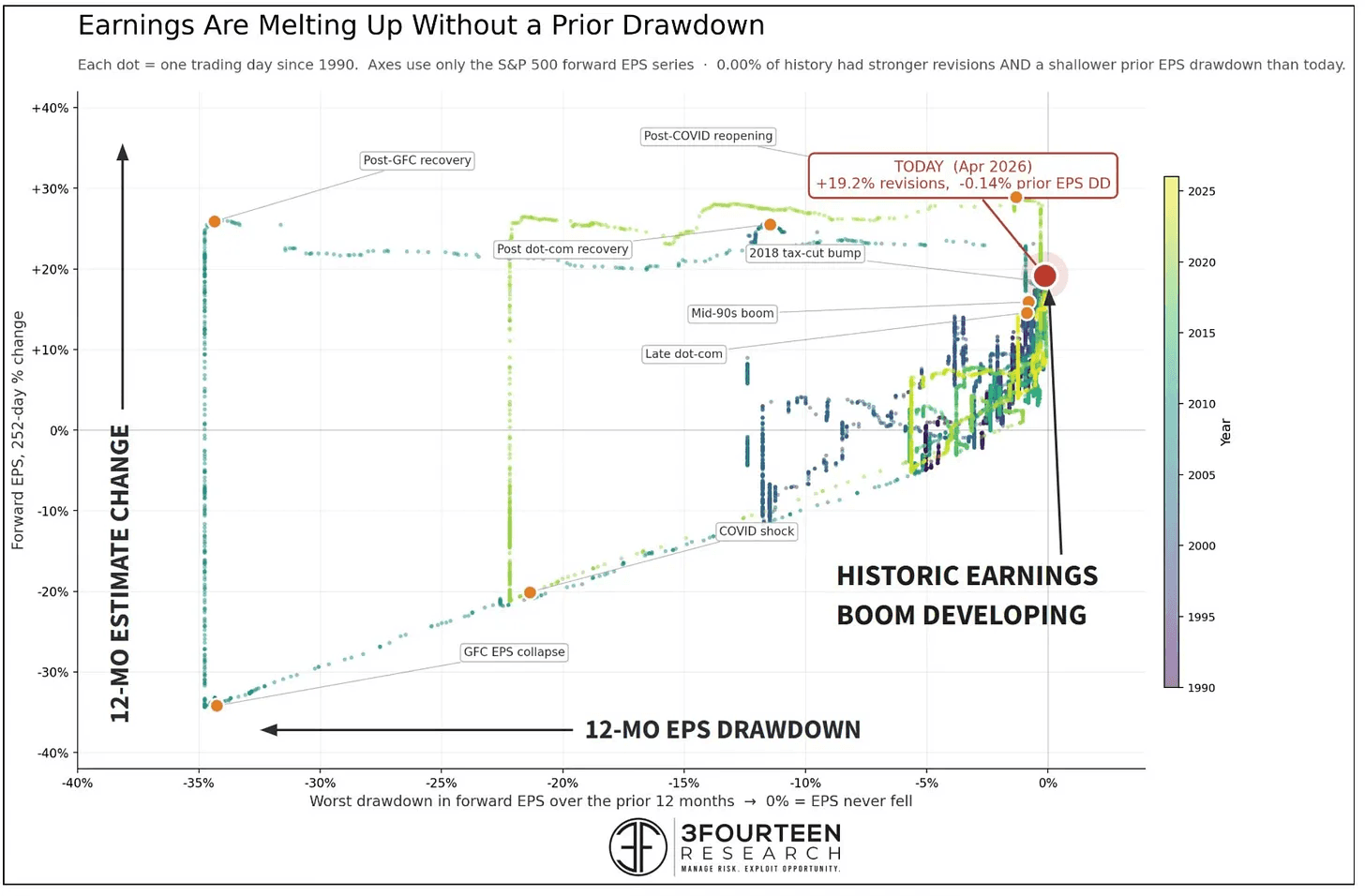

Interestingly, forward EPS is rising faster than it did during the mid 1990s boom or even the late dot-com era. Those were some of the strongest profit expansion periods in modern market history, yet the current pace is now competing with, or surpassing, them.

That kind of melt-up in profits, without a recessionary washout beforehand, is extremely rare and arguably close to unprecedented in modern market history.

This is the AI boom in real time.

If you think the market is wrong for going higher, start by checking the earnings backdrop. It is easy to argue with price, but it is much harder to argue with rising profits.

Yes, over time price often moves ahead of earnings and tries to discount what is coming next. But right now, this is not just a story of hope or speculation. Earnings are growing significantly, forward estimates continue to move higher, and now investors who stayed defensive are beginning to come off the sidelines and chase performance.

And now institutional chase appears to be underway.

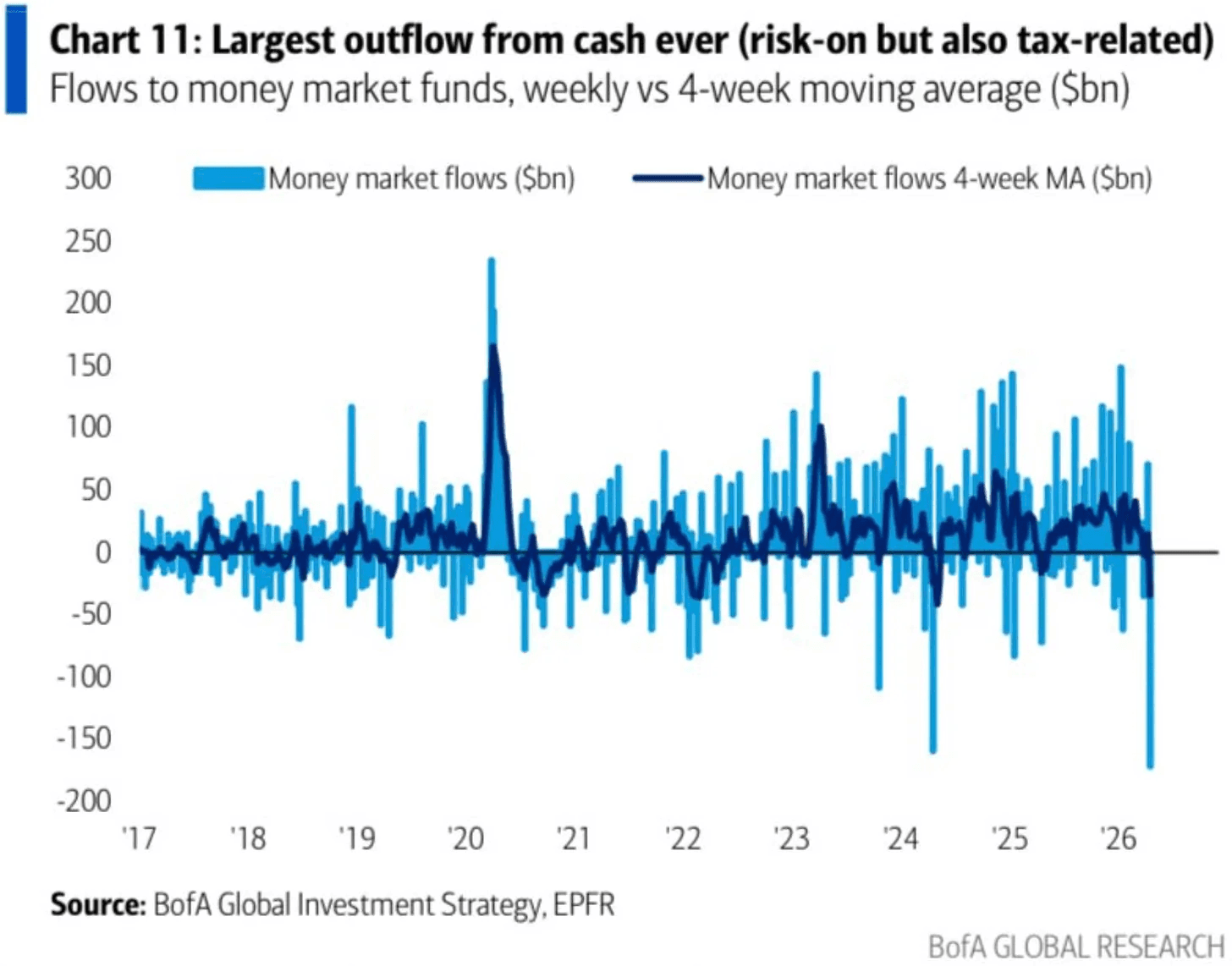

Money market funds reportedly saw roughly $172 billion in outflows last week, the largest weekly drawdown ever recorded. That is more than 320% above the average weekly April outflow of the past 4 years. Some of that capital likely rotated into equities, bonds, gold, and crypto.

Cash that was sitting safely on the sidelines is starting to move back into risk assets at a historic pace. When large pools of idle money begin reallocating after a period of caution, trends can feed on themselves.

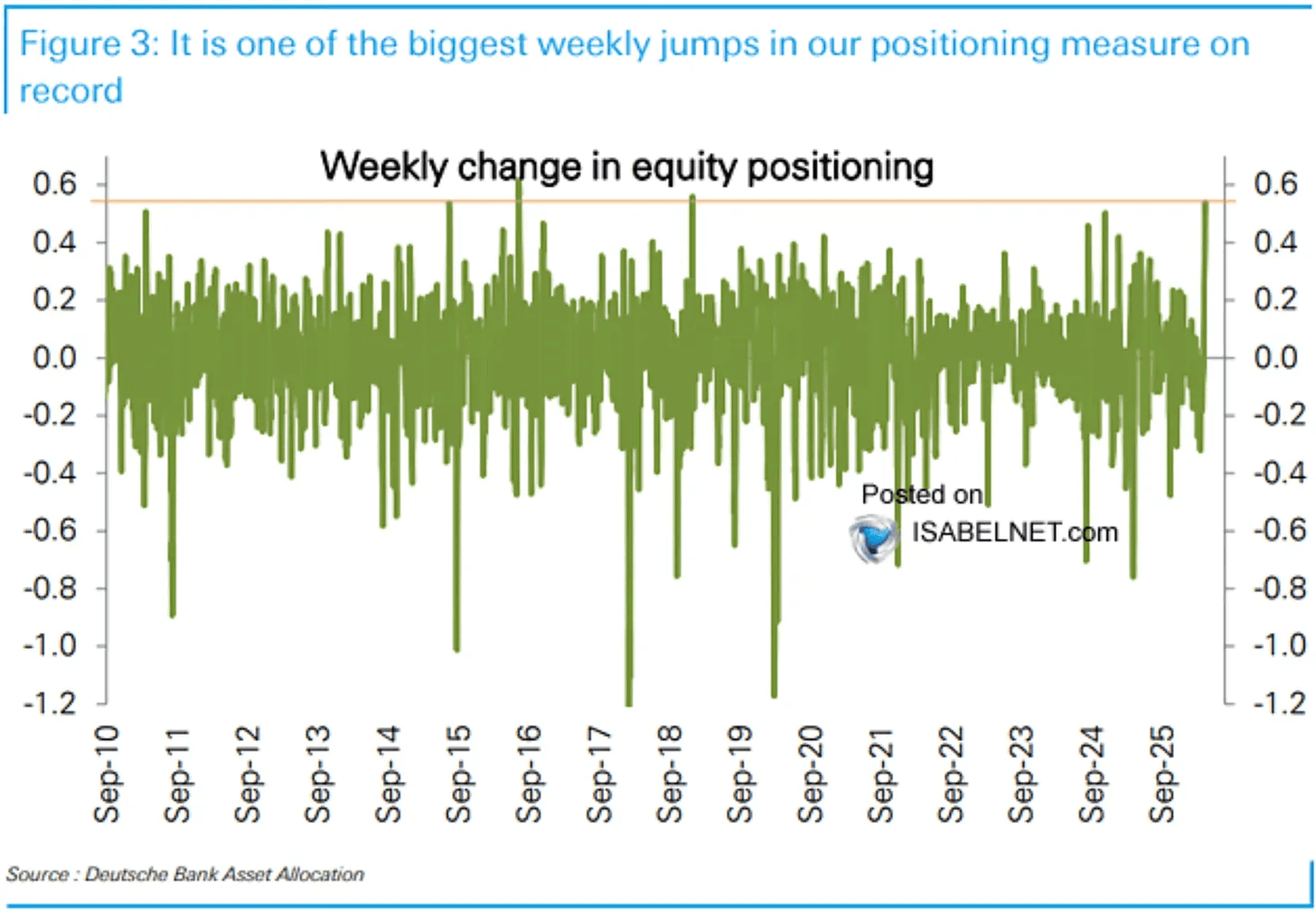

The FOMO is starting to show up in the positioning data as well.

This week saw one of the largest single-week jumps in equity positioning ever recorded. Moves like that usually do not come from slow, methodical capital allocation or carefully planned portfolio rebalancing. They tend to happen when investors feel pressure to get involved quickly.

That is the psychology of FOMO. Investors watch prices keep rising, and begin to worry more about missing the upside than protecting against downside risk.

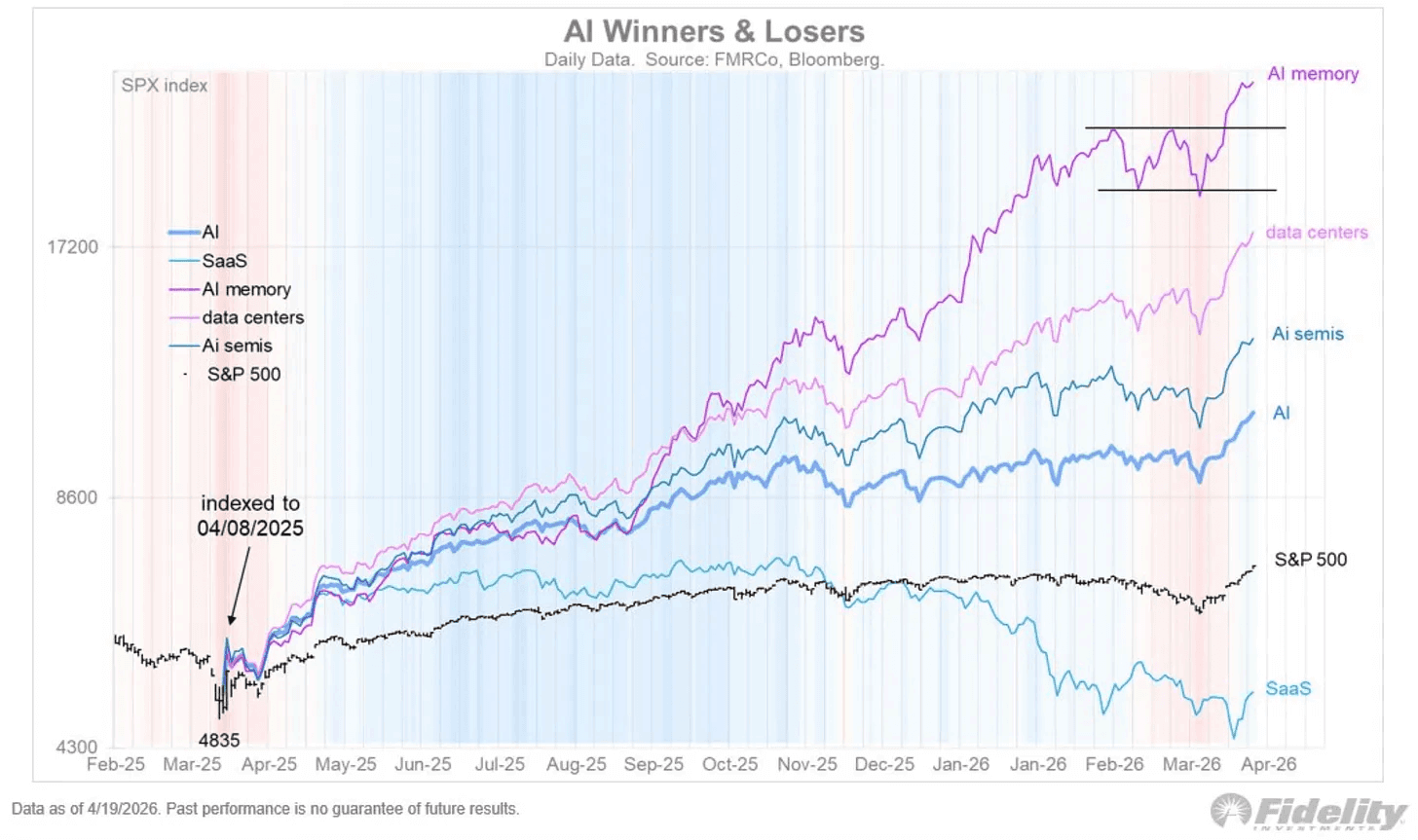

Since the war began, the market has made its preferences very clear.

AI continues to be the clear winners, while most other areas have lagged or moved lower. That alone tells you a lot about where money wants to be positioned right now.

Meanwhile, traditional defensive assets have underperformed materially. Gold is down 13.5% relative to the S&P 500, while Silver is down 21% relative to the index.

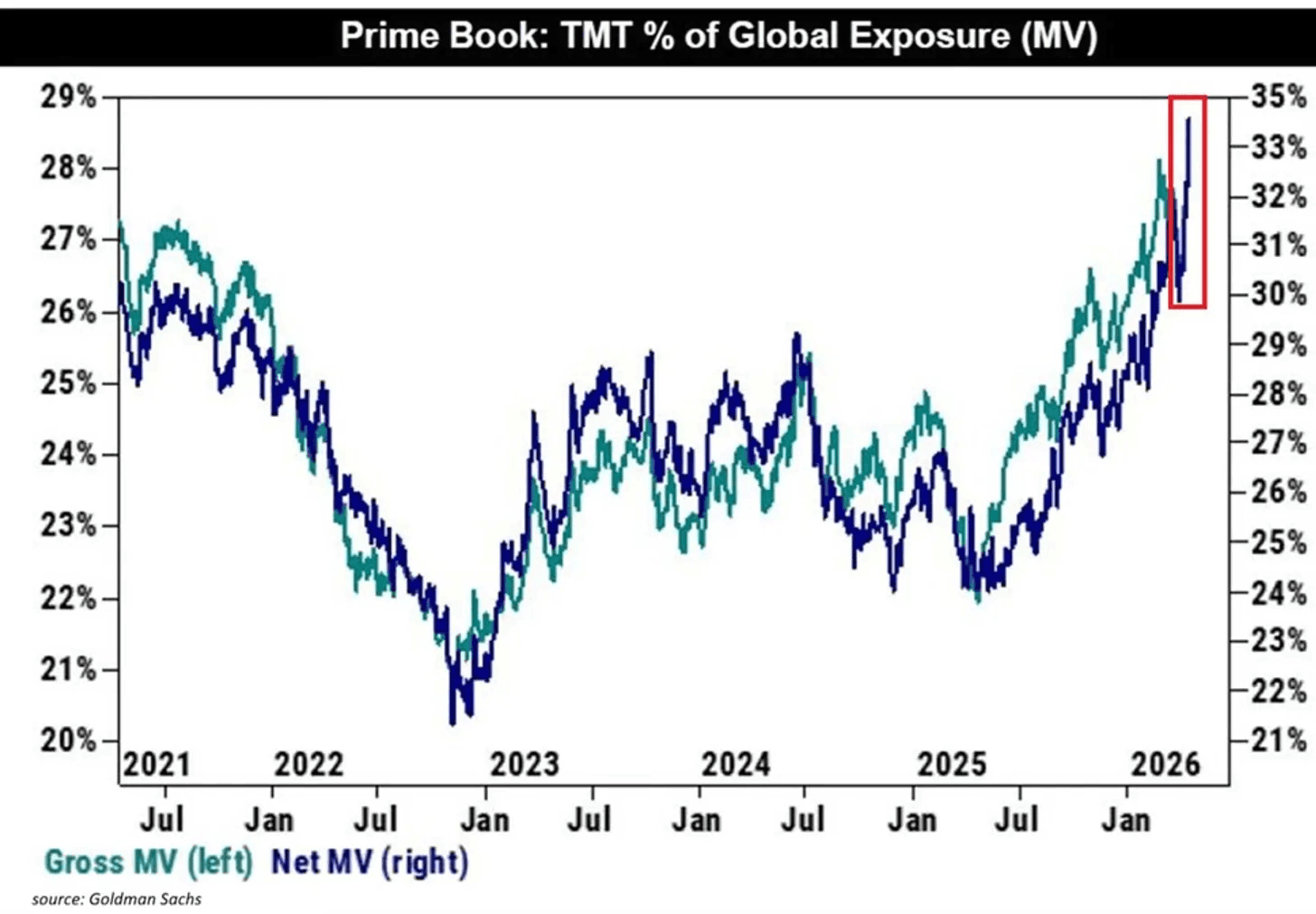

Here is one of the most interesting things happening beneath the surface in tech right now.

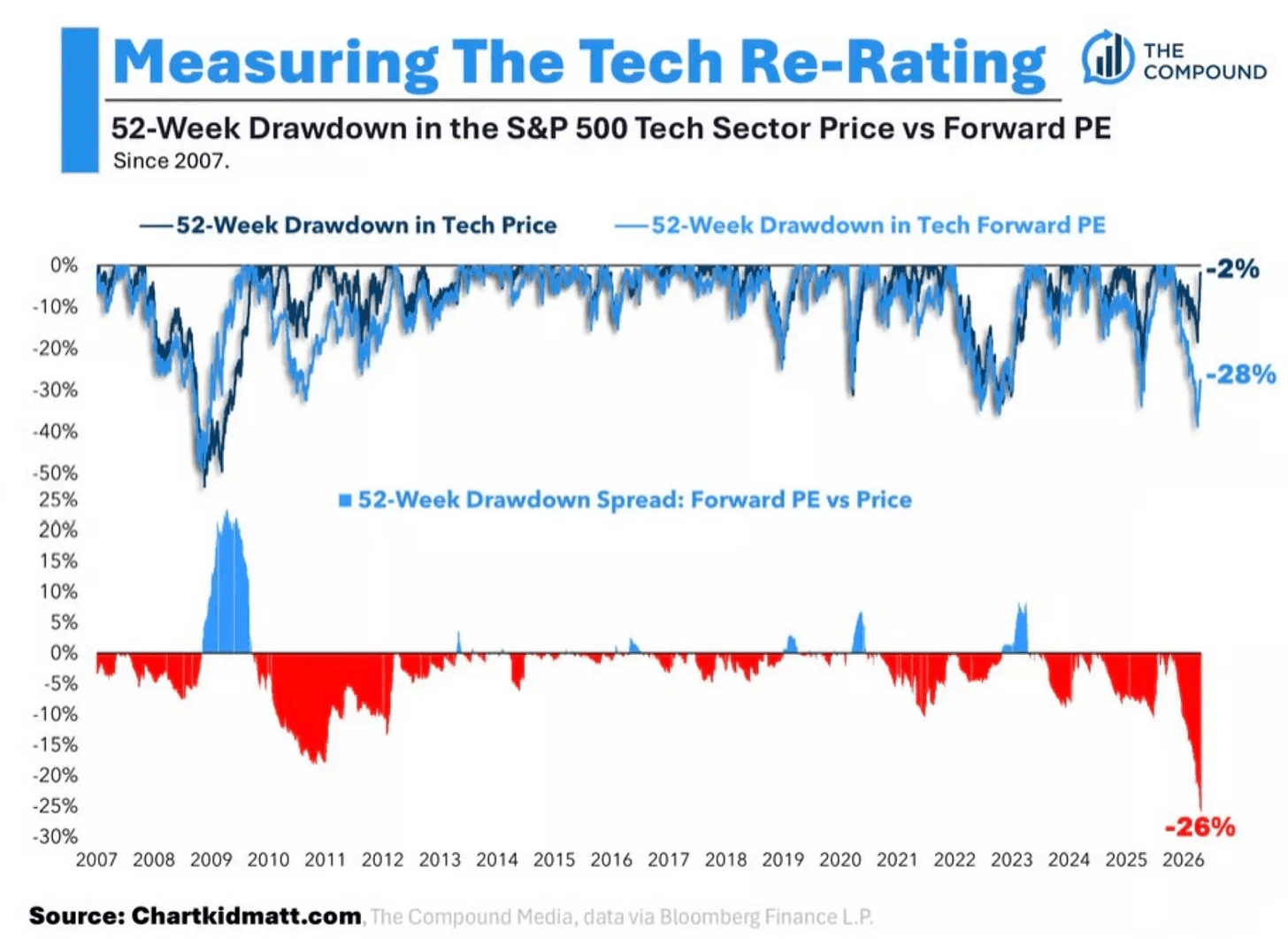

The S&P 500 technology sector is only about 2% below its 52 week highs on price. On the surface, that looks like a market still trading near peak levels.

But underneath, the valuation picture looks completely different.

The sector’s forward price-to-earnings multiple is down roughly 28% from its highs. In other words, investors are paying materially less for each dollar of future earnings than they were before, even while prices remain near the top of the range.

That is actually a healthy sign.

It means this is not just a rally built on excitement or speculative multiple expansion. It suggests the move is being supported by real earnings power, which is usually far more durable over time.

Hedge funds bought global technology stocks more aggressively last week than any other sector, marking the first net purchase of Information Technology in 5 weeks. That matters because leadership sectors often attract capital first when conviction starts to build.

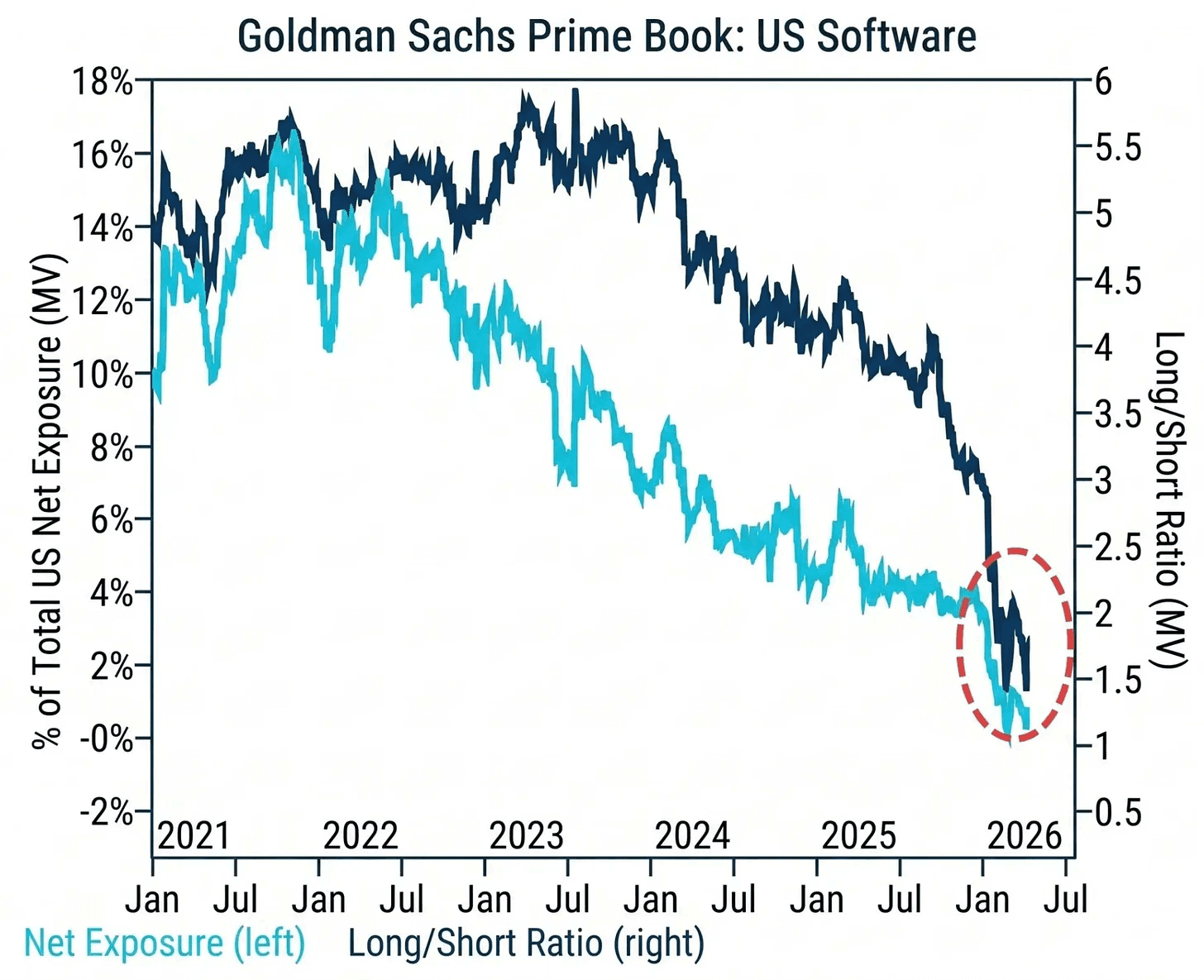

Everyone hates software.

You can see that in positioning data. Hedge fund net exposure to US software has fallen to just above 2%, one of the lowest levels in years. That sounds bullish on the surface, but it is also a reminder that trying to catch the biggest losers is usually the wrong game.

There is rarely an edge in buying stocks simply because they have fallen the most. Weak stocks often stay weak for longer than expected, especially when institutions are still reducing exposure. Cheap can always get cheaper.

It sounds counterintuitive, but in bull markets the better strategy is usually to focus on strength, not weakness. The market often tells you where money wants to go. The leading stocks and sectors are usually the ones making new highs or trading close to their highs while everything else struggles.

Strength tends to attract more strength. Institutions add to winners, analysts raise estimates, sentiment improves, and momentum builds on itself. Meanwhile, laggards often need a full turnaround story or a substantial catalyst before they come back to life.

I continue to be very positive, and I will stay that way until the data gives a real reason not to.

Does that mean the market cannot pull back or pause here? Of course not. Short-term moves happen all the time. What it means is that I will continue to view pullbacks, volatility, and drawdowns as opportunities rather than reasons to panic.

The biggest and most important piece of this entire market puzzle remains earnings. Over the long run, stocks tend to follow one thing above all else: the direction of corporate earnings. If earnings estimates keep getting revised higher and businesses continue to grow profits, stock prices usually follow over time.

If we do see a pullback in the coming weeks as a sell-the-news reaction to big cap tech earnings, I would likely view that as an opportunity to add exposure or rotate into the strongest leaders. Unless we get something truly catastrophic or meaningfully worse than expected from these reports, the broader direction of the market still looks clear in the bigger picture.

Previous Updates

View All

- Market Update: DeepSeek 2.0

- Weekly Market Update: All Eyes On the Mag 7

- Weekly Market Update: Earnings Season Is Here

- Market Update: The FinTech Comeback

- Weekly Market Update: Halftime

- Market Update: The Robots Are Coming

- Weekly Market Update: The Broadening

- Market Update: The Break Point

- Weekly Market Update: Patience

- Market Update: The Memory Crunch

- Weekly Market Update: The First Trillionaire

- Market Update: In Focus

- Weekly Market Update: Deleveraging